Market overview

It would be nice to be able to write the March review in the past tense. How shocked citizens, politicians and investors initially were by the sudden spread and the consequences of the new coronavirus, SARS-CoV-2 and the disease it triggered, COVID-19. And how, after successful public health efforts and bold intervention by governments and central banks, the worst is now behind us. But unfortunately the past tense is very much premature. The coronavirus storm is still in its early days. The disease is still developing very dynamically, especially in the world's leading economy, the United States, and is also now spreading to numerous emerging markets. Although no more than 100 cases were recorded in the United States at the beginning of March, by the end of the month there were already more than 4,000 deaths. In addition to the poor state of the U.S. public health system, lack of preparation was a major contributing factor. As late as end of February, President Trump said that the virus could be controlled in the United States and that the S&P 500 was beginning to look very good to him.[1] About a month later, he told his countrymen that they would have to expect restrictions on movement until the end of April and probably 100 to 240 thousand deaths. This crisis management has not hurt Trump so far; he has even been able to gain ground in opinion polls.[2] One reason might be his daily on-screen presence, as he himself tweeted.[3] Meanwhile, the situation in New York looks particularly dire, partly because more and more doctors and nurses are becoming infected due to a lack of protective equipment.[4] In other large U.S. cities, too, the number of cases and deaths is skyrocketing.

But it was in Europe, not China itself, the originating country of the virus, that the global alarm bells first started ringing. The quarantine imposed in Italy on March 9 subsequently caused other countries to go into crisis mode. Already in the final week of February, stock markets worldwide had begun to tumble at unprecedented speed, bringing the longest ever rally (some 11 years) in the S&P 500 to an end. Stock-market volatility in Europe and the United States even exceeded the record levels of 2008. A further negative development for stocks was that Russia and Saudi Arabia entered a price war at the beginning of March, with Saudi Arabia opening the taps to punish Russia for non-compliance with OPEC quotas. As a result the price per barrel of West Texas Intermediate (WTI) fell below 20 dollars, a drop of about two-thirds since January and the lowest level in 18 years. On March 9, for the first time in history, all U.S. government-bond maturities yielded less than 1%. Toward the end of the month, yields at the short end, below six months, even fell into negative territory. The major central banks reacted in an unusually rapid and resolute manner, bringing most key interest rates close to zero and supporting the bond markets with bond purchases and large-scale liquidity measures. In the Eurozone, the European Central Bank (ECB) made it easier for banks to lend via numerous channels. Finally, fiscal packages, worth trillions, have complemented the monetary rescue measures. The record number of 3.3 million unemployment claims in the United States on March 26 (the previous weekly record was 0.7 million in 2008) indicates just how necessary these emergency responses were.

The course of the pandemic, as well as the extent and duration of government measures to contain it, will determine the direction of markets in coming months in our view, more than the central banks and fiscal emergency packages. The virus still poses enough questions even for professional virologists, still more for politicians and investors. Everyone is at a learning phase and some misjudgments are inevitable. As asset managers we continue to work with core and risk scenarios, incorporating new findings into our models and prepared to revise our opinion if the data or assessment changes.

We currently assume that the extensive international lockdown of society and the economy will continue into May. The subsequent defrosting will take place in small steps, and it will be another two months before the economy returns to more or less normal capacity utilization.

This would mean that the Eurozone and U.S. economies would be likely to contract by around 3% to 5% this year. But there are many question marks. Will there be a second wave of contagion in autumn? And how strongly would policymakers react to it? In addition, there is the question of what other domino effects could result from corporate or even state bankruptcies? We are particularly concerned about countries whose economies are heavily dependent on exports, especially oil, and tourism. But we are also worried about Italian public debt, which is likely to get out of hand, and the stress this may place on the unity of the Eurozone. We are also looking at China and the question of whether the government there cannot or does not want to implement a larger fiscal package. In the longer term we will again be dealing with fundamental questions of debt sustainability in all nations and the outlook for inflation and yields.

In the short term, however, the virus remains the focus. The infection and death rates, medical progress in combatting the illness, and society's ability to manage the epidemic are all going to be crucial. We currently face a time in which that frequently repeated phrase, 'increased uncertainty,' can rightly be pronounced. But uncertainty embraces the potential for both bad as well as good surprises. Necessity is the mother of invention, and mankind is adaptable and resourceful, and seldom has so much effort been exerted to solve a problem, and not only from the medical side.

