Market overview

The MSCI AC World Index rose by a miserable 0.01% in January. The virtual standstill might seem to suggest that nothing much happened. So we might as well go straight to the outlook section then, right? Well, not so fast. There were some quite unexpected and important developments during the month.

Let's start with politics. After much toing and froing, a so-called phase-one trade agreement was signed by the United States and China in mid-January. The market saw this as positive. Its mantra was that "trade uncertainty has fallen." And certainly some of the damage both countries had previously done to one another was reversed. But the agreement did not do much more than that. Essentially it represents a ceasefire in a very tense conflict. It obliges China to import significantly more from the United States than it has done so far, in clearly defined sectors and in clearly defined quantities. This is a strange development, as if the United States took lessons from China in terms of a planned-economy. But how China is to execute on this shopping list in practice is uncertain. And the signal this risky maneuver gives world trade is negative. First, China's U.S.-focused imports will be at the expense of other countries, including Germany. Second, and in our opinion this is more serious for the decision-making of global corporations, it means we are moving away from multinational regulatory frameworks, supported by the World Trade Organization (WTO), toward bilateral trade agreements. The United States' blockade of appointments to the Appellate Body is also wounding the WTO, leaving it largely paralyzed at present.

The capital markets are therefore showing their typical perversity: a certain deterioration is preferred to lingering uncertainty. The Brexit saga also shows this. Yes, it is now certain that, after 47 years of membership, the UK left the European Community at the end of January. And Boris Johnson's clear election victory gives him a strong mandate. But the next eleven months, during which the island kingdom plans to establish rapidly its new relationship status with the European Union (EU), are likely to provide both politicians and businesses with plenty of headaches.

Another certainty is the future of the high-ranking Iranian military commander, Qasem Soleimani. He was executed by the United States on January 3 in Iraq. Global stock markets and the oil price reacted, but retraced their moves after only a few days. Another issue that has political weight but little impact on markets is the ongoing impeachment process against Donald Trump. There is thought to be no chance anyway of removing the President due to the Republican majority in the Senate. Continuing protests in Hong Kong, and strikes and street protests in France, should also not be forgotten. If President Macron's government abandons its pension plans, we would see it as a fatal signal on France's ability to reform.

On the economic side, a quick conclusion can be given for the month: there was stabilization overall but with data to encourage both skeptics and optimists. The fourth quarter gross-domestic-growth (GDP) figures for the United States are a case in point. We find the data more bitter than sweet, showing some signs of a weakening trend in growth. Germany's Ifo, new orders and industrial production figures are also showing, at best, signs of bottoming – and might warn of weaker growth.

The wildcard is the development that has brought the markets' early 2020 upturn to an end and whose impacts on people, economies and markets cannot yet be reliably determined. The new coronavirus – 2019-nCoV in medical terminology – emerged at the turn of the year. By the end of January it had already infected more than 10,000 people, killing over 200.[1] The extensive restrictive measures China has introduced to contain the spread of the virus may reduce China's GDP growth by one to two percentage points this year – in the absence, at least, of a subsequent catch-up should the virus be contained and of compensating economic stimulus by the government. Our baseline scenario foresees a flattening of the rate of new infections by mid-February – but you can read about how much uncertainty is involved in our DWS CIO Flash as of 1/28/20.

Beneath the still surface of the MSCI AC World Index in January, divergent factors were, then, in play. Simultaneous risk-on and risk-off one might call it: many equity sectors and corporate-bond segments again did well – risk-on – while investors searched for safety favored government bonds and gold – risk-off. Oil and copper, on the other hand, two classical proxies for economic momentum, were amongst the biggest losers in January. Investors, thus, seem to be as afraid of missing out on the rally as they are skeptical of it. Amid fears of weaker economic growth, ever higher premiums were paid for growth stocks, which rose by almost 3% in the month while value stocks lost almost 2%.[2] The two top performing sectors were also an odd combination: first technology, then utilities.

