- Home »

- Insights »

- Global CIO View »

- Rising ESG bond volumes offer opportunities

- Sustainable bond investments have become an integral part of the capital market, and thus precisely meet the social and political discourse.

- The range of corresponding financial instrument is growing steadily; on the bond market in particular, there are more and more sustainable counterparts to traditional securities.

- ESG bonds historically have tended to outperform in some market phases. This could make them attractive in our opinion.

Sustainable bonds offer the chance to diversify and possible outperformance

ESG bonds have recently gained an important place in the global investment universe. In the past two to three years, in particular, these investments have been given a significant boost by lively public discussion. Sustainability has become integral to many areas of everyday life. And so why should this not be the case in bond markets?

The encouraging growth has been driven by both sides. Issuers have provided a diverse range of products. Investors seem to be in more and more demand for them. These securities offer the chance to diversify and there might be potential for outperformance over periods of time. They may offer interesting opportunities for bond investors.

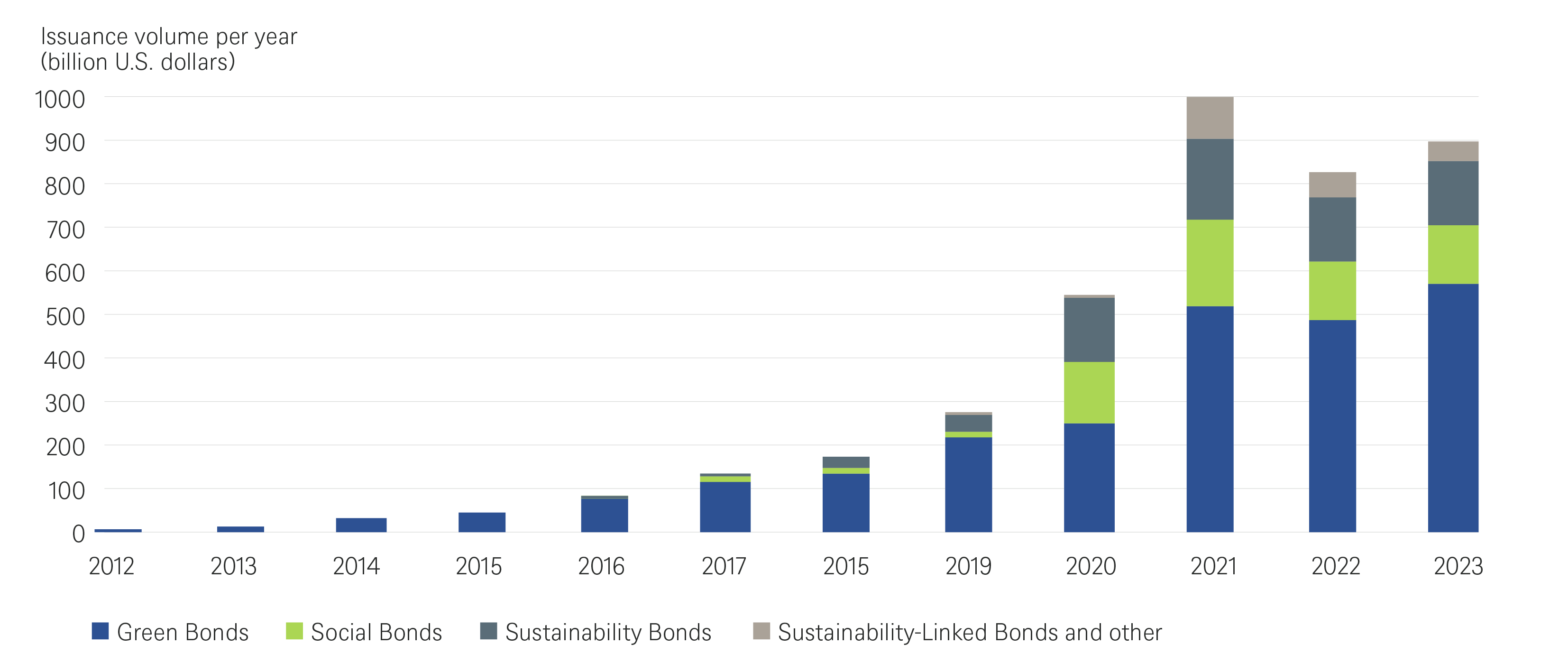

1 / The supply of sustainable investments keeps growing

1.1 Sustainable bonds are a great success story on the primary market

Strong global primary market activity in 2023 ...