Outlook and changes

We believe that the pattern of the virus's spread and the degree of success of measures to contain it will be decisive for the markets in the coming weeks. The monetary and fiscal-aid packages will keep markets going and provide some downward protection. The practical implementation of these packages may reveal many shortcomings and we believe that despite their impressive scale they might not be the final step. They are essentially designed above all to cushion the immediate negative consequences of the lockdowns on companies and people. They may not therefore constitute an economic stimulus package.

Short-term assessment of the individual asset classes is currently so difficult, not only because of the further unknowns where the virus is concerned, but also because of numerous market anomalies. Many sub-markets are still suffering from low liquidity and individual stress indicators are still near record levels. Moreover, central banks' purchases of only certain securities are in reality dividing the market in two.

Equity: The revisions to analysts' consensus earnings estimates still look modest. They were in the single-digit percentage range from the beginning of the year. We, however, expect declines in earnings of over 20% for the current year. It is now apparent that global economic activity and corporate profitability peaked in 2019. A new economic cycle is beginning, starting with a downturn. The 30% - 40% correction that has taken place in equity markets already prices in a lot of bad news. But whether all of the bad news is priced in depends on one's assumptions. If the economic lockdown is indeed gradually eased after the Easter holidays we would expect the equity markets to trade above current market levels in a year's time. But the dynamics of the virus will be the key determinant.

Virtually all sectors are being negatively affected by the crisis, albeit to different degrees, which offers opportunities for targeted stock selection. Tourism, airlines and restaurants face existential challenges. The oil sector is having to deal simultaneously with the dual challenge of increased supply and decreasing demand. Banks will have to increase loan provisions and will record even lower net-interest income. However, in general global banks are in much better shape than in 2008.

Whatever the longer-term market outcome, short-term volatility is likely to remain very high, and new lows are possible. While the Dax plunged in mid-March to a low that was only around two hundred points above its book value of 8200, the sell-off in the United States still left the S&P 500 at around 2.5 times book value. Furthermore, we do not expect a rapid, pronounced recovery in the markets.

We do not have strong regional equity preferences at this time. We continue to favor blue chips in the United States and small caps in Europe, and high-quality companies with strong balance sheets and relatively resilient cash flows. Our sector preferences derive from this. Sales and earnings profiles already speak in favor of technology stocks, and now their strong balance sheets are another important factor. The crisis could even accelerate the trends toward digitalization, as home working, video conferencing and online shopping create some new niche opportunities. Healthcare remains our preferred defensive sector. We maintain our underweight in commodities, even though valuation levels in this sector have already fallen sharply.

Fixed Income: The bond market also remains strongly influenced by the coronavirus and the emergency monetary and fiscal packages. Compared to the high peaks in spreads and volatility in mid-March, many sub-markets are now in much better shape. We are neutral on U.S. government bonds, positive on most corporate bonds and also neutral on sovereign and corporate emerging-market bonds.

U.S. Treasuries are once again proving to be a sought-after asset class where short-term liquidity can be parked, as evidenced by strong foreign demand. The yield on 10-year bonds is currently at around 0.6%, close to its record low. However, we keep them at neutral because we believe sentiment in the United States could become even gloomier during the lockdown. This could overshadow for the time being the upward push on yields that new government financing needs are likely to bring. We see the danger of something similar in Germany, with even more negative sentiment driving yields down, but we expect them to rise again over the next three months. While the German government is likely to step up its bond issuance significantly, the ECB is likely to prioritize other countries in its bond purchases. On the Eurozone periphery countries we are split, after their yield spreads to Bunds have already tightened again. We keep Italy on neutral but see Spain, tactically, positive. Despite all the pressure from the coronavirus crisis and the level of new debt required, the ECB's 750 billion euro purchase program (Pandemic Emergency Purchase Program - PEPP) is likely to keep a lid on yield spreads in the Eurozone periphery.

In the case of corporate bonds, there is currently an enormous level of issuance, despite the fact that risk premiums are still high and liquidity is low. This supply is still being well received by the market. In Europe, we take a positive view of both investment-grade and high-yield bonds. Although we expect the rating agencies to issue downgrades much faster this time, the markets have already anticipated much of this in their mid-March sell-off. ECB purchases are also providing support. In the United States, however, we are more cautious in the investment-grade sector, and are neutral.

Many emerging markets are currently suffering from a combination of blows: a strong dollar, weak oil prices, a slump in global trade and tourism, and greater risk aversion among investors. While emerging markets will not be all equally affected by the coronavirus and liquidity shortages, the market is currently not very differentiated, so we are neutral overall.

The multi-asset perspective

In the multi-asset sector we maintain our marginally constructive stance on portfolio risk. Even though we expect high volatility and possibly new lows in the near future, we assume that uncertainty, in terms of the lack of understanding of the coronavirus, will be decreasing in a few weeks. We expect a better idea of how things are going to develop to have a positive impact on riskier asset classes, especially equities. Our preferred regions remain the United States and emerging markets.