While global stock markets as a whole were still up in mid-month, almost all were down by month end, with the notable exception of the Swiss SMI amongst the more prominent ones. U.S. markets only turned negative on January's last trading day, as heavyweights, especially in the technology sector, gave strong support to the indices. It used to take two of the U.S. giants to match the entire market value of the Dax; now just one is enough. A small comfort for Germany is that the German government gets its borrowing for less than nothing, paying minus 0.44% on its 10-year bonds, against a positive 1.53% yield at present on U.S. Treasuries. Italian government bonds are also giving their government a welcome break: the yield, which was at 1.41% at the beginning of the year, had dropped to 0.93% by the end of January. A regional election defeat for the right-wing Lega Nord Matteo Salvini may be the main reason.

Outlook and changes

Given last month's pronounced dichotomy – strong start, weak end – it is not surprising that there have been some changes at the tactical level. In equities we have taken the materials sector down to underweight. The sector's performance has been highly divergent (especially comparing chemicals to mining stocks), but overall has been weak for almost two years. This of course has made its valuation attractive compared to other sectors. But the economic stabilization, especially in the industrial sectors that we expect to see this year in Europe and Asia is now likely to be more difficult due to the spread of the coronavirus. It therefore remains unlikely that investors will change their sector and style preferences much in the near future. This means that cyclicals are likely to continue to await their big moment while sectors that have recently been strong are likely to remain so: solid, defensive growth stocks and so-called bond proxies, i.e. sectors such as utilities whose performance is closely linked to bond yields. As long as the markets continue not to expect any significant rise in interest rates in the medium term, we believe sector preferences are unlikely to change much.

This brings us to bonds. At the beginning of the month it still looked as if we would see a slight recovery in yields on the basis of the economic outlook, which has been stabilizing for a number of months, but this turned around as the month proceeded. Government-bond yields above all and, to some extent, investment-grade corporate yields fell significantly. However, yields on lower-rated corporate bonds in the high-interest segment rose in both the dollar and euro areas. We have adjusted tactically to the somewhat more nervous market sentiment and have returned all our positive signals to neutral. This includes corporate bonds in the United States and in Europe as well as emerging-market and Asia credit. We think it may be some time before investors' appetite to seek higher returns replaces the caution triggered by the coronavirus and supports these segments, on which we remain strategically positive.

On Bunds we go back to neutral after having expected yields to rise earlier on. In U.S. Treasuries we believe the correction has gone a little too far and we now expect yields to rise again, which is why we have set a negative signal for 10- and 30-year bonds. In Italy, on the other hand, we are moving to neutral. We believe that more than enough confidence on political developments in Italy is priced into the much lower yields.

As far as currencies are concerned, we are again betting tactically on a weakening of the euro against the dollar and the yen. Against the dollar mainly for market technical reasons, against the yen because we believe it should continue to be seen by investors as a safe haven in more turbulent times.

The multi-asset perspective

In the multi-asset sphere, too, market movements and political developments in January led to some adjustments. At the end of January, we came to the conclusion that investors' flight to safe havens, especially in government bonds, had gone a little too far and that demand could fall again in the coming weeks, with corresponding impacts on prices. We remain modestly skeptical on equities and believe prices could fall even further in the context of the coronavirus. A brightening in our tactical assessment would lead in particular to a higher weighting in emerging-market equities. Overall, we continue to expect markets to trade sideways. Any slump would be likely to be countered by an expansionary policy from central banks, helping to keep the global economy stable, while demanding valuations make an upward move equally unlikely. We must therefore continue to use short-term exaggerated moves in one direction or another as an opportunity to shift positions.

