- The steep pace of development

- Much remains to be proven

- One of the few truly monumental trends

- What’s next?

- Investing: Some of the most important current questions

Steve Jobs said in 1984 that a computer was like a bicycle for the mind, meaning computing accelerated our ability to learn, think, and do. Extending that analogy, Artificial Intelligence or AI, significantly enhanced this progress with large language models (LLM), which takes the capability of computers to enable advanced thinking to an entirely new level, a level that is more akin to a jet airplane for the mind, whereby the technology has real potential to maximize our time and capabilities. We believe it is important to keep this vast potential in mind as we are nearing one year past the world’s introduction to LLMs and Generative AI, a moment where results start to matter more than potential, concept, and exuberant optimism.

"A computer is like a bicycle for the mind, meaning computing accelerated our ability to learn, think, and do."

- Steve Jobs, 1984

"A recent McKinsey survey revealed that 1/3 of their respondents are currently using Gen AI in at least one function."

When the potential of Generative AI (Gen AI) started to become apparent earlier in 2023, the possibilities to integrate in our daily lives seemed substantial and quite open ended. However, the use cases were not clear, efficacy was questioned, and importantly, safety became a legitimate concern. Standing here today we see use cases forming across all industries. In productivity there are multiple reports of tools that are saving hours per week, and in some cases hours per day for knowledge workers across a variety of companies and industries who have begun to infuse new technology across the spectrum of their operations. One example of this is the development of Microsoft Copilots, which is a set of AI powered tools that provide suggestions, summaries, and can generate content based on user input. Essentially this capability assistance mimics having a highly competent human assistant. A recent McKinsey survey[1] revealed that 1/3 of their respondents (arguably more digitally oriented) are currently using Gen AI in at least one function. And companies serving creators, like Adobe, have quickly integrated Gen AI capabilities to assist in accelerating and enhancing the content creation process.

The models have improved, and newer use cases are rapidly developing such as customized learning and personalized e-commerce. Training techniques for Gen AI have improved accuracy to minimize issues of hallucination, which is a scenario where the generated result seems correct but actually is wrong. Yet there is still much work to be done. On the regulatory front, lawmakers have been busy trying to understand and regulate the power of Gen AI but have yet to demonstrate an ability to regulate these tools effectively.

The evidence to date suggests that high expectations are more than warranted, in our view. The number of industries and companies that are finding highly productive use cases is significantly broader than envisioned at the beginning of 2023. Additionally, many countries are awakening to the need to invest in sovereign AI solutions, in their own models, with their own data, in their own languages, a trend not even contemplated previously. One reflection of the much broader applicability and concomitant investment is the substantial increase in revenue expectations for NVIDIA Corp (ticker NVDA). Revenues for the first three quarters of their ’24 fiscal year were $38.8 billion at the end of October 2023. This compares to full year fiscal ’23 revenue of $26.9 billion, a 43% increase with still one quarter of revenue to report.[2]

We recognize fully that there have been many promising technologies that didn’t deliver, yet our experience through similar technology revolutions in the past has taught us that innovation is often preceded by a slow gradual start followed by a period of rapid proliferation. And that is certainly our view of the potential around AI. As we are in the business of making judgements, we do see strong potential for the long-term impact to be far more meaningful than currently appreciated, even if it doesn’t develop in a straight line. AI has been a focus for many companies for well more than a decade, and powers much of what we use already (i.e., recommendation engines). But Gen AI (powered by LLMs) takes utility to an entirely new level given the machine’s ability to make connections by analogy, draw conclusions from perspective, and generate content. All of these functions provide open-ended capabilities and have shown to evolve from the initial models to now do things not even contemplated when developed (i.e., pass the bar exam).