Meanwhile we have become more cautious on the bond sector. We believe that the investor flight into government bonds caused by the coronavirus crisis and the associated drop in yields has gone a little too far. Sooner or later the unprecedentedly high monetary and fiscal stimulus that has been introduced will put upward pressure on yields, especially at the long end of the yield curve. Even though we see some opportunities in corporate bonds, we are currently paying increased attention to the liquidity of individual bonds. Furthermore we are holding a higher than normal level of cash in order to have maximum flexibility should markets become shaky again.

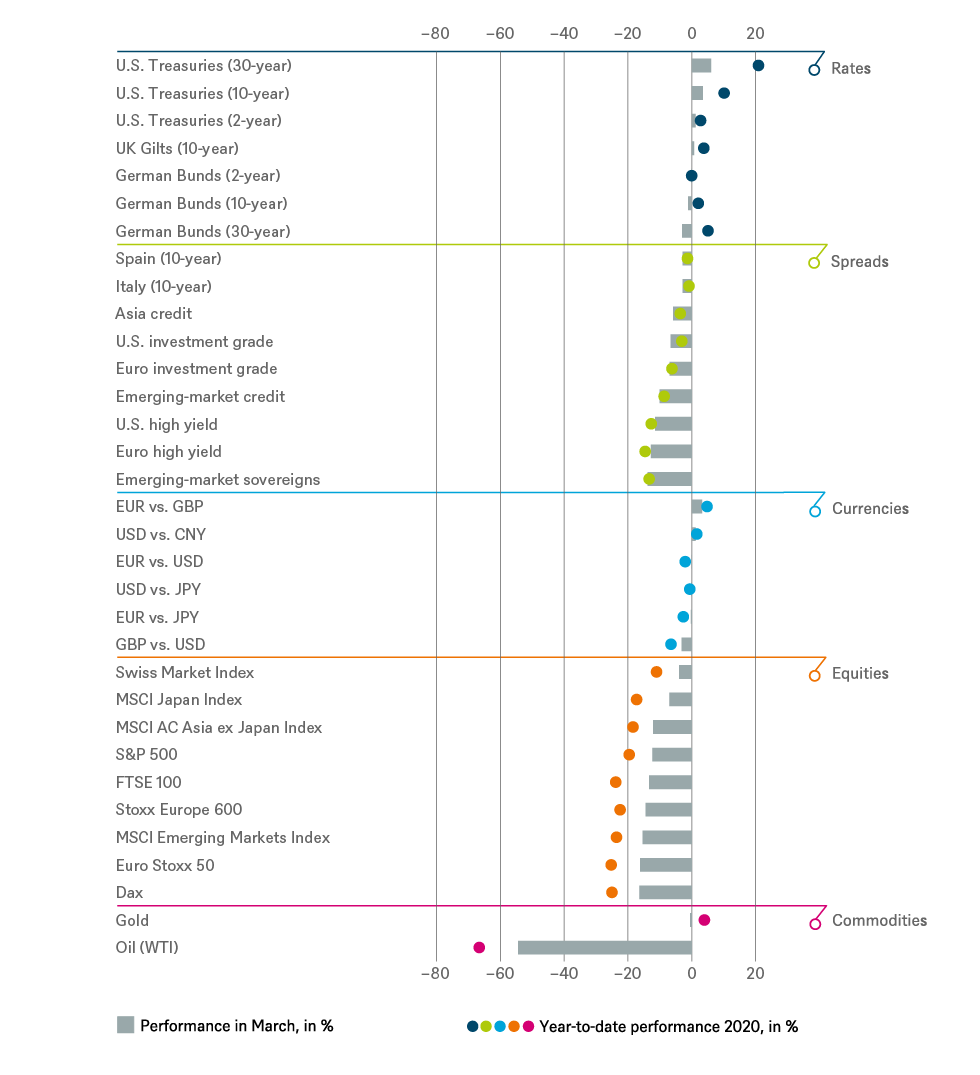

Past performance of major financial assets

Total return of major financial assets year-to-date and past month

Past performance is not indicative of future returns.

