Market overview

A brief look at the past decade shows why investors cannot completely relax during the summer vacation. Especially in 2011 and 2015 the stress-removing benefits of a nice holiday quickly disappeared as August's market storms raged. This year, however, the vacation mood fell victim to this year's by now infamous curse, coronavirus. Though some markets recovered from the spring plunge and rushed from record to record, providing positive returns for the year as a whole, European holidaymakers had a lot to worry about. Almost daily there were changes to the list of countries to which they could still travel untroubled. In addition, talks about a second wave of coronavirus surfaced. New infections have indeed risen again. But the second wave, at least as experienced so far, differs significantly from the first. The average age of those infected is significantly lower. Lower still are Covid-19-related hospitalizations and deaths.[1] The degree to which serious cases have dropped is due to a possible weakening of the virus or to the summer weather, and whether or not younger people will eventually infect older, more vulnerable people, will become apparent in autumn. In light of the current data, however, we believe that renewed transnational lockdowns seem rather unlikely. What we do believe to be increasingly likely, however, is a slowdown in the economic recovery in the autumn. Even though sentiment indicators are positive worldwide – outside China and some of its neighbors – data such as unemployment, investment and industrial production are somewhat less benign and still far from pre-crisis levels.

These signs of economic frailty are compounded by a number of political developments in recent weeks that could make for a stormy autumn. The U.S. presidential election campaign is, as expected, getting tense and personal but beyond that, the incumbent president is warning almost daily that the election could be manipulated by postal votes and most likely be "stolen."[2] In order to guarantee the technical prerequisites for the postal vote, the U.S. Congress had to admonish the newly appointed head of the U.S. Postal Service.[3] Meanwhile, conflicts between left-wing demonstrators and Trump supporters and armed groups of nationalists are raging in various U.S. cities, with little prospect of a moderation before the election. How things might develop after a close election without an immediately clear winner is being discussed with increasing concern in the media. Derivative markets are also reflecting investor's nervousness for the period after the vote.[4] We consider serious political turbulence only as a small risk, but acknowledge that it might be longer than usual before we obtain official and final results.

Elsewhere, too, there was political drama in August. In the Mediterranean, the conflict over sea territories between Turkey and Greece is coming to a head. There have also been repeated skirmishes on the Chinese-Indian border and in Belarus Russian President Vladimir Putin has already offered his colleague Alexander Lukashenko administrative assistance in the form of troops. The poison attack on Russia's most prominent opposition leader, Alexei Navalny, in turn, threatens to worsen Russian-European relations to such an extent that even the Nordstream 2 Baltic gas pipeline project might be halted. And in Brexit negotiations the British side seems to be playing such high-risk poker that Brussels could run out of patience. Most directly relevant for the economy and markets, however, are the escalating tensions between the United States and China. With the announcement of sanctions against the largest Chinese Internet platforms, a new level has been reached and one from which there is unlikely to be any turning back. The consequences of just the measures announced by the United States so far are so far-reaching that it seems to be only a matter of time before China reacts clearly – and stock markets, too, take notice.

In August, however, investors remained extraordinarily confident, with the S&P 500 posting its biggest August price increase since 1986. The large American technology stocks, in particular, pulled away, as can be seen from the gain of 11.2% on the Nasdaq 100 in the month. August was also the month in which the market capitalization of a U.S. company exceeded the two-trillion-dollar mark for the first time. What was unusual about the U.S. stock rally, however, was that it was accompanied by increasing, not decreasing, volatility toward the end of the month, a rare phenomenon. Skeptical investors found some vindication at the beginning of September, when the Nasdaq 100 in particular corrected sharply, losing around 10% within three days. Bonds did not do so well in August, and gold also weakened again after a brilliant start to the month (the troy ounce rose above 2,000 dollars). The dollar continued to weaken, trading as low as 1.19 dollars to the euro at times. One reason for this may also have been this August's virtual Jackson Hole central-bank meeting in which Jerome Powell outlined the U.S. Federal Reserve's (Fed's) new framework, one that essentially means an interest-rate hike is no longer immanent even if inflation exceeds 2%. The central banks are thus even less likely to put an end to the low-interest-rate environment.