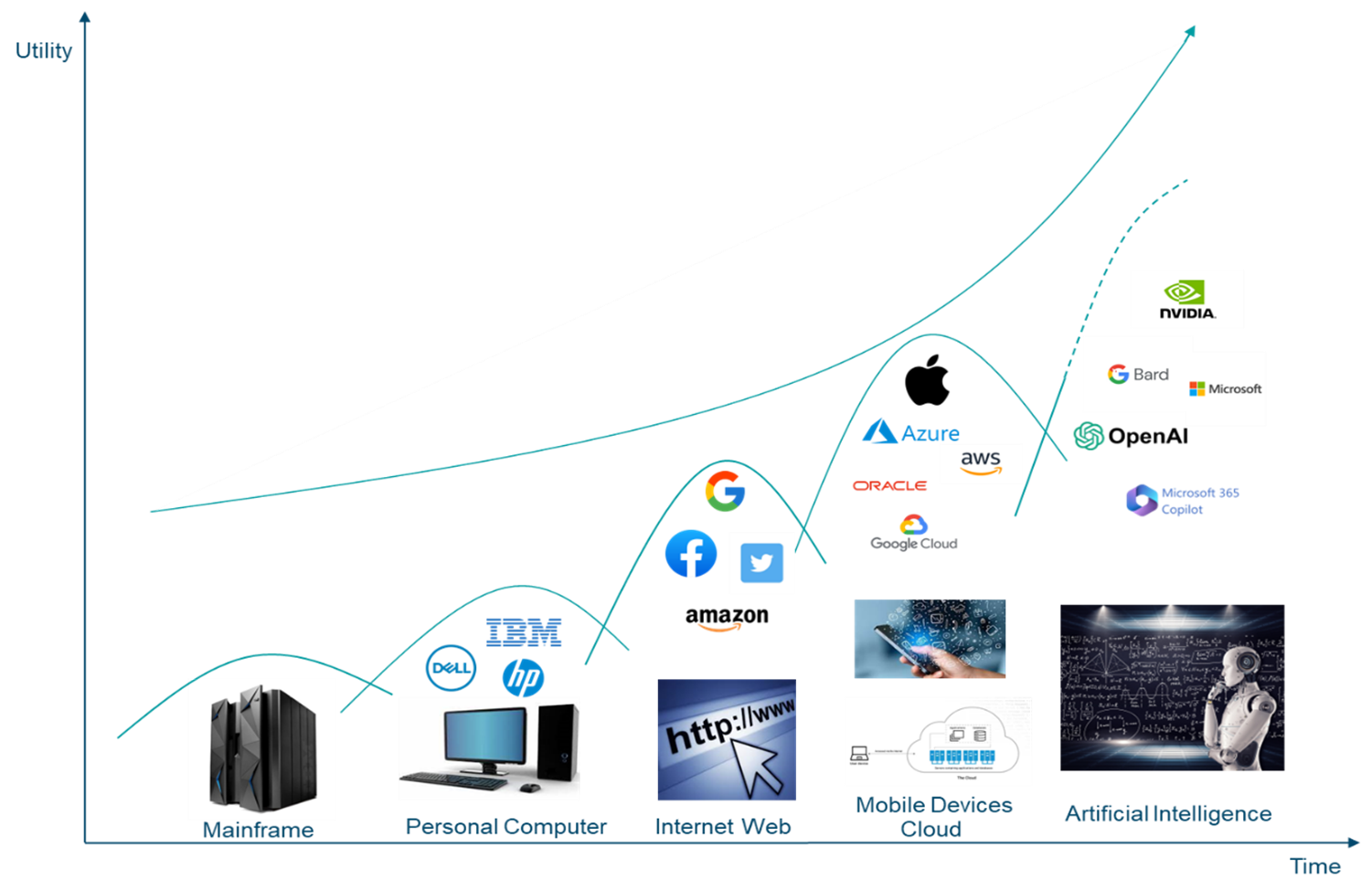

Steep pace of development

There has been a steep pace of development since several Gen AI services started to become generally available since the end of 2022:

- Number of models: While hard to quantify it is clear the number of LLMs has expanded significantly, from a handful a year ago, to a wide range across the world.

- Utility: The capabilities of the LLMs has sharply advanced (better answers, less hallucination) and have started to operate in multiple formats simultaneously (text, voice, images) to be “multi-modal.”

- Investment: Many of the mega technology companies have significantly accelerated investments in AI infrastructure, companies, capabilities in AI/LLMs, and AI services; One example is the firm Anthropic, who is an AI safety and research firm. Amazon recently announced a $4 billion deal with Anthropic, while several news outlets reported that Google agreed to invest up to $2b over the course of 2023.

- Services: Most companies in the technology industry, and some outside, have developed capabilities to apply Gen AI internally, as well as work to infuse their client offerings with Gen AI to help improve productivity across multiple platforms and unleash creativity to grow scale and relevance. For example, a podcast that is distributed to a particular region in a single language can leverage Gen AI to grow the consumer base by making that podcast available in multiple languages and multiple countries.