Sources: Bloomberg Finance L.P., DWS Investment GmbH as of 3/31/20

Tactical and strategic signals

Fixed Income

| Rates | 1 to 3 months | until March 2021 |

|---|---|---|

| U.S. Treasuries (2-year) | ||

| U.S. Treasuries (10-year) | ||

| U.S. Treasuries (30-year) | ||

| German Bunds (2-year) | ||

| German Bunds (10-year) | ||

| German Bunds (30-year) | ||

| UK Gilts (10-year) | ||

| Japan (2-year) | ||

| Japan (10-year) |

| Spreads | 1 to 3 months | until March 2021 |

|---|---|---|

| Spain (10-year)[5] | ||

| Italy (10-year)[5] | ||

| U.S. investment grade | ||

| U.S. high yield | ||

| Euro investment grade[5] | ||

| Euro high yield[5] | ||

| Asia credit | ||

| Emerging-market credit | ||

| Emerging-market sovereigns |

| Securitized / specialties | 1 to 3 months | until March 2021 |

|---|---|---|

| Covered bonds[5] | ||

| U.S. municipal bonds | ||

| U.S. mortgage-backed securities |

| Currencies | ||

|---|---|---|

| EUR vs. USD | ||

| USD vs. JPY | ||

| EUR vs. JPY | ||

| EUR vs. GBP | ||

| GBP vs. USD | ||

| USD vs. CNY |

Equities

| Regions | 1 to 3 months[6] | until March 2021* |

|---|---|---|

| United States[7] | ||

| Europe[8] | ||

| Eurozone[9] | ||

| Germany[10] | ||

| Switzerland[11] | ||

| United Kingdom (UK)[12] | ||

| Emerging markets[13] | ||

| Asia ex Japan[14] | ||

| Japan[15] |

| Style | |

|---|---|

| U.S. small caps[27] | |

| European small caps[28] |

Legend

Tactical view (1 to 3 months)

- The focus of our tactical view for fixed income is on trends in bond prices.

- Positive view

- Neutral view

- Negative view

Strategic view until March 2021

- The focus of our strategic view for sovereign bonds is on bond prices.

- For corporates, securitized/specialties and emerging-market bonds in U.S. dollars, the signals depict the option-adjusted spread over U.S. Treasuries. For bonds denominated in euros, the illustration depicts the spread in comparison with German Bunds. Both spread and sovereign-bond-yield trends influence the bond value. For investors seeking to profit only from spread trends, a hedge against changing interest rates may be a consideration.

- The colors illustrate the return opportunities for long-only investors.

- Positive return potential for long-only investors

- Limited return opportunity as well as downside risk

- Negative return potential for long-only investors

Appendix: Performance over the past 5 years (12-month periods)

| 03/15 - 03/16 | 03/16 - 03/17 | 03/17 - 03/18 | 03/18 - 03/19 | 03/19 - 03/20 | |