Outlook and changes

As the quarterly DWS strategy meeting was held in August, we will briefly outline our new 12-month forecasts, in addition to the tactical changes. We expect a significant recovery in the global economy in 2021, with 5.3% growth, but this will still not be sufficient for the vast majority of regions to return to their pre-crisis output levels. As a result of a strengthening economy and increasing public debt levels, inflation is likely to be higher than this year, but not to the extent that we would doubt that the low-interest-rate environment will continue we believe. Central-bank monetary policy continues to be strongly accommodating. Given that the recovery rally in most capital markets is already far advanced, we therefore expect potential returns only in the low single digits for the next 12 months, and possibly negative returns, for example for some government bonds.

From a tactical point of view, too, many markets appear to have run quite hot. In view of the political risks mentioned above, the possibility of further corrections has not diminished, even if monetary policy in particular should provide strong support. Fiscal policy too is generous and highly supportive. A problem emerging, however, is the difficulty getting the money to where it can bring a more sustainable boost to employment and investment. Moreover, in the United States agreement on a second stimulus package is being postponed more and more, so that there is the growing concern it will not be launched before the elections. That would have a significant impact on U.S. growth prospects.

Fixed income

The overriding theme for bonds remains central banks, which continue to show no signs of wanting to tighten the interest-rate screws. Instead they are signalling that they still have effective instruments at their disposal should the economy need further support. As grateful as the market is for these signals and corresponding action, they come as little surprise. Government-bond yields in the major industrial nations have been trading sideways within a relatively narrow band for some time now, and we expect this to continue, especially if the economic recovery is accompanied by setbacks and delays. We are positioning ourselves accordingly, depending on where yields are currently in this band. Upgrades and downgrades may be necessary at short notice, as we have recently seen with 10-year Treasuries and Bunds. However, we expect bond yields to rise slightly over the next 12 months, primarily in the United States. We expect the dollar to recover ground to 1.15 against the euro in this period. In case of corporate bonds, we currently prefer non-investment-grade (IG) issuers to IG issuers, and we prefer euro to dollar issuers.

Equities

We have not changed our equity positioning. In our view, sectoral vs. regional divergences continue to dominate, with the exception of China, South Korea and Taiwan, which have a clear lead in coping with the pandemic. This region also benefits from the increasing weighting of its technology sector, which we continue to see in a positive light strategically. It benefits from various trends, some of which have been reinforced by the pandemic. In the United States, where most of the technology heavyweights are based, a significant but as yet hardly noticed turnaround has taken place in recent weeks in our opinion. Until now, regulatory intervention has been regarded as the eternal sword of Damocles above the biggest in the industry. But with its sanctions against the only serious global competition – Chinese Internet platforms – Washington has now made it clear that it has no interest whatsoever in allowing its dominance to weaken, quite the contrary. From a tactical point of view, however, we have become a little more cautious about the sector in the course of August, even if we did not ultimately reduce it to neutral. Although its valuation has not yet reached the excesses of the 2000s, we believe it is optimistic. However, technology stocks also benefit from the most solid earnings performance among all sectors. During the crisis especially, the sector showed how it combines both growth potential and defensive qualities. The healthcare sector showed similar qualities, and we also continue to view it positively, even though there could be major price swings in the context of the U.S. election.

Alternatives

On a 12-month horizon we see further upside potential for gold, not least because demand is benefiting from concerns about excessively loose monetary policy and rapidly rising government debt. Moreover, gold has recently benefited from the weakening dollar and falling real yields. There is unlikely to be any monetary tightening to challenge gold for some time. But its tailwind is easing, too, as we now see the dollar and real yields moving sideways. We also expect the price of oil to continue its upward trend, albeit with strong fluctuations. At present there is a rough balance between the production discipline of the OPEC+ countries, which is weakening somewhat, reduced U.S. shale oil production, and the economic recovery. Setbacks are still conceivable, especially if the recovery in air traffic continues to falter.

The multi-asset perspective

The tactical positioning of the multi-asset team has remained slightly defensive recently. Market sentiment and market positioning became increasingly optimistic in the course of August, while volatility between asset classes continued to decline, though not to extreme levels. However, we believe that central-bank liquidity, low bond yields, fiscal support, and some catch-up potential in the positioning of institutional investors are providing the markets with a tailwind despite rising valuations.

