The latest U.S. Federal Reserve (Fed) interest-rate cut by 25 basis points (bps) along with persistent geopolitical conflicts – in particular in Saudi Arabia and between China and the United States – have provided support for gold. It is, however, a non-ferrous, silvery-white metal that is currently attracting our attention. Nickel is outshining gold. The yellow metal was given a bit less help than expected by a Federal Open Market Committee statement that did not promise more rate cuts but nickel has found other fundamental drivers. Indonesia, the world's largest nickel exporter, has brought forward its ban on nickel-ore exports to January 2020 from 2022, creating fears of a supply shortage at the London Metals Exchange. Given its limited mineable nickel resources, Indonesia is making a strategic shift toward more refined products, such as electric-vehicle battery production. It might be challenging for other large exporters, such as the Philippines, to fill the supply gap at such a scale. China – the largest nickel consumer – is likely to be particularly affected by any shortage.

While precious metals and in particular gold tend to react in a predictable fashion to central-bank policies, i.e. interest-rate changes, the reaction function of base metals is linked to the manufacturing industry and therefore currently dominated by the development of the trade talks between China and the United States. In each base metal, however, different underlying fundamentals are at play.

A major drone attack on Saudi oil infrastructure at Abqaiq and Khurais took 5.7 million barrels of crude oil per day offline – equivalent to almost half the Saudi output and 5% of global output, leading to a sharp spike in oil prices [CIO Flash as of 9/16/19]. While prices plateaued soon, not least because the Saudi Energy Minister sought to calm a frazzled market, we believe the geopolitical risks are fundamentally underpriced. Any potential for military escalation in the region is likely to keep prices elevated in the short term. The attack comes at a time when Saudi Arabia is focused on preparing one of the largest initial public offerings (IPO) in history. The Saudis are therefore particularly keen to calm down markets. Strategically, we believe that prices will grind lower as growth rates are coming down. The usual suspects, disruptions from Brexit, weakness in global manufacturing activity, protectionist endeavors and trade-related uncertainties, continue to weigh on the oil-demand outlook. In line with that, the International Energy Agency (IEA) has revised down its oil-demand forecast for 2020. Decreasing demand coupled with surplus supply in the long-term does not favor prices. We have therefore revised our 12-month forecast down to 54 dollars per barrel for West Texas Intermediate (WTI) in our quarterly strategy meeting. In the long term compliance with OPEC plus production cuts will be critical when trying to keep the market in balance.

Natural gas benefitted from a seasonal demand increase and is likely to be supported by cooler temperatures in the short term. Its price was probably supported, too, by winter prices[1] for natural gas that had drifted too low and the recent hot weather. However, year-to-date natural gas prices have been depressed compared to history, with record U.S. natural-gas production being an important factor. While a large amount of the increase in U.S. production has been absorbed by expanding inventories, we take a cautious view on long-term prices.

On the agricultural front, developments in the U.S.-China trade negotiations continue to be front and center. We were surprised by the World Agricultural Supply and Demand Estimates (WASDE) report. We had expected lower corn acreage due to delays in planting caused by adverse weather earlier in the year. Historically, late planting has led to lower corn yields but the WASDE report actually showed increased expected yields compared to the last report. Additionally, the U.S. Department of Agriculture (USDA) Farm Service Agency's report of increased "cover-crop" acreage late in August could mean that many planted acres will ultimately not be harvested.[2] Given the reported data, we believe corn is likely to outperform due to a shortage of supply.The expectation is for domestic and international beef demand to remain strong throughout 2019. Similarly, demand for pork remains strong and insensitive to price increases. The spread of African Swine Fever (ASF)[3] throughout China significantly reduced the hog-herd population. Therefore, China continues to be dependent on the United States to satisfy not only its pork but also its soybean demand. Whether driven by renewed goodwill or purely by need, China's resumed buying of U.S. soybeans might eventually bring them back to the negotiating table with the United States.

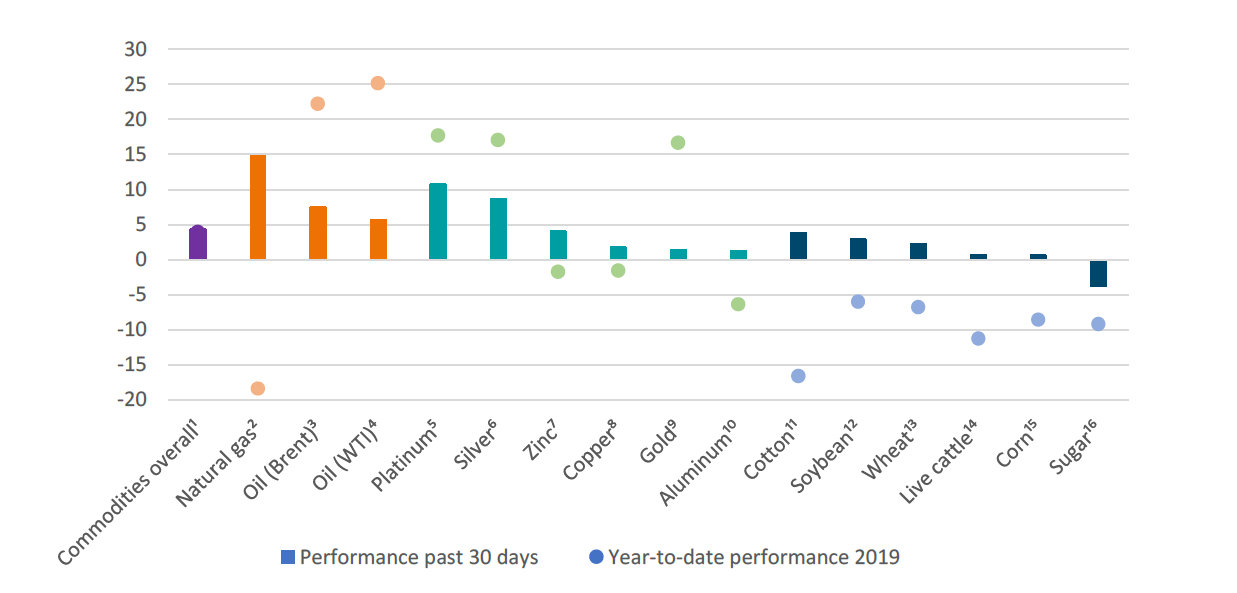

Past 30-day and year-to-date performance of major commodity classes

Platinum Subindex; 6 Bloomberg Silver Subindex; 7 Bloomberg Zinc Subindex; 8 Bloomberg Copper Subindex; 9 Bloomberg Gold Subindex; 10 Bloomberg Aluminum

Subindex; 11 Bloomberg Cotton Subindex; 12 Bloomberg Soybeans Subindex; 13 Bloomberg Wheat Subindex; 14 Bloomberg Live Cattle Subindex; 15 Bloomberg

Corn Subindex; 16 Bloomberg Sugar Subindex

Sources: Bloomberg Finance L.P., DWS Investment Management Americas Inc. as of 9/23/19

[1] Generally, U.S. gas prices are more volatile and higher during the winter period, where demand is high.

[2] Cover crops improve commodity yields and improve the soil significantly and are usually planted on corn, soybean or cotton acres.

[3] African Swine Fever is a highly contagious viral disease of wild and domestic pigs.