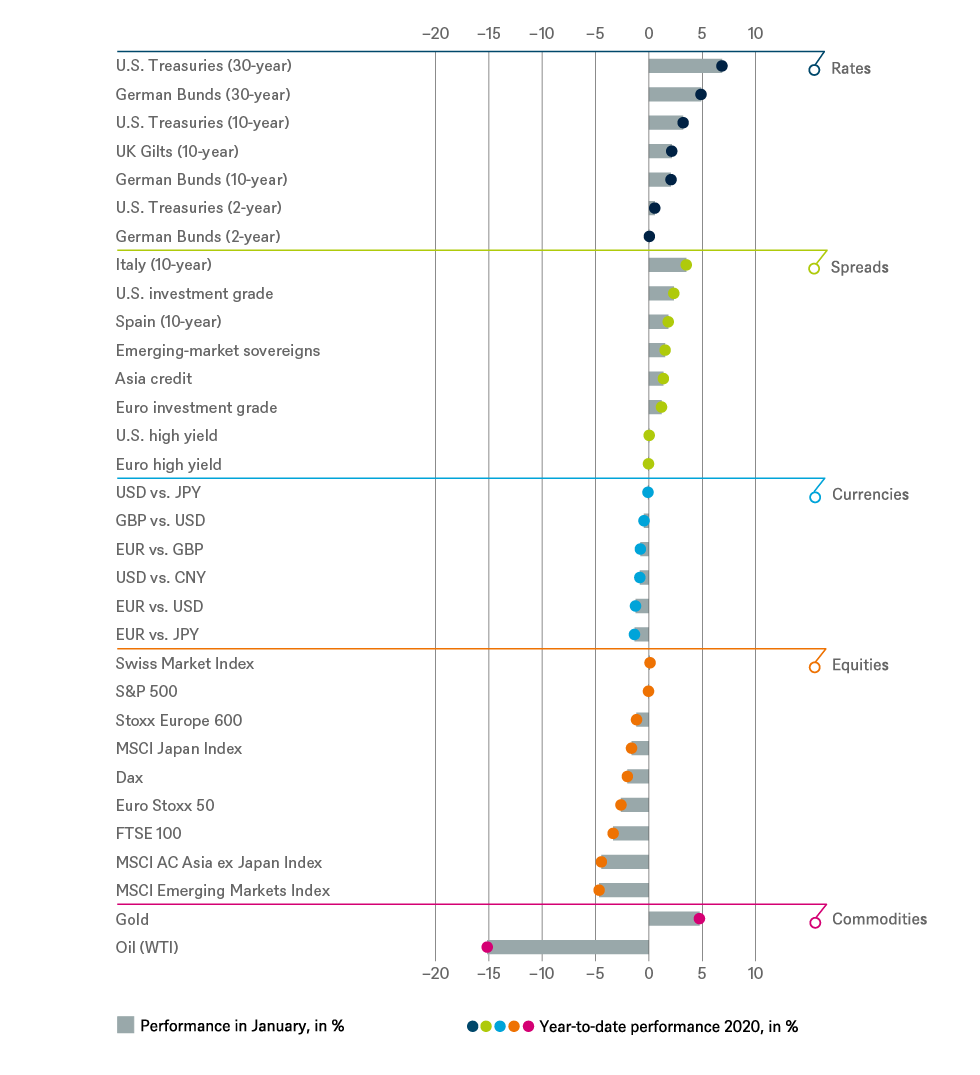

Past performance of major financial assets

Total return of major financial assets year-to-date and past month

Past performance is not indicative of future returns.