|---|---|---|---|---|---|

|

Asia credit |

4.1% |

4.8% |

1.7% |

5.5% |

2.3% |

|

Covered bonds |

0.7% |

0.5% |

0.6% |

1.9% |

1.1% |

|

Dax |

-16.7% |

23.6% |

-1.8% |

-4.7% |

-13.8% |

|

EM Credit |

2.9% |

9.7% |

3.3% |

5.2% |

-1.4% |

|

EM Sovereigns |

4.2% |

8.9% |

4.3% |

4.2% |

-6.8% |

|

Euro high yield |

-0.6% |

9.5% |

3.8% |

2.1% |

-10.2% |

| Euro investment grade |

0.4% |

2.5% |

1.7% |

2.3% |

-3.4% |

| Euro Stoxx 50 |

-15.9% |

21.4% |

-1.0% |

3.4% |

-13.9% |

| FTSE 100 |

-5.3% |

23.4% |

0.2% |

7.6% |

-18.4% |

| German Bunds (10-year) |

2.1% |

-0.1% |

-0.4% |

5.5% |

2.6% |

|

German Bunds (2-year) |

0.1% |

-0.2% |

-0.8% |

-0.4% |

-0.6% |

|

German Bunds (30-year) |

-0.9% |

-2.3% |

0.2% |

10.9% |

8.9% |

|

Italy (10-year) |

3.1% |

-4.3% |

6.7% |

-2.1% |

9.1% |

|

Japanese government bonds (10-year) |

4.3% |

-0.8% |

0.5% |

1.6% |

-0.6% |

|

Japanese government bonds (2-year) |

0.4% |

-0.2% |

-0.2% |

0.0% |

-0.3% |

|

MSCI AC Asia ex Japan Index |

-11.9% |

17.5% |

25.8% |

-5.2% |

-13.4% |

|

MSCI AC World Communication Services Index |

-0.4% |

-2.6% |

-3.8% |

1.2% |

-7.4% |

|

MSCI AC World Consumer Discretionary Index |

-3.4% |

9.7% |

15.6% |

1.3% |

-12.4% |

|

MSCI AC World Consumer Staples Index |

5.4% |

1.8% |

2.4% |

2.5% |

-8.0% |

|

MSCI AC World Energy Index |

-17.2% |

12.2% |

3.8% |

-0.2% |

-46.7% |

|

MSCI AC World Financials Index |

-13.1% |

21.5% |

13.7% |

-10.3% |

-24.4% |

|

MSCI AC World Health Care Index |

-9.7% |

6.6% |

8.2% |

9.3% |

-0.8% |

|

MSCI AC World Industrials Index |

-3.6% |

13.9% |

13.1% |

-2.7% |

-19.5% |

|

MSCI AC World Information Technology Index |

0.7% |

23.4% |

28.1% |

7.3% |

5.5% |

|

MSCI AC World Materials Index |

-14.4% |

23.3% |

13.4% |

-5.9% |

-23.5% |

|

MSCI AC World Real Estate Index |

-2.8% |

-0.3% |

5.4% |

7.9% |

-21.3% |

|

MSCI AC World Utilities Index |

1.8% |

0.9% |

2.4% |

9.1% |

-8.5% |

|

MSCI Emerging Market Index |

-12.0% |

17.2% |

24.9% |

-7.4% |

-17.7% |

|

MSCI Japan Index |

-7.1% |

14.4% |

19.6% |

-7.8% |

-6.7% |

|

Russel 2000 Index |

-11.1% |

24.4% |

10.4% |

0.7% |

-25.1% |

|

S&P 500 |

1.8% |

17.2% |

14.0% |

9.5% |

-7.0% |

|

Spain (10-year) |

1.3% |

1.3% |

6.2% |

3.0% |

3.4% |

|

Stoxx Europe 600 |

-12.3% |

17.0% |

0.4% |

5.9% |

-12.6% |

|

Stoxx Europe Small 200 |

-6.0% |

16.1% |

7.2% |

1.5% |

-15.3% |

|

Swiss Market Index |

-11.7% |

15.1% |

4.1% |

12.0% |

1.9% |

|

U.S. high yield |

-3.7% |

16.4% |

3.8% |

5.9% |

-6.9% |

|

U.S. investment grade |

0.9% |

3.0% |

2.6% |

4.9% |

5.1% |

|

U.S. MBS |

10.0% |

22.7% |

7.4% |

20.7% |

71.4% |

|

U.S. Treasuries (10-year) |

3.8% |

-2.6% |

-0.4% |

5.8% |

16.2% |

|

U.S. Treasuries (2-year) |

1.0% |

0.2% |

0.0% |

2.7% |

5.4% |

|

U.S. Treasuries (30-year) |

3.0% |

-4.8% |

3.2% |

6.2% |

32.6% |

|

UK Gilts (10-year) |

3.9% |

4.5% |

-0.8% |

5.1% |

6.2% |

Source: Bloomberg Finance L.P., DWS Investment GmbH as of 4/1/20

Past performance is not indicative of future returns.

1. Tweet from February 24: "The Coronavirus is very much under control in the USA. We are in contact with everyone and all relevant countries. CDC & World Health have been working hard and very smart. Stock Market starting to look very good to me!"

2. Since January his approval ratings have risen from 42.5% to 45.4%, see https://projects.fivethirtyeight.com/trump-approval-ratings/?ex_cid=rrpromo

3. See Tweet from March 29: “President Trump is a ratings hit. Since reviving the daily White House briefing Mr. Trump and his coronavirus updates have attracted an average audience of 8.5 million on cable news, roughly the viewership of the season finale of ‘The Bachelor.’ Numbers are continuing to rise..."

4. https://www.nytimes.com/2020/03/30/nyregion/ny-coronavirus-doctors-sick.html?action=click&module=Top%20Stories&pgtype=Homepage

6. Relative to the MSCI AC World Index

7. S&P 500

9. EuroStoxx 50

10. Dax

12. FTSE 100

13. MSCI Emerging Markets Index

14.

MSCI AC Asia ex

Japan Index

15. MSCI Japan Index

16. MSCI AC World Consumer Stables

17. MSCI AC World Health Care Index

18. MSCI AC World Communication Services Index

19. MSCI AC World Utilities Index

20. MSCI AC World Consumer Discretionary Index

21. MSCI AC World Energy Index

22. MSCI AC World Financials Index

23.

MSCI AC World

Industrials Index

24. MSCI ACWI Information Technology Index

25. MSCI AC World Materials Index

26. MSCI AC World Real Estate Index

27. Russel 2000 Index relative to the S&P 500

28.

Stoxx Europe Small 200 relative to the Stoxx

Europe 600

29.

Relative

to the Bloomberg Commodity Index