The new Coronavirus Covid-19 has paralyzed the world at such a speed that, in the short term, even comparisons with Fukushima, 9/11 or the financial crisis appear insufficient. In order to cope with the exponential spread of the virus, all industrialized countries have had to effectively freeze large swaths of economic and social life. It is difficult to estimate how great the economic damage will be, but it is likely to be considerable. These necessary containment measures have plunged global economic activity into a sharp recession in record time.

We want to make an initial attempt to quantify the extent of the economic damage caused by the preventive measures currently in place, the means by which further countermeasures can and should be assessed and the size of fiscal rescue packages. Of course, the situation remains fluid. Our goal is less to exactly quantify the impact than to provide some rough rules of thumb of what to watch out for and how the likely consequences should be assessed.

The economic damage is caused primarily by the fact that in order to prevent a large number of new infections with the novel Coronavirus (or more precisely: to spread their occurrence over time) the economic and social interactions of a large part of humanity have been severely limited. Numerous countries are in a lockdown mode: curfews have been issued in an ever growing list of countries and territories. At the time of writing, the list includes large parts of the United States, Italy, France and Spain. In Germany, all public events have been banned, all shops deemed not "systemically important" have been closed, international air traffic has largely been suspended and the free movement of goods is severely restricted.

Many of these emergency measures may be necessary for health reasons until more effective medical remedies and practices to combat the threat can be developed and deployed in coming months. The crisis could certainly have been managed with less economic and social collateral damage if there had been better and more internationally coordinated health-policy responses early on. The same is probably true of the fiscal and monetary measures currently being discussed or already passed. Ideally, these should be coordinated at the G7 or, better still, the G20 level. Restrictions in international travel, interest-rate cuts and announcements of fiscal pacts could all have been better coordinated among the actors. Unfortunately, the crisis is hitting the world at a time when populist and protectionist measures had already been gaining traction.

Moreover, from a global perspective, the pendulum between "freedom" and "security" has now swung a long way in the direction of "security." This, too, tends to lead to measures that have a serious impact on society and the economy.

Economic impact: A deep global recession

It is difficult to quantify the effects of the numerous measures, not least since they are constantly changing. An initial indication of how the protective steps taken are affecting various sectors can be obtained from China. It is not only the manufacturing industry that is suffering, but also the service sector. Overall, figures from China paint a frightening picture: Trade in passenger cars was down by around 80% from February 2019, industrial production fell by 13% and retail sales by 22%.

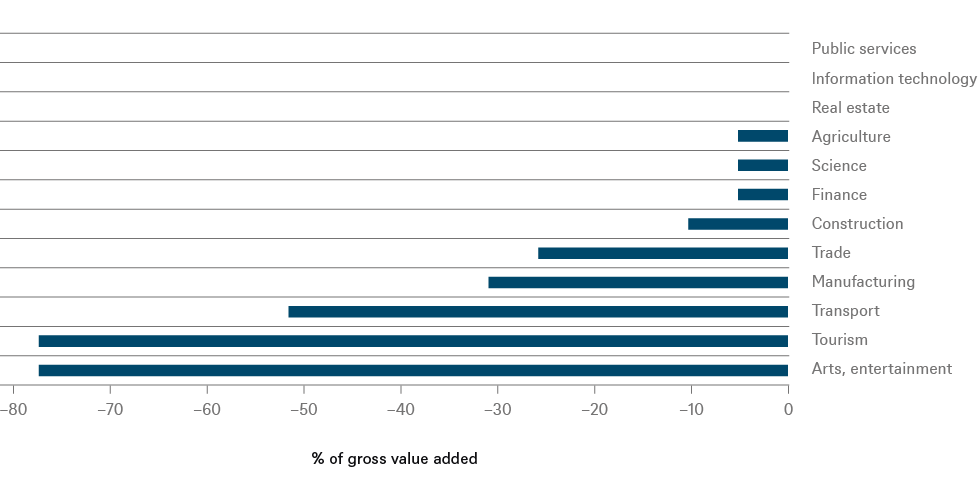

Figure 1 provides an illustration of how individual sectors might be affected in the Eurozone. Some sectors are unlikely to suffer any significant losses – most obviously, providers of medical equipment have already seen a spike in demand, though, of course, they too may suffer from Covid-19 shocks to their supply chain. Other sectors have been hit extremely hard: above all tourism and the entire arts and culture sector, which had to cease operations overnight.