Sources: Bloomberg Finance L.P., DWS Investment GmbH as of 1/31/20

Tactical and strategic signals

Fixed Income

| Rates | 1 to 3 months | until December 2020 |

|---|---|---|

| U.S. Treasuries (2-year) | ||

| U.S. Treasuries (10-year) | ||

| U.S. Treasuries (30-year) | ||

| German Bunds (2-year) | ||

| German Bunds (10-year) | ||

| German Bunds (30-year) | ||

| UK Gilts (10-year) | ||

| Japan (2-year) | ||

| Japan (10-year) |

| Spreads | 1 to 3 months | until December 2020 |

|---|---|---|

| Spain (10-year)[3] | ||

| Italy (10-year)[3] | ||

| U.S. investment grade | ||

| U.S. high yield | ||

| Euro investment grade[3] | ||

| Euro high yield[3] | ||

| Asia credit | ||

| Emerging-market credit | ||

| Emerging-market sovereigns |

| Securitized / specialties | 1 to 3 months | until December 2020 |

|---|---|---|

| Covered bonds[3] | ||

| U.S. municipal bonds | ||

| U.S. mortgage-backed securities |

| Currencies | ||

|---|---|---|

| EUR vs. USD | ||

| USD vs. JPY | ||

| EUR vs. JPY | ||

| EUR vs. GBP | ||

| GBP vs. USD | ||

| USD vs. CNY |

Equities

| Regions | 1 to 3 months[4] | until December 2020 |

|---|---|---|

| United States[5] | ||

| Europe[6] | ||

| Eurozone[7] | ||

| Germany[8] | ||

| Switzerland[9] | ||

| United Kingdom (UK)[10] | ||

| Emerging markets[11] | ||

| Asia ex Japan[12] | ||

| Japan[13] |

| Style | |

|---|---|

| U.S. small caps[25] | |

| European small caps[26] |

Legend

Tactical view (1 to 3 months)

- The focus of our tactical view for fixed income is on trends in bond prices.

- Positive view

- Neutral view

- Negative view

Strategic view until December 2020

- The focus of our strategic view for sovereign bonds is on bond prices.

- For corporates, securitized/specialties and emerging-market bonds in U.S. dollars, the signals depict the option-adjusted spread over U.S. Treasuries. For bonds denominated in euros, the illustration depicts the spread in comparison with German Bunds. Both spread and sovereign-bond-yield trends influence the bond value. For investors seeking to profit only from spread trends, a hedge against changing interest rates may be a consideration.

- The colors illustrate the return opportunities for long-only investors.

- Positive return potential for long-only investors

- Limited return opportunity as well as downside risk

- Negative return potential for long-only investors

Appendix: Performance over the past 5 years (12-month periods)

| 01/15 - 01/16 | 01/16 - 01/17 | 01/17 - 01/18 | 01/18 - 01/19 | 01/19 - 01/20 | |