Equities

Due to stronger earnings revisions and supported by a weaker dollar, we have become more positive on emerging-market (EM) equities, which we have upgraded to neutral. This region fits with our preference for cyclical and technology stocks. We particularly like China, Korea and Taiwan. At the same time, European equities have not been able to keep up with the United States, partly because of their sectoral weighting, with less technology and more financials, and so we have become somewhat more cautious, downgrading them to neutral. This means we currently have no regional preference. We have not completely abandoned our tactical positioning in value stocks in order to secure an increased positioning in the growth sector (i.e. technology, healthcare, etc.).

Fixed Income

Here we have hardly changed our positioning, but we have shortened duration somewhat in expectation of slightly rising yields. We continue to favor the United States over the Euro in government bonds. In corporate bonds we continue to prefer IG over high yield (HY) and euro over dollar bonds.

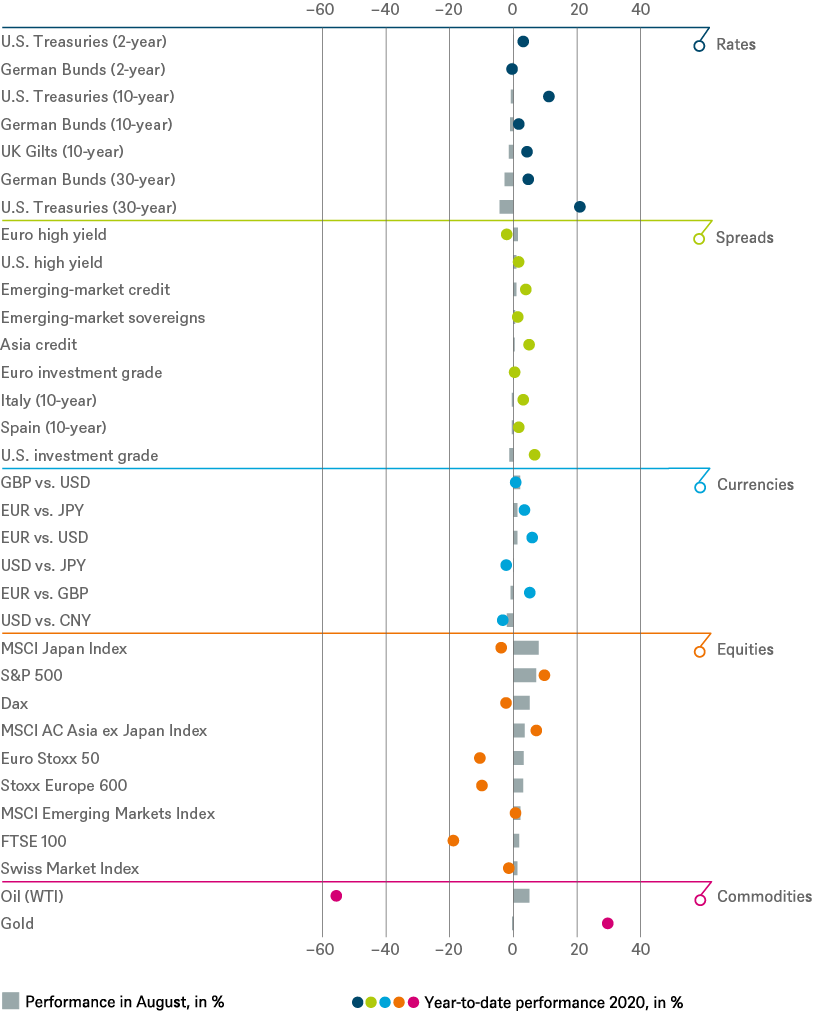

Past performance of major financial assets

Total return of major financial assets year-to-date and past month

Past performance is not indicative of future returns.