Trade and manufacturing, too, have been hit to a very considerable extent. If these losses are added up for the Eurozone, the result is likely to be a loss of over 17% of the gross domestic product (GDP). This takes into consideration the weight of individual sectors during normal times. As a rule of thumb, we estimate that around 1.5% of the annual GDP will be lost per month while the Eurozone largely remains in lockdown. Individual EU member states are affected to varying degrees. Germany, for example, is hit harder because the manufacturing industry accounts for a larger share of total value added. Italy and Spain, on the other hand, suffer more because tourism is coming to a standstill, which accounts for a larger share of GDP there.

Fig. 1: Estimated loss of gross value added due to Covid-19

Source: DWS Investment GmbH as of 3/20/20

In general, it makes sense to differentiate between the world's three big economic regions (China, the United States and Europe). Their local economic systems are structured differently, as are their countermeasures. That is partly, but not solely, a result of the course the pandemic itself has taken. China, for example, is already able to slowly ramp up its production again, but in doing so is encountering reduced demand from the rest of the world. By contrast, the lockdown in Europe and the U.S. has only just begun. However, the extent of the impact appears to be similar for all regions. As a rule of thumb, one can deduct around 1.5% of annual GDP per month of lockdown.

The progression

We believe the crucial question therefore is how long the now adopted measures will last and whether they might become even more severe. We assume that, in Europe, the current countermeasures will be maintained until May, at the latest. A certain normalization of circumstances should therefore show up in the third quarter.

Various reasons for this assumption should be considered: Most obviously, the number of new infections may begin to fall, not least because of the measures themselves. In addition, there is still a small hope that warmer temperatures may slow the virus – as is typically the case with most flu epidemics caused by (unrelated) influenza viruses. We caution, though, that such hopes are highly uncertain, as so much about Covid-19 remains unknown. In any case, summer temperatures alone are unlikely to eliminate the virus. By autumn at the latest, or when economic activity resumes, the number of infections could rise again.

A vaccine would have to be sufficiently tested before it could be administered to millions upon millions of people. That will almost certainly take at least a year. A drug that alleviates the effects of the disease is not yet in sight, but could be subject to an accelerated approval procedure. In the short term, however, the most important thing would be to have more widely available tests so that larger sections of society can be tested and virus carriers, and their contacts, can be isolated more quickly. This was one of the most important building blocks in facilitating a rapid response to the pandemic in Singapore and Taiwan.

However, policymakers cannot rely on such progress for the time being, which is why we believe the existing exceptional measures are likely to remain in place for some time to come. But neither can they last forever: in a liberal society, the suspension of almost all basic political and civil rights (freedom of movement, freedom of assembly, the right to education, to the undisturbed practice of religion and the free exercise of professions) is tricky for long periods of time. The founding father of German hygiene research, Max von Pettenkofer, said that no epidemic could be so bad that one could permanently suspend or freeze civil society.[1]

In addition, from a certain point on, the economic damage caused by a policy geared exclusively to fighting the virus would no longer be socially acceptable. If the lockdown in the Eurozone were to continue for a whole year, economic output would have to be expected to fall by 17% compared with the previous year, and if second-round effects were taken into account, it would certainly be possible for the slump to be far greater. Unemployment would likely rise massively, and a banking and also a public-debt crisis might well follow.

There is a bigger, underlying reason, though, why we currently expect the most severe containment measures to remain in place for a maximum of two months and to be gradually relaxed after that. As a German saying goes, desperation is the mother of innovation. In past wars and other crises, democratic and (in normal times) open societies with free market economies have frequently proven surprisingly resilient. Citizens, business and various government agencies learn over time, including from the example of other countries. Currently, the best practices include not just testing and contact tracing, but the very blunt instruments of curfews and lockdowns. As time passes, we believe more precise, milder and less economically costly forms of social distancing are likely to emerge. In this battle of "human vs. virus" we would firmly place our bets on human innovation and resilience.

Meanwhile, we feel the current severe countermeasures provide valuable time to expand the health-care infrastructure. If, for example, the treatment options improve and there is a sufficiently large number of tests, then the measures could be restricted to those people who are actually infected and their immediate surroundings.