- Corporate boards focus and governance: Similar to topics such as cybersecurity and digital transformation, AI and Gen AI is gradually becoming a board level focus and IT budget line item. For example, International Data Corporation (IDC) expects Gen AI spend will grow from $16 billion in 2023 to $143 billion in 2027.[3]

- Venture Capital funding has been ample and growing; And,

- Regulators have been intensely studying the trend. At this point it continues to appear regulation will not be a significant constraint given the challenges of creating and enforcing regulation for something moving so fast. Additionally, they may have concern about perceptions of being viewed as hampering national competitiveness. Ultimately it is hard to predict what regulators will do, but these are factors that may impact how quickly they adopt Gen AI capabilities.

Much remains to be proven

Of course, much remains to be proven. After a swift pace of AI focus and investment, and some strong stock moves, the markets are now digging into the real questions of what will be the truly big applications, how long will they take to ramp up, and whether they can be delivered economically. Said another way, are we at or near “peak AI” sentiment and about to embark on the long plunge towards a trough of disillusionment? Or are we embarking upon the next phase of the Technology revolution where individuals and corporations will have their lives transformed by highly capable and customized AI? We welcome a period of healthy skepticism, as that is clearly in the best interests of us all. As investors, key points to monitor will be uptake of services and customer feedback, and key among those will be the uptake of Microsoft Copilots. Many of these are now generally available and anecdotal evidence of “saving hours per day” seems common, but the actual uptake and results reported by Microsoft will be even more important. Monetization is another important area of focus in terms of how much more can companies charge and how profitable is it. A consensus view seems to be that these products need to show measurable upside in revenue and operating margins for enthusiasm to continue. Of course, that makes sense, however we believe that near term monetization won’t prove to be as important as demonstrable utility. That is to say that if these services really do help people (i.e., save hours a day, find customers they couldn’t before, make discoveries that weren’t possible before), the market will be smart enough to look through the short-term lack of monetization, if that’s the case.

A monumental trend

At risk of sounding overly optimistic, this trend is likely to prove to be one of the few truly monumental ones. In the last big shift, the combination of cloud computing capabilities and mobile made the modern smartphone possible, which is now a geolocated device that provides access to much of the world’s information and connectivity to a large part of the planet’s population in the palm of your hand. As incredible as that is, AI makes our technology significantly more useful:

- User Interface -- Interact in our native tongue: One of the most significant innovations of the smartphone was the touch user interface which made accessing what was available easier – removing friction in this way is a big deal. LLMs take this to the next level – we can now interact with much of the world’s information in our native tongue(s). Now with text, but voice is fast coming. A fundamental differentiator and advantage of the company, Apple, is the design principle that technology should get out of the way for product development. The more naturally we can interact, the more productive and creative we can be, and Gen AI enables a whole new level of natural user interface. In fact, Jony Ive, the lead designer behind much of Apple’s iconic product platform is now (independently) working on an AI first device where a basic design principle is to reduce the amount of interaction via screens. Wouldn’t it be nice to spend less of our days and nights staring at and tapping into screens?

- Reasoning, intuition (sort of): In 1970s the famous physicist Richard Feynman was asked in a lecture whether machines can think. His response was that computers don’t think the way we do but they can produce very useful things, some much better than humans.[4] At that time, computers were getting very good at operations based on logic. AI and LLMs in particular, take their capability well beyond basic logic to areas that appear to us like reasoning and thinking by analogy, and some cases creativity. Clearly that point hits a lot of philosophical hot buttons, but it is simply the intention here to point the obvious reality that machines can now do things that appear to us like reasoning and creativity. In the coming quarters and years, we will come to know the similarities and differences between the thought process of ourselves and of our machines, and the practical applications will likely proliferate. A key product category is now “copilots” which is essentially like having a reasonably intelligent entry level person working side by side with you. That is pretty incredible. The current trajectory seems to be there will be many different copilots for different areas, and possibly our own, more generalized copilot that is personalized for you, and eventually Agents that go beyond by taking actions on our behalf.

- Generation: While AI has been around us for a while, the generative part is new. In short, the ability to generate, create content of many types, and do so in ways that reflect a sophistication level we can relate to (i.e., would pass the Turing test[5]) opens up a significant level of automation and interaction possibilities.

In the history of modern computing there have been many important technologies, trends, developments that have been instrumental, but just a small handful have been truly profound. For the reasons stated above, we believe AI is one.

