- The outcome of the federal election is more uncertain than ever before.

- Of particular relevance for the capital markets are programmed differences on taxes, spending policy and European fiscal union.

- An abrupt change in policy, however, is hardly to be expected due to the fed-eral distribution of power in Germany.

1 / The end of an era

The German federal elections will be held on September 26. That much is certain. But the outcome of the elections is uncertain to an extent that is unusual for Germany. For the first time in the history of the Federal Republic the incumbent is not up for re-election. Over the past 16 years, Angela Merkel has stood for continuity and reliability in German politics – especially abroad. This upcoming change alone is likely to cause increased uncertainty. Moreover, it is completely unclear which coalition the new chancellor will lead. Never before has the range of possible coalitions been as wide. To make matters worse, there is a probability that the next coalition will even consist of a three-party alliance – due to the proportional representation in German electoral law.

However, a new government consisting of a multiparty alliance would actually lead to continuity rather than dramatic changes. In German politics, the coalition agreement traditionally plays a major role and its importance is likely to increase: The more parties have participated in a coalition agreement, the more difficult it will be to renegotiate it at a later date. This also considerably limits the power of a new chancellor. Certainly, with Armin Laschet (CDU), Annalena Baerbock (Greens) or Olaf Scholz (SPD), there will be a somewhat different leadership style than under Angela Merkel, but it is primarily the parties that decide the fundamental policy direction.

In this CIO Special, we focus on the parties' election programs and possible consequences for potential coalition governments, as we assume that the new chancellor's room for maneuver will be considerably constrained by the coalition agreement.

Article continues on next page...

2 / The year of the swing voters

2.1 The polls

Looking at the polls, it is still too early to declare a winner or predict a winning coalition. Fig. 1 shows how widely the poll ratings are fluctuating, especially those for the center-right Christian Democratic Union (CDU) / Christian Social Union (CSU). One reason for the soaring popularity of the current grand coalition of the CDU/CSU and Social Democrats (SPD) has been the coronavirus pandemic. Crises are often good times for rulers, giving them the chance to demonstrate their usefulness, and, all in all, Germany has come through the pandemic quite well by international standards. This was especially the case during the first two waves of Covid infections. Interestingly, the CDU/CSU and the CDU in particular seem to have profited far more from this than the SPD. This is probably due to Angela Merkel's un-agitated but determined way of handling the crisis. However, approval of the government dropped sharply during the third wave and with the sluggish start of the vaccination campaign. Recently, the CDU/CSU's approval ratings rose again as the vaccination campaign progressed.

Fig. 1 Polling data for the federal election: Large fluctuations

The course of the pandemic in the remainder of the summer is still likely to have a strong influence on the poll ratings. If vaccinations continue to make good progress, the incidence of infection remains manageable and, above all, schools reopen on time in August and stay open during September, this is likely to have a positive impact for the governing parties, especially the CDU/CSU. On the other hand, if there are further major storms or floods, or this summer proves particularly hot and dry, climate change could gain in influence and give the Greens a fresh opinion-poll boost.

According to current poll figures, it is almost impossible for one party to achieve an absolute majority of seats in the Bundestag.

2.2 The possible coalitions

Before delving into the programs of the various parties, it makes sense to look at the potential governing coalitions. After all, according to current poll figures, it is almost impossible for one party to achieve an absolute majority of seats in the Bundestag (see figure 2 below). In this analysis we look at parties that could potentially be part of a governing coalition and therefore exclude the right-wing AfD because all the other parties have ruled out forming a coalition with it.

Fig. 2 shows the potential coalition governments. We currently consider a grand coalition of the CDU/CSU and the Greens, with Armin Laschet of the CDU as chancellor, to be the most likely outcome – even if this should not be taken as a reliable forecast at this early stage. The number of votes needed for a majority will depend not least on how many parties fail to obtain the 5% of the total vote needed in order to be given any seats, and, in particular, on whether die Linke (the Left – a left-wing party, as its name suggests) makes it.