|---|---|---|---|---|---|

|

Asia credit |

2.3% |

5.7% |

4.3% |

1.7% |

10.7% |

|

Covered bonds |

0.7% |

1.0% |

0.4% |

1.2% |

3.5% |

|

Dax |

-8.4% |

17.7% |

14.3% |

-15.3% |

16.2% |

|

EM Sovereigns |

0.1% |

11.9% |

8.6% |

0.0% |

11.9% |

|

Euro high yield |

-1.8% |

12.0% |

5.7% |

-1.7% |

8.2% |

| Euro investment grade |

-1.0% |

3.5% |

2.7% |

0.1% |

6.4% |

| Euro Stoxx 50 |

-6.1% |

10.4% |

15.3% |

-9.2% |

19.3% |

| FTSE 100 |

-6.5% |

21.5% |

10.4% |

-3.6% |

9.3% |

| German Bunds (10-year) |

1.8% |

0.2% |

-1.3% |

5.6% |

4.3% |

|

German Bunds (2-year) |

0.3% |

-0.2% |

-0.9% |

-0.3% |

-0.5% |

|

German Bunds (30-year) |

-0.4% |

0.0% |

-1.3% |

10.3% |

12.1% |

|

Italy (10-year) |

4.3% |

-3.5% |

4.6% |

-0.4% |

14.9% |

|

Japanese government bonds (10-year) |

2.4% |

-0.1% |

0.4% |

1.4% |

0.4% |

|

Japanese government bonds (2-year) |

0.2% |

0.0% |

-0.3% |

0.0% |

-0.3% |

|

MSCI AC Asia ex Japan Index |

-18.2% |

21.2% |

43.5% |

-14.6% |

5.2% |

|

MSCI AC World Communication Services Index |

-6.7% |

3.1% |

4.7% |

-8.2% |

13.0% |

|

MSCI AC World Consumer Discretionary Index |

-3.0% |

12.0% |

28.2% |

-7.8% |

13.6% |

|

MSCI AC World Consumer Staples Index |

1.3% |

1.5% |

15.3% |

-9.7% |

13.0% |

|

MSCI AC World Energy Index |

-22.8% |

24.7% |

10.5% |

-10.7% |

-10.3% |

|

MSCI AC World Financials Index |

-12.9% |

24.1% |

26.5% |

-17.1% |

7.0% |

|

MSCI AC World Health Care Index |

-5.5% |

1.7% |

22.5% |

-0.3% |

13.3% |

|

MSCI AC World Index |

-8.6% |

15.5% |

25.1% |

-9.3% |

13.7% |

|

MSCI AC World Industrials Index |

-8.8% |

20.1% |

26.6% |

-13.0% |

12.5% |

|

MSCI AC World Information Technology Index |

-2.0% |

23.9% |

43.6% |

-6.6% |

38.2% |

|

MSCI AC World Materials Index |

-25.4% |

44.0% |

24.6% |

-16.6% |

2.4% |

|

MSCI AC World Real Estate Index |

-12.1% |

6.4% |

14.6% |

-2.2% |

7.8% |

|

MSCI AC World Utilities Index |

-10.7% |

2.7% |

9.2% |

4.1% |

17.4% |

|

MSCI Emerging Market Index |

-20.9% |

25.4% |

41.0% |

-14.2% |

3.8% |

|

MSCI Japan Index |

-1.7% |

15.7% |

25.0% |

-11.6% |

11.2% |

|

MSCI World Growth Index |

-3.8% |

12.0% |

29.7% |

-6.0% |

24.0% |

|

MSCI World Value Index |

-9.9% |

17.5% |

17.5% |

-10.8% |

7.2% |

|

Russel 2000 Index |

-11.2% |

31.5% |

15.7% |

-4.8% |

7.6% |

|

S&P 500 |

-0.7% |

20.0% |

26.4% |

-2.3% |

21.7% |

|

Spain (10-year) |

2.1% |

2.0% |

4.2% |

3.9% |

8.6% |

|

Stoxx Europe 600 |

-3.8% |

9.0% |

13.4% |

-6.1% |

18.7% |

|

Stoxx Europe Small 200 |

0.3% |

10.6% |

20.3% |

-7.2% |

18.0% |

|

Swiss Market Index |

2.2% |

3.3% |

16.3% |

-0.6% |

22.5% |

|

U.S. high yield |

-6.6% |

20.8% |

6.6% |

1.7% |

9.4% |

|

U.S. investment grade |

-3.0% |

5.4% |

4.8% |

0.9% |

14.0% |

|

U.S. MBS |

-36.4% |

4.8% |

13.6% |

28.0% |

50.0% |

|

U.S. Treasuries (10-year) |

0.6% |

-2.0% |

0.2% |

3.9% |

11.2% |

|

U.S. Treasuries (2-year) |

0.6% |

0.4% |

0.0% |

2.1% |

3.9% |

|

U.S. Treasuries (30-year) |

-4.4% |

-3.4% |

4.7% |

2.1% |

21.9% |

|

UK Gilts (10-year) |

0.9% |

3.2% |

0.8% |

4.2% |

6.6% |

Source: Bloomberg Finance L.P., DWS Investment GmbH as of 2/3/20

Past performance is not indicative of future returns.

1. Source: https://www.cnbc.com/2020/01/31/fridays-massive-sell-off-ruins-january-barometer-market-signal.html as of 1/31/20

2. As measured by the MSCI AC World Growth Index and the MSCI AC World Value Index.

4. Relative to the MSCI AC World Index

5. S&P 500

7. EuroStoxx 50

8. Dax

10. FTSE 100

11. MSCI Emerging Markets Index

12.

MSCI AC Asia ex

Japan Index

13. MSCI Japan Index

14. MSCI AC World Consumer Stables

15. MSCI AC World Health Care Index

16. MSCI AC World Communication Services Index

17. MSCI AC World Utilities Index

18. MSCI AC World Consumer Discretionary Index

19. MSCI AC World Energy Index

20. MSCI AC World Financials Index

21.

MSCI AC World

Industrials Index

22. MSCI ACWI Information Technology Index

23. MSCI AC World Materials Index

24. MSCI AC World Real Estate Index

25. Russel 2000 Index relative to the S&P 500

26.

Stoxx Europe Small 200 relative to the Stoxx

Europe 600

27.

Relative

to the Bloomberg Commodity Index