Sources: Bloomberg Finance L.P., DWS Investment GmbH as of 8/31/20

Tactical and strategic signals

Fixed Income

| Rates | 1 to 3 months | until September 2021 |

|---|---|---|

| U.S. Treasuries (2-year) | ||

| U.S. Treasuries (10-year) | ||

| U.S. Treasuries (30-year) | ||

| German Bunds (2-year) | ||

| German Bunds (10-year) | ||

| German Bunds (30-year) | ||

| UK Gilts (10-year) | ||

| Japan (2-year) | ||

| Japan (10-year) |

| Spreads | 1 to 3 months | until September 2021 |

|---|---|---|

| Spain (10-year)[5] | ||

| Italy (10-year)[5] | ||

| U.S. investment grade | ||

| U.S. high yield | ||

| Euro investment grade[5] | ||

| Euro high yield[5] | ||

| Asia credit | ||

| Emerging-market credit | ||

| Emerging-market sovereigns |

| Securitized / specialties | 1 to 3 months | until September 2021 |

|---|---|---|

| Covered bonds[5] | ||

| U.S. municipal bonds | ||

| U.S. mortgage-backed securities |

| Currencies | ||

|---|---|---|

| EUR vs. USD | ||

| USD vs. JPY | ||

| EUR vs. JPY | ||

| EUR vs. GBP | ||

| GBP vs. USD | ||

| USD vs. CNY |

Equities

| Regions | 1 to 3 months[6] | until September 2021 |

|---|---|---|

| United States[7] | ||

| Europe[8] | ||

| Eurozone[9] | ||

| Germany[10] | ||

| Switzerland[11] | ||

| United Kingdom (UK)[12] | ||

| Emerging markets[13] | ||

| Asia ex Japan[14] | ||

| Japan[15] |

| Style | |

|---|---|

| U.S. small caps[27] | |

| European small caps[28] |

Legend

Tactical view (1 to 3 months)

- The focus of our tactical view for fixed income is on trends in bond prices.

- Positive view

- Neutral view

- Negative view

Strategic view until September 2021

- The focus of our strategic view for sovereign bonds is on bond prices.

- For corporates, securitized/specialties and emerging-market bonds in U.S. dollars, the signals depict the option-adjusted spread over U.S. Treasuries. For bonds denominated in euros, the illustration depicts the spread in comparison with German Bunds. Both spread and sovereign-bond-yield trends influence the bond value. For investors seeking to profit only from spread trends, a hedge against changing interest rates may be a consideration.

- The colors illustrate the return opportunities for long-only investors.

- Positive return potential for long-only investors

- Limited return opportunity as well as downside risk

- Negative return potential for long-only investors

Appendix: Performance over the past 5 years (12-month periods)

| 08/15 - 08/16 | 08/16 - 08/17 | 08/17 - 08/18 | 08/18 - 08/19 | 08/19 - 08/20 | |