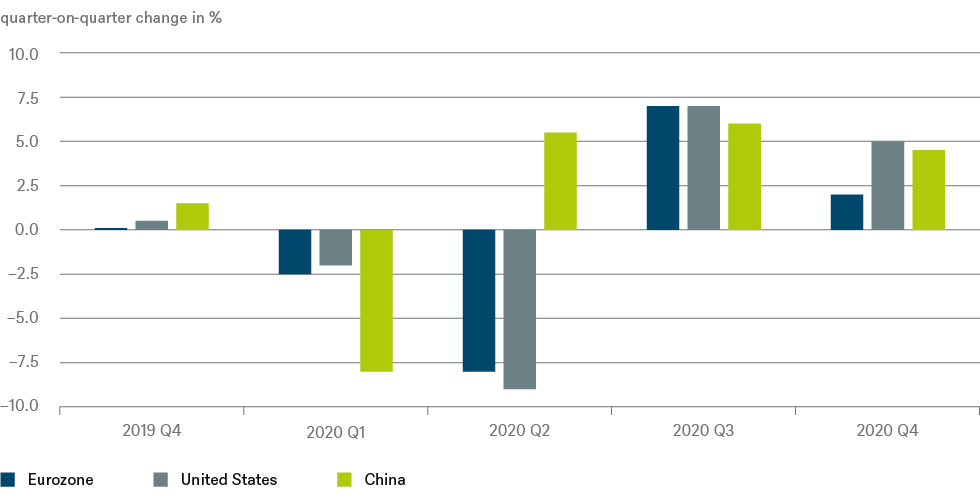

Fig. 2: GDP growth rates

Sources: Haver Analytics Inc, DWS Investment GmbH as of 3/20/20

This should result in a growth picture that stands to be more moderate than many other, more pessimistic scenarios currently circulating. One must assume a sharp recession in China in the first quarter, and this recession is virtually travelling around the world alongside the rapid spread of the virus we have all been witnessing. In Europe and the U.S., we believe the recession will most probably start at the end of the first quarter.

Overall, the first quarter should have been only slightly affected in western industrialized countries. We believe the full impact of the "shock freeze" on the economy will only be seen in the second quarter. We currently assume that the lockdown in most industrialized countries will last for a total of two months and the subsequent thawing phase will last for around three months. We expect only quite moderate growth rates for this period after the most severe virus-containment measures are lifted. It will take some time before production can be ramped up – in addition, demand from partner regions will be weak. The annual growth rates for the three regions in such a scenario are clearly negative. We expect economic output in the Eurozone to decline by around 5% in 2020.

For the U.S., we expect a decline of 3.5%. There, the rise in unemployment is likely to be more pronounced due to very weak protection against dismissal. This will probably have a greater impact on consumption there than in European countries. Consumer spending is also likely to be impacted by the fall in share prices through stronger wealth and sentiment effects. However, we believe the subsequent upswing could be somewhat more dynamic again, as the U.S. has one of the most flexible economies in the world and may more quickly be able to seize new business opportunities the post-Covid-19 world might offer.

In China, the Coronavirus crisis has taken its huge economic toll during the entire first quarter. However, we expect the recovery to start in the second quarter. For the full year, China looks set to achieve some growth, probably about 2%. In this scenario, the global economy would swiftly slide into a recession, but experience a rebound in the second half of 2020, instead of a full-blown, prolonged depression.

Our scenario, although quite plausible as things stand at present, could of course prove to be too optimistic or too pessimistic. Governments and central banks are supporting the economy with substantial rescue packages. State institutions are certainly undergoing an extraordinary stress test at the moment, and the conditions for internationally coordinated cooperation have been better. Nonetheless, Western democracies have repeatedly proven their ability to act in the past, even if, especially in times of crisis, not always as quickly as financial markets had hoped.

Fiscal policy: Sharp rise in government debt

We expect the lockdown to lead directly to a massive increase in unemployment. This in turn should lead to a sharp decline in private consumption. Subsequent corporate bankruptcies could drag banks and even states into the abyss. Although the Coronavirus crisis should ultimately be temporary by nature, the question arises as to how many companies will be able to survive the forced slumber. In our view, only fiscal policy can limit the economic damage.

The immediate question is: how much money does the state have to spend to contain the crisis? A simple calculation can provide a rough idea. The fallout could be reduced to virtually zero if government spending were to make up for every activity cancelled due to Covid-19. Imagine a special Coronavirus government agency, which simply bears the costs of all cancelled meals and hotel bookings, as well as paying airlines the full passenger revenue at this time of year for keeping their planes grounded, instead of flying. The owners of empty theatres, cinemas and bars would similarly be reimbursed by this hypothetical agency.

This is unrealistic, of course, but it gives you an idea of the scale of the programs required: they would need to be roughly equivalent to the forgone GDP. We estimate that the Eurozone economy will shrink by about 5% this year. The bailout packages would have to roughly fill this gap, i.e. have an equally high volume. This would cause public debt in the Eurozone to rise by around 5% of GDP in each member state - and that would come on top of new debt issuance already planned before the crisis. A similar order of magnitude probably also applies in the U.S. In addition, gross domestic product would still fall in real terms, so that the national debt ratio could well rise by 10 or more percentage points. This is due to the fact that when calculating the government debt ratio, both the higher new debt issuance and the fall in GDP need to be taken into account.