ESG bonds are fixed-income securities whose proceeds are used to finance or refinance environmental or social projects or activities, or a combination of the two. Issuance of such bonds again reached an impressive volume in 2023, largely due to record sales of green bonds, according to data compiled by Citigroup.[1] Issuance of so-called use-of-proceed bonds (i.e. green, social, sustainability and sustainability-linked bonds) totaled USD 895 billion in 2023, a significant increase of around 8% compared to the same period last year. However, this figure is not a record. The previous one was set in 2021, when issuance reached just under $1 trillion. One segment where records were set in 2023 was green corporate and government bonds, which climbed to $571 billion, well above the volumes in 2022 and 2021 ($486 billion and $516 billion, respectively).

… continues at the start of 2024

This impressive performance by ESG bonds in the primary market continued in the first three months of 2024. Green bonds worth USD 202.5 billion were issued worldwide, according to Bloomberg data, the highest figure ever. With a 60% share of total ESG bond issues in the first quarter, green bonds have thus left the other segments far behind. Social bonds represented the second largest level of issuance in Q1, at USD 63.9 billion, 19% of the total, closely followed by sustainability bonds with USD 60.2 billion, 18% of the total. At USD 11.8 billion (3.5% of the total volume in Q1), sales of sustainability-linked bonds remained weak.[2]

Dynamic development in the ESG bond market

Sources: Citi Global Sustainable Debt Capital Markets, DWS Investment GmbH as of 3/22/24

European IG and high-yield corporate bonds particularly strong

The trend in euro-denominated European corporate ESG bonds in the investment grade (IG) and high yield (HY) segment was particularly strong, the Bank of America calculates.[3] During the first three months of the year, ESG bonds with a volume of around EUR 46 billion were issued in the IG segment – only about EUR 1 billion below Q1 2023, the strongest first quarter to date, and already equivalent to around 33% of total sustainable IG issuance in 2023. In the high-yield segment we are already at around 43% of last year's total volume, with issuance of EUR 6 billion in the first quarter.

A look at the volume outstanding also clearly shows that the role of ESG bonds is becoming increasingly important. A good 16% of the ICE BofA Euro Corporate Index now consists of such securities, compared to around 11% for the corresponding high yield index. In 2023 as a whole, ESG corporate bonds accounted for just over 28% of the total supply in this sector, with green bonds accounting for just over 75% of sustainable issues.[3]

Given the increasing investments being made in the Energy Transmission Sector, we believe that sustainable investing will become extremely important in the coming years. For the more distant future, they represent a potential factor of differentiation, if the issue is pursued with the necessary vigor. Green bond issuance is likely to become active even in sectors that have seen little or no green bond issuance so far.

1.2 What is the framework for sustainable bond emissions?

ICMA's Green, Social, Sustainability and Sustainability-Linked Principles

The market for sustainable bond investments has grown in recent years. As a result, it is becoming increasingly difficult for investors to identify which products really fall into this category and which providers and issuers may just want to jump on the bandwagon without really meeting high environmental standards. Statutory rules and regulations for ESG bonds have been adopted by the EU but are not yet really established. This is why standards set by private initiatives are currently being used, such as the Green Bond Principles (GBP) of the International Capital Market Association (ICMA).

The GBP are a collection of voluntary guidelines and principles, intended to give investors a certain degree of security. The GBP are closely related to the Social Bond Principles (SBP), the Sustainability Bond Guidelines (SBG) and Sustainability-Linked Bond Principles (SLBP) of the ICMA. According to ICMA’s website: "The Principles are a collection of voluntary frameworks with the stated mission and vision of promoting the role that global debt capital markets can play in financing progress towards environmental and social sustainability. The Principles outline best practices when issuing bonds serving social and/or environmental purposes through global guidelines and recommendations that promote transparency and disclosure, thereby underpinning the integrity of the market. The Principles also raise awareness of the importance of environmental and social impact among financial market participants, which ultimately aims to attract more capital to support sustainable development."[4]

In the EU, the taxonomy sets the basic framework, while the "Green Bond Standard" specifies the criteria

In the European Union the so-called EU taxonomy is the basic framework for classifying green or sustainable economic activity. The EU taxonomy, which came into force in July 2020, creates clear rules and framework conditions for the concept of sustainability, defining when a company is operating in a sustainable or environmentally friendly manner.[5] In our opinion, the framework is an important and, above all, necessary step towards channeling capital flows into sustainable investments and supporting companies in their initiatives to become more environment-friendly.

In order to make investing in sustainable assets safer, the "Regulation (EU) 2023/2631" of the European Parliament and of the Council on European Green Bonds (EUGBV) was published on November 30, 2023. It sets out an EU-wide market standard for "green" bonds: the European Green Bond Standard (EUGBS).[6] A bond that complies with this standard must fulfill special conditions linked to environmental sustainability criteria. The EUGBS also specifies how external auditors, national financial supervisory authorities and the European Securities and Markets Authority ensure that issuers comply with these requirements. Of course, issuers can still decide for themselves whether or not they want to issue their bonds as EU Green Bonds (EuGBs). It is also still possible to comply with the other available sustainability standards, such as the ICMA’s GBP. However, if an issuer decides to issue its bonds as EuGBs, the EUGBS must be strictly adhered to.[7] As the responsible supervisory authority, BaFin, Germany's Federal Financial Supervisory Authority, monitors whether issuers of European Green Bonds fulfill the transparency and information requirements. BaFin also keeps an eye on whether the required documents have been checked beforehand by external auditors.