Fig. 2 Potential coalitions: Great diversity

What emerges strikingly is that the Greens would be involved in almost all the most likely coalitions. The FDP also has a good chance of being part of the governing coalition this time. Unlike the CDU/CSU, both the Greens and the FDP do not stand for continuity and would represent a break from the current government; they would want to put a different stamp on the nation’s politics. We therefore take a closer look at these parties. (For clarity, we have detailed the parties' programs in the appendix. See PDF)

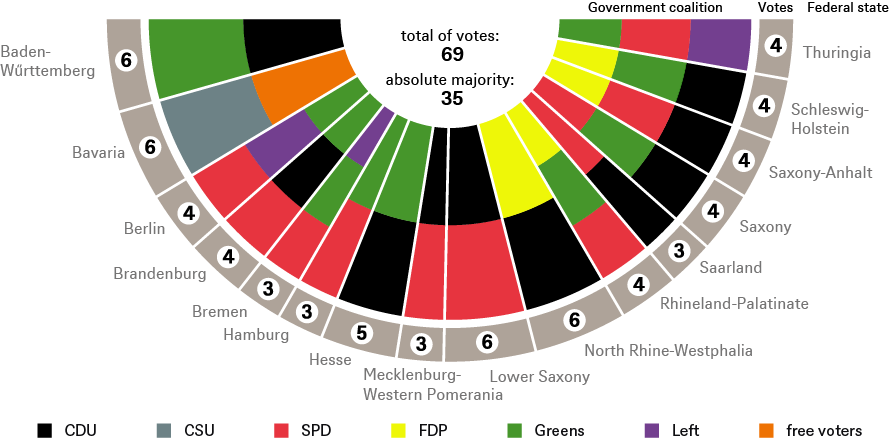

2.3 The Bundesrat – the consensus machine

The Bundesrat, Germany's Upper House, exercises a "right of co-determination" with respect to numerous laws. Most important laws require not only the approval of the Bundestag, but also that of the Bundesrat. This includes all amendments to the constitution and legislative projects that affect the sovereignty of the states, including many tax laws. However, there is such a patchwork of coalitions in the 16 federal states (see Fig. 3) that the CDU, the SPD and the Greens can take down any law requiring approval in the Bundesrat. This is because the coalition partners in a state’s government have to agree on how to vote on a proposed law and if they don't, the state in question abstains from voting. This abstention, in turn, counts as a de-facto "no" vote for laws requiring approval.

Fig. 3 Composition of The Bundesrat: A patchwork forces compromise

Source: Federal Council; Status: 16.09.2021

As a result, important proposed legislation in Germany has required the approval of not only the federal coalition partners CDU/CSU and SPD but also the Greens for some time now. In this sense, Germany has long been governed by a still grander "grand coalition" than the three ruling parties, and this is unlikely to change much after the Bundestag elections. Weighty projects, such as constitutional amendments, still require the approval of all relevant parties. This also means, in particular, that the options for a government "without the CDU/CSU," for example a green-red-red coalition of the Greens, SPD and the Left, would be significantly restricted by the CDU's veto power in the Bundesrat.

There is such a patchwork of coalitions in the 16 federal states that the CDU, the SPD and the Greens can take down any law requiring approval in the Bundesrat.

Article continues on next page...

3 / The campaign issues

The key issues on the government’s agenda in the coming legislative period are climate change and fiscal policy. From a capital-market perspective, however, we also consider the government’s stance towards the European Union (EU) and the rest of the world to be relevant. In the following analysis, we rely on the election programs of the parties as published. It is noticeable, however, that some of the goals are addressed only very vaguely and avoid detailed analysis. This is particularly true of those parties that are very likely to be involved in a new government. One could almost say that the more likely parties are to be members of the government, the more vague the programs they set out to accomplish. This is not so surprising. All the parties know that they will only be able to govern in a coalition. This means that every opponent in the election campaign may become a party with which it is necessary to carry out coalition negotiations – and may later become a partner in government. The more red lines one has drawn before the election, the more complicated the later negotiations will be. And any crossed red lines would also make it harder to convince one's own party members that whatever is agreed in coalition negotiations is acceptable. In this election, just who you will be negotiating and, ultimately, working with is particularly uncertain. This makes the political game all the more complicated.

In June, the German parliament passed the Climate Protection Act 2021, bringing forward the goal of net-zero greenhouse-gas emissions from 2050 to 2045.

3.1 Climate change

One of the key issues in this election campaign – all the more so after the catastrophic flooding in July – is climate change. The heart of the matter is the reduction of greenhouse-gas emissions, and above all the CO2 reduction target. The issue is hardly controversial. In June, the German parliament passed the Climate Protection Act 2021, bringing forward the goal of net-zero greenhouse-gas emissions from 2050 to 2045. This means that the climate target is already ambitious. The Greens, however, are aiming for an even more ambitious reduction target: net zero by 2040. But in a coalition, especially one involving the CDU/CSU or the FDP, the Greens are likely to find it difficult to push through a (further) tightening, and the differences compared with the current law are slight (Fig. 4). Therefore, remarkably enough, the participation of the Greens in a federal government is not likely to make that much difference on this issue at this point. One could say that the Greens have already succeeded in persuading other parties that climate change must be addressed urgently.