Coming soon

Multi-modal: Unlike current LLM’s which operate in one mode (i.e., text), multi-modal is now increasingly available. These models can process and integrate multiple inputs beyond text including images, and audio. Beyond the greater ability to create (i.e., in multiple modes), these models likely will have richer perspective of our world.

- Use case and industry vertical solutions: Beyond the general purpose, Gen AI solutions, services that are tuned to and focused in a particular area (marketing automation, financial analysis, health care diagnostics) will be increasingly effective and available.

- Real-time language translation and interpretation: The “universal translator” concept will be reality and will start to be available during the first half of 2024.

- Taking action, beyond the copilot: The capability increasingly exists to go beyond summarizing and creating, to actually taking action. An example often used is to do research on a trip (including the user’s preferences) and create a full itinerary (restaurant reservations included) and actually book the trip. More generally, the possibilities of automating workflows increase substantially with this capability. A reasonably possible progression here is that we eventually won’t have to use different applications for different tasks and instead just speak (or type) to our “agents” who know our preferences and can do research and take action on our behalf. This seems to go beyond the “copilot” concept, more like a superhuman assistant that is connected to much of the world’s information, people, and things (i.e., internet of things), and can get things done. The gaiting factor for this view of the world is less likely to be technology, much of what is needed is already here, but rather getting the coordination and buy-in of necessary parties.

- Increasingly personalized education and training: Beyond the historical one-size-fits-all approach, education and training can increasingly be personalized to a person’s strengths and needs and adapt in real time.

Investing Issues. Some of the most important current questions

- Arms race leads to overbuilding? Even the most profound trends can be overbuilt. The Internet circa 2000 is a prime example as it was massively overbuilt for demand at the time, but those facilities laid the foundation for what we have today. With knowledge of such high stakes in AI, there is currently an “Arms Race” underway – to build computer/GPU capacity, to build LLMs, and to develop AI services. It will likely lead to some excess, and semis/GPU is likely to prove no exception. But we think it’s a bit early to be sounding that alarm given the potential companies see. We acknowledge the potential for some investment slowdown in the next few quarters, and will manage risks along those lines, but the bigger trend is likely intact.

- Disrupted or enhanced competitive position? One of the most discussed dynamics in investing, particularly in technology, media and communications, is the idea of disruptive innovation, as described by Clayton Christensen in the landmark 1997 book, “The Innovator’s ” The idea is that a dramatically new product or approach powered by some innovation can provide the marketplace with a solution that is better, sometimes radically better, at a lower cost, and often starts off as what appears to be an inferior solution. This development poses a problem for the market leaders, the incumbents, as they are faced with the choice of either losing significant market share or following the new development that may cannibalize their existing base of business with much lower priced/margin business. What that misses, however, is that disruption has been a feature in some, but not all, big new innovations.

There are also sustaining innovations, those that actually enhance a dominant position of the incumbent. The question for investors is whether AI will be disruptive or sustaining? In our view the answer is BOTH! Of course, it depends on the company and the particular situation. We suspect that for the very big companies, that have large user bases, a lot of customer data, large language models and AI expertise, that Gen AI will be more of a sustaining innovation – for instance, social media companies will be able to improve the experience for the users as well as the advertisers on the platform. But the impact will not be even across the big companies. Of course, we reserve the right to change our view as new information becomes available, but the reason we say sustaining is more likely is that AI, and especially Gen AI, is quite expensive in terms of the facilities, data, intellectual property, and expertise needed. While it will gradually get more accessible for smaller startups in the future, we have already seen that AI can serve to dramatically improve existing products and competitive position for larger companies. If the view of agents comes to pass, that is we interact with our agents and no longer need a different application for different uses, then it becomes a lot more disruptive to incumbents, most obviously software companies. - Our framework: We are acutely aware that identifying a significant trend is a necessary but not a sufficient condition for generating investment Alpha. Not all trends are investable. The challenge is finding companies who derive a meaningful part of their opportunity, growth, and revenue from that trend, and who will sustainably benefit. And of course, just as significant is avoiding the companies which will be disrupted.

Below is how we are currently categorizing potential beneficiaries. Note that the mega technology companies, such as Amazon and Meta currently address much of the opportunity set. After figuring out where a company falls along the AI opportunity spectrum, we come back to our first principles which are: a.) How big and fast is their market growing? b.) How substantial and durable is their advantage? and c.) How much of that potential is in the consensus view? We believe that those who build and/or are good at applying Gen AI will emerge as dominant leaders in a whole new world of growth.