Rating agencies are also hopping on the ESG bandwagon

Much has improved for investors in sustainable products in recent years. A number of uncertainties have at least been mitigated by the various frameworks and regulations. Rating agencies also play an important role in the evaluation of sustainable assets and the large, well-known agencies are not the only ones to have felt compelled to meet investors’ increased demand for relevant information. A number of specialized agencies have also been founded. In the case of ESG bonds, the so-called second party opinions, which are external verifications that an investment complies with sustainability standards, are an essential part of the external assessment of the quality of the security.

2 / Greenium & Performance

2.1 Sustainable bonds often act as performance drivers, especially in more turbulent markets.

However, investing in sustainable products should not be an end in itself. Sustainable investments need to be attractive in order to compete with their more traditional counterparts. In recent years, it has become clear that it is not only the difference in yield between conventional bonds and ESG bonds (greenium) that can be an incentive to invest sustainably (although in the longer history of the ESG market, the opposite was certainly true, i.e. that ESG bonds were more expensive for investors).[8] Expected secondary market performance also plays a key role. Ideally, investors in ESG bonds will benefit from the outperformance of ESG bonds, as they offer not only the identical borrower profile (in the case of different bonds from the same issuer), but also the specific and sustainable use of funds discussed above, which should appeal to a broader group of investors. If green bonds offer a comparable yield to conventional bonds, we believe there is a strong case for preferring sustainable securities. After all, they should generally perform at least as well or better than conventional bonds. In particular, ESG bonds have historically outperformed during periods of increased volatility and slightly negative sentiment in the bond market, mainly because volatility is often lower in the sustainable segment due to higher buy-and-hold ratios. However, during rallies, the performance of the two asset classes tends to be broadly balanced.

ESG bonds have often performed better over time in recent years. For example, those bonds performed strongly against their counterparts in the Bloomberg Global Aggregate Bond Index in 2023. That was not the case, however, in 2022, when ESG bonds clearly underperformed. In Europe, the outperformance of ESG bonds in 2023 was not quite as pronounced.[8]

Significant outperformance of global ESG bonds

Sources: Bloomberg Finance L.P., DWS Investment GmbH as of 4/18/24

When looking at this chart, however, it should be noted that there is a very strong weighting of government bonds and supranational issuers within the respective indices. These have a significant influence on performance at times, as the quality criterion "sustainable" plays a much greater role within these segments (at least so far). However, even if we only look at corporate bonds (including financial institutions), the picture is largely similar.

However, following the generally strong performance of European corporate bonds in 2023, the performance picture of ESG bonds compared to their traditional counterparts has changed somewhat since the start of the current year. Currently, the year-to-date performance of these two segments is largely balanced, with sustainable securities even underperforming for a short time. The greenium at times shrunk close to zero after averaging around 5 basis points in 2022 and 2023.[8]

Only slight outperformance of European ESG corporate bonds in 2024

* indexed, year end 2023=100

Sources: Bloomberg Finance L.P., DWS Investment GmbH as of 4/18/24

The markets are currently nervous, particularly due to geopolitical tensions and significantly reduced expectations of interest rate cuts in the U.S. In our view ESG corporate bonds therefore have the potential to outperform again if investors, as we expect, tend to prefer the ESG bond in the event of a "tie" between the two segments.

3 / Summary and outlook

In our opinion, sustainable bond investing will become increasingly important in coming years – driven primarily, but not only, by the general political and social discourse on environmental protection and sustainability. Investments in ESG bonds are in line with the 17 climate goals of the United Nations, promote transparency and thus contribute to a more sustainable and low-carbon economy for European companies. In addition, more and more frameworks and regulations, with which reputable issuers comply, may give investors confidence that issuers are not jumping on the green bandwagon without really being sustainable

We assume that the sustainable corporate bond segment will experience another growth spurt in the coming years, with further increases in issuance volumes. Investors seem to be increasingly interested to do something positive for the environment with their investments decisions. But this is not the whole picture. Investments must make financial sense.

What seems to make ESG bonds particularly attractive (besides all the risks that they entail, just like traditional bonds) is that they, at least in the recent past since the beginning of 2023, have tended to perform better than traditional bonds due to their lower volatility, especially in phases of higher market uncertainty. Indeed, they have also tended to lose some of their outperformance in times of bullish sentiment. But at least in the period we are considering it is rare that they underperform bonds without a sustainability label. On balance, sustainable investments therefore bring advantages: in our opinion, they make sense environmentally and financially.