Fig. 4 CO2 Reduction Targets: Small difference

However, there are major differences between the parties in the means they intend to use to achieve their goals. The CDU/CSU and, above all, the FDP are relying more on market-based instruments (especially emissions trading[1]), while the Greens, SPD and Left are relying more on taxes and bans. For example, the Greens and the Left want to ban the sale of new internal combustion vehicles from 2030. While the CDU/CSU and especially the SPD are concerned about how the social consequences of climate-protection measures can be mitigated, the FDP also sees climate protection as offering great opportunities for the use of innovative technologies. We will deal with the different approaches to climate policy in a separate article.

3.2 Fiscal policy

3.2.1 Income taxes

The greatest differences between the left-wing and the conservative parties are in fiscal policy. Judging by their election programs, a coalition government of the CDU/CSU and FDP would provide tax relief for taxpayers across the entire income distribution. High-income earners would benefit in particular from the elimination of the solidarity surcharge. According to the calculations of the ZEW economic research group[2], however, the government’s budget would be significantly burdened, and income inequality would increase slightly. A "left-wing" coalition government consisting of the Greens, the SPD and the Left, however, would tailor their fiscal policy precisely to the goal of reducing income inequality. In addition to relief at the lower end of the income scale, there would be tax increases. All three of the more left-wing parties want to introduce a wealth tax and increase or tighten inheritance tax. Those on lower incomes would be relieved of the burden of paying inheritance tax but those with high wealth or inheritances would have to reckon with substantial tax increases – which the Left sees as a priority. According to ZEW's calculations, the tax plans of the Greens and SPD would ease the burden on the national budget and reduce income inequality somewhat; the far-reaching proposals of the Left would even inject considerably more money into the government budget and significantly reduce income inequality.

3.2.2 Corporate taxation

A global desire is emerging for the establishment of a minimum corporate taxation. Even if the first international agreements are still quite vague and likely to affect only a few large companies, the direction is clear: "a tax race to the bottom" is out of fashion. The U.S. in particular is aiming for a global minimum corporate tax rate of 15%, and the U.S. Treasury Secretary would even prefer a higher minimum than that. Germany is already one of the high-tax countries (Fig. 5). The current corporate income tax of 15% is supplemented by a trade tax[3] at an average rate of around 14% and the solidarity surcharge at just under 1%, so that the total tax burden is around 30% at the moment.

That leaves Germany's parties pushing in different directions. The CDU/CSU wants to cap the tax on retained corporate earnings at 25% while the Greens want an EU-wide minimum corporate taxation of 25%. The Left wants to raise Germany's corporate income tax to 25% (from the current 15%) which would lead to a total tax load of 40%. Only the FDP is actually aiming for a comprehensive reform of corporate taxation, including the abolition of the trade tax and a reduction in the overall burden to 25%. But the FDP, too, wants to see a global minimum corporate tax rate.

"a tax race to the bottom" is out of fashion.

Fig. 5 Corporate Tax Rates: High-tax country Germany

All parties want to invest massively in education and digitization

3.2.3 The federal budget: Between "black zero" and public investment

All party programs address the debt brake, which limits annual federal government borrowing to no more than 0.35% of gross domestic product (GDP). Unfortunately, all party programs are short on details. Interestingly, it is precisely those parties whose tax plans would put a strain on the budget that want to return to the debt brake and the so-called "black zero" (a balanced federal budget) as quickly as possible. The FDP even wants to tighten the debt brake further by having the non-insurance benefits of the social-security funds financed entirely from the federal budget. That would end circumventing the debt brake by shifting expenditures from the federal budget to the social-security system. The more left-wing parties, on the other hand, would like to exploit the "constitutional leeway" allowed by the debt brake, or even expand it. The Greens, for example, want to make the debt brake looser by adjusting it to the interest burden, which is exceptionally low at present due to the ECB's zero-interest-rate policy, and the Left wants to abolish the debt brake altogether.

To make matters worse, all parties see a huge need for private investment – and are not entirely without reason to do so – and for more public investment. For example, combating climate change requires considerable investment, from insulating buildings to providing the necessary infrastructure for electric transport, to generating renewable energy for the increase in electricity demand. In addition, all parties want to invest massively in education and digitization. The CDU/CSU wants a modernization decade, the Greens want 500 billion euros in additional public investment over the next ten years, and the Left wants 10 billion euros right away for broadband expansion alone. Germany has been lagging behind in terms of public investment in an international comparison for years anyway (Fig. 6).