|---|---|---|---|---|---|

|

Asia credit |

10.2% |

2.4% |

-0.9% |

10.9% |

5.9% |

|

Covered bonds |

3.8% |

-0.9% |

0.3% |

4.9% |

-0.8% |

|

Dax |

3.2% |

13.8% |

2.6% |

-3.4% |

8.4% |

|

EM Credit |

11.3% |

5.6% |

-1.6% |

12.2% |

6.6% |

|

EM Sovereigns |

14.2% |

5.0% |

-3.4% |

13.8% |

2.7% |

|

Euro high yield |

6.8% |

6.4% |

1.2% |

4.8% |

-0.4% |

|

Euro investment grade |

6.7% |

0.6% |

0.0% |

6.7% |

-0.9% |

|

Euro Stoxx 50 |

-3.8% |

17.0% |

2.6% |

4.8% |

-1.8% |

|

FTSE 100 |

13.0% |

14.0% |

4.1% |

1.4% |

-14.3% |

|

German Bunds (10-year) |

8.0% |

-2.0% |

1.2% |

8.5% |

-2.6% |

|

German Bunds (2-year) |

0.3% |

-0.5% |

-0.7% |

0.0% |

-1.3% |

|

German Bunds (30-year) |

18.6% |

-7.7% |

3.2% |

21.8% |

-4.4% |

|

Italy (10-year) |

9.0% |

-3.3% |

-6.6% |

22.1% |

1.2% |

|

Japanese government bonds (10-year) |

3.8% |

-0.4% |

-0.5% |

3.6% |

-2.6% |

|

Japanese government bonds (2-year) |

0.2% |

-0.2% |

-0.2% |

0.2% |

-0.5% |

|

MSCI AC Asia ex Japan Index |

12.9% |

24.8% |

2.8% |

-6.3% |

21.6% |

|

MSCI AC World Communication Services Index |

2.5% |

-0.9% |

-8.3% |

7.9% |

21.4% |

|

MSCI AC World Consumer Discretionary Index |

2.9% |

13.5% |

16.0% |

-1.5% |

33.2% |

|

MSCI AC World Consumer Staples Index |

11.5% |

3.4% |

-1.8% |

7.9% |

3.3% |

|

MSCI AC World Energy Index |

2.8% |

-0.6% |

17.7% |

-18.6% |

-30.4% |

|

MSCI AC World Financials Index |

-2.0% |

23.1% |

2.3% |

-7.9% |

-8.8% |

|

MSCI AC World Health Care Index |

-2.5% |

8.8% |

11.8% |

-2.0% |

21.6% |

|

MSCI AC World Industrials Index |

9.7% |

15.4% |

6.9% |

-3.4% |

5.3% |

|

MSCI AC World Information Technology Index |

16.5% |

30.5% |

24.1% |

2.1% |

51.8% |

|

MSCI AC World Materials Index |

9.6% |

22.1% |

2.5% |

-9.2% |

12.8% |

|

MSCI AC World Real Estate Index |

12.8% |

2.9% |

-0.5% |

7.4% |

-10.0% |

|

MSCI AC World Utilities Index |

6.8% |

10.1% |

-4.3% |

12.0% |

-2.4% |

|

MSCI Emerging Market Index |

11.8% |

24.5% |

-0.7% |

-4.4% |

14.5% |

|

MSCI Japan Index |

2.9% |

13.7% |

9.0% |

-5.6% |

10.2% |

|

Russel 2000 Index |

6.9% |

13.3% |

23.9% |

-14.1% |

4.5% |

|

S&P 500 |

12.6% |

16.2% |

19.7% |

2.9% |

21.9% |

|

Spain (10-year) |

10.9% |

-0.2% |

2.4% |

12.5% |

-1.1% |

|

Stoxx Europe 600 |

-1.6% |

12.6% |

5.8% |

3.2% |

-0.7% |

|

Stoxx Europe Small 200 |

-0.3% |

16.8% |

9.9% |

-1.9% |

5.2% |

|

Swiss Market Index |

-3.7% |

12.4% |

4.0% |

14.0% |

5.9% |

|

U.S. high yield |

9.1% |

8.6% |

3.4% |

6.6% |

4.7% |

|

U.S. investment grade |

9.1% |

1.9% |

-1.0% |

13.0% |

7.1% |

|

U.S. MBS |

-44.4% |

100.0% |

-3.3% |

62.1% |

19.1% |

|

U.S. Treasuries (10-year) |

7.0% |

-1.4% |

-3.1% |

13.7% |

8.6% |

|

U.S. Treasuries (2-year) |

1.1% |

0.5% |

-0.1% |

4.4% |

3.5% |

|

U.S. Treasuries (30-year) |

16.7% |

-5.4% |

-2.8% |

24.2% |

13.0% |

|

UK Gilts (10-year) |

12.3% |

-1.0% |

-1.1% |

9.2% |

1.8% |

Sources: Bloomberg Finance L.P., DWS Investment GmbH as of 9/10/20

Past performance is not indicative of future returns. Forecasts are based on assumptions, estimates, opinions and hypothetical models that may prove to be incorrect.

1. See https://www.worldometers.info/coronavirus/

2. See, as one example of many a tweet from July 26: "The 2020 Election will be totally rigged if Mail-In Voting is allowed to take place, & everyone knows it. So much time is taken talking about foreign influence, but the same people won't even discuss Mail-In election corruption. Look at Patterson, N.J. 20% of vote was corrupted"

3. See: https://www.nytimes.com/2020/08/21/us/politics/dejoy-postal-service-senate-hearing.html

4. As can be seen in higher implied volatilities for S&P 500 options expiring in November.

6. Relative to the MSCI AC World Index

7. S&P 500

9. EuroStoxx 50

10. Dax

12. FTSE 100

13. MSCI Emerging Markets Index

14.

MSCI AC Asia ex

Japan Index

15. MSCI Japan Index

16. MSCI AC World Consumer Stables

17. MSCI AC World Health Care Index

18. MSCI AC World Communication Services Index

19. MSCI AC World Utilities Index

20. MSCI AC World Consumer Discretionary Index

21. MSCI AC World Energy Index

22. MSCI AC World Financials Index

23.

MSCI AC World

Industrials Index

24. MSCI ACWI Information Technology Index

25. MSCI AC World Materials Index

26. MSCI AC World Real Estate Index

27. Russel 2000 Index relative to the S&P 500

28.

Stoxx Europe Small 200 relative to the Stoxx

Europe 600

29.

Relative

to the Bloomberg Commodity Index