The packages of measures currently being discussed or already launched certainly point in the right direction: short-time working allowances, tax deferrals, bridging loans for small and medium-sized enterprises. These are similar to the replacement measures we mentioned in the above thought experiment. One could also envisage issuing a Corona bond for the Eurozone, for which all member states would be jointly liable. Given the size of the task to be solved, this is a thoroughly plausible idea.

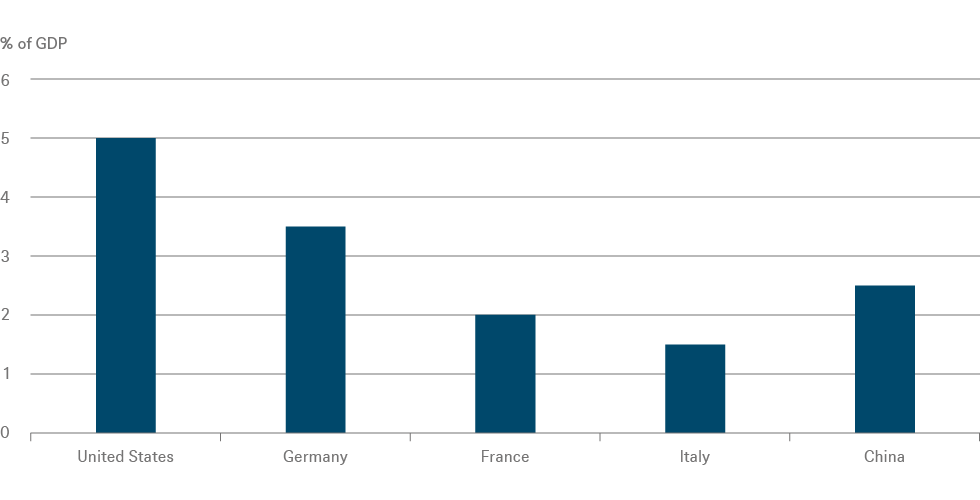

In the U.S., the rescue packages have a funding volume of around 5%.[2] The corresponding packages in Europe – especially in Italy and France – do not seem to be of the required size yet (see Fig. 3). They will probably continue to grow in the coming weeks.

Fig. 3: Estimated funding volume of Coronavirus-related fiscal packages*

* already adopted or in the parliamentary process – without guarantees

Source: DWS Investment GmbH as of 3/20/20

With the clean-up work that will follow, it could prove helpful that this time it is a truly global crisis, triggered by an external shock, with no clearly identifiable culprit. This should be helpful in the long term for crisis management based on solidarity. In Europe, the question of debt sustainability will most likely arise sooner or later – especially for Italy. The demand for a common solution looks set to gain further prominence, for example by issuing Corona bonds. The idea is quite plausible: given the size of the problems that are already pending, another euro crisis is the last thing European policymakers would want to have on their crowded agenda.

Monetary policy: interest rates at or below zero, asset purchases and unlimited liquidity

In this crisis, monetary policy can neither address the causes nor combat the immediate consequences. But it can support fiscal policy by keeping credit markets liquid and ensuring that companies can "hibernate" the crisis. In the meantime, major central banks have pulled out all the stops. Taken together, their monetary-policy measures are truly unprecedented. Interest rates are virtually at zero, central banks are providing the banks with basically unlimited liquidity, and they are buying bonds on a large scale, including corporate bonds, which should help calm credit markets. These measures are likely to remain in force for quite a while, partly because of the duration of the aforementioned clean-up operation and partly because inflationary pressures are likely to remain subdued for now: in the short and medium term, the pandemic is certainly deflationary because demand is initially more affected than supply. Admittedly, it cannot be ruled out, or indeed must be assumed, that production potential will also be negatively impacted by the crisis. Probably, sometime will have passed, though, before this is felt in production and is released in corresponding inflation pressures.

To summarize

Despite the difficulty to predict how the virus will spread and what countermeasures governments will take: In this battle of "human vs virus" we would firmly place our bets on human innovation and resilience. We believe the solution may come from better treatment options for patients, from a vaccine or – the most promising at present - from improved testing options. As time passes, more precise, milder and less economically costly forms of social distancing are likely to emerge.

Nobody can say what the world will look like after the Covid-19 shock has passed. However, governments are currently making every effort to contain the economic "fallout". This could well succeed. We remain cautiously optimistic that in a year's time, humanity will again be more confident about the future than it is today.

1. Quoted in: https://www.spiegel.de/gesundheit/coronavirus-medizinhistoriker-ueber-parallelen-der-corona-epidemie-zu-frueheren-seuchen-a-3bab7496-ff0b-4a4d-a8d5-43ed4beb7aa8

2. In addition, there are guarantees of a similar magnitude, which may or may not be drawn.