Fig. 6 Public Investment: A lot to do

All in all, there is much to suggest that there will indeed be a substantial expansion of public investment. In that case, however, greater tax relief is unrealistic, irrespective of the make-up of the governing coalition, as new borrowing is subject to relatively tight limits imposed by the constitutionally enshrined debt brake. This is all the more true since the debt brake can only be removed from the Basic Law with the agreement of the CDU/CSU, SPD and Greens. If the CDU/CSU is in government, it will certainly not want to tamper with the debt brake; if it is in opposition, it will not allow the government this triumph and will exercise its power via the Bundesrat. On the other hand, every government will probably try to exploit the leeway provided by the debt brake, which is certainly available, given the July storm disaster.

According to United Nations forecasts, the working-age population will decline by one percent per year by the end of the decade.

3.3 The pension system

The parties' ideas on the pension system are very heterogeneous, but potentially quite relevant for capital markets. The Left merely wants to strengthen public pension insurance, while the CDU/CSU initially wants to set up a reform commission and then make a fresh start on the private pension system. The proposals of the SPD, Greens and FDP are aiming for additional capital-funded pension provisions. The SPD and the Greens want this to follow the Swedish model and invest the money according to ecological criteria in the form of a publicly managed "citizens' fund.”[4] The FDP, on the other hand, is in favor of privately organized pension funds ("equity pension").

Reform of the pension system as planned by most parties is certainly urgently needed. Germany is facing dramatic demographic change. According to United Nations[5] forecasts, the working-age population will decline by one percent per year by the end of the decade. In our view, equities could play a central role in solving this, not least because there is still an underdeveloped equity culture in Germany. In our opinion, competitive solutions should be given preference.

3.4 Europe

Even though all potential governing parties are clearly pro-EU, their positions are quite different. This applies in particular to the issues of further fiscal integration and the handling of the Stability and Growth Pact (SGP), which are certainly relevant to the capital market. The attitudes of the political camps toward the SGP largely correspond to their views on German fiscal policy. The more left-wing parties see the 750-billion-euro Recovery and Resilience Program (RRP)[6] as an opportunity to enter into further fiscal integration and want to perpetuate, in one form or another, the underlying mechanism (paying according to performance, withdrawing according to need). The CDU/CSU parties and the FDP, on the other hand, see the RRP as a one-off and want to return to the strict Maastricht budgetary criteria as soon as possible. Given that all major EU countries currently have a national debt of well above the Maastricht cap of 60% of GDP (Fig. 7), the austere approach could well cause irritation in capital markets, especially with regard to government bonds from the periphery. While there is a general trend in the EU toward looser or more supportive fiscal policies, even a change in the SGP would require the approval of all member states. That is unlikely at the moment, and as long as the CDU/CSU or the FDP are involved in a government, not much is likely to happen here.

Fig. 7 Debt Levels: Beyond maastricht

Article continues on next page...

3 / Conclusion

Although there is great uncertainty regarding the outcome of the elections, the possible coalitions and the agreement they could reach, we venture to put forward the following conclusions now.

- First, regardless of the election outcome, not that much will change. This is because there is already a broad consensus in Germany on important issues (such as climate change and Europe) and because the government’s power is constrained by the legislature: It is very unlikely that a governing coalition will have a two-thirds majority in the Bundestag. Amendments to the Basic Law would therefore only be possible by broad consensus. And important laws that would need the approval of the Bundesrat would require the consent of the CDU, the SPD and the Greens anyway.

- Third, public investment will increase. All parties want to invest in combating climate change, in digitization and in education.

- Fourth, the debt brake will remain. There will certainly be efforts to interpret it creatively, but abolishing it does not seem feasible at present, with the CDU and the FDP in government or in opposition. This also means that the scope for tax cuts is very limited.

- Fifth, German policy will remain pro-European in its basic orientation.

Our base scenario of a black-green (CDU/CSU and the Greens) coalition is likely to be met with a shrug of the shoulders by capital markets because it has already been priced in. The same applies to all coalitions in which at least one center-right party (CDU/CSU and FDP) and a left-wing party (SPD, Greens and the Left) are represented.

A conservative coalition of CDU/CSU and FDP could be positively received on the stock markets due to its more market-oriented policies, but its strict fiscal ideas could cause a "European scare" on the bond markets. By contrast, a left-wing coalition government comprising of the Greens, SPD and the Left is likely to cause some concerns on the stock markets about further (direct) regulation and a less growth-oriented policy approach, while bond markets might react more positively given the more Europe-friendly attitude.

But, all in all, there is much to suggest that the German parliamentary elections will not shake up German or European politics or the capital markets too much.