- Home »

- Insights »

- Global CIO View »

- Chart of the Week »

- Of Bund yields and paradigm shifts

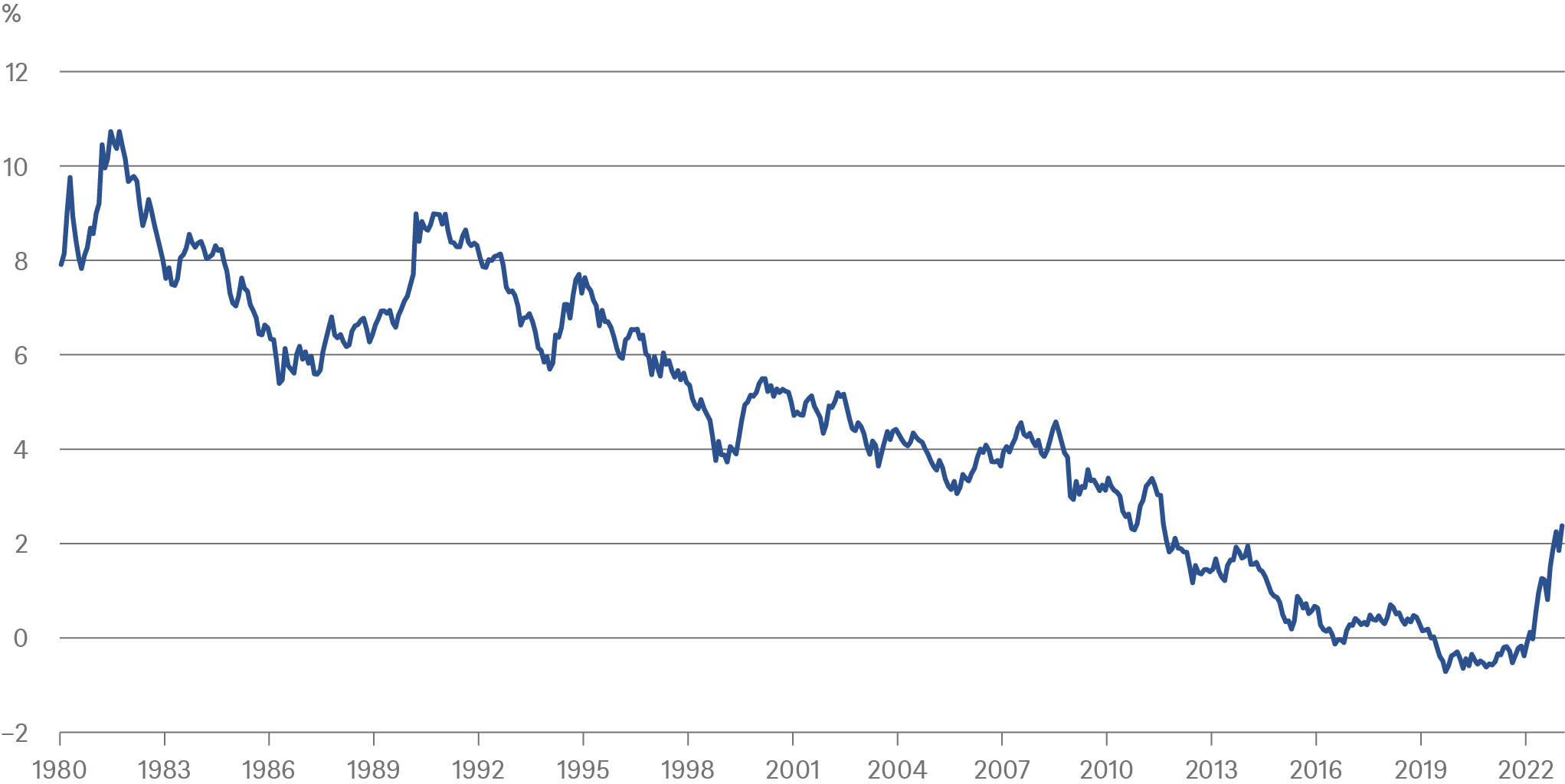

From a long-term view, 10-year Bund yields remain strikingly low

Sources: Refinitiv Datastream, DWS Investment GmbH as of 1/4/23

To see why, take a look at our Chart of Week, which simply shows the yields of the past 40 years on 10-year German government bonds, known as Bunds. Now, imagine that you are a veteran German bond investor in around 2010. How likely would it have appeared to you that 10-year Bund yields could fall below and stay below 2% for any prolonged length of time? The data up to 2010 would have pointed to a very low likelihood. So would have the conceptual tools that had served you well for so long – how much compensation investors in Bunds had typically demanded, say, for the uncertain paths of future inflation, German fiscal policy and global interest rates in the past.

After a few years of underperformance, you might have been replaced by someone younger, more comfortable with the emerging lower-for-longer paradigm. Presumably, you would have spent 2022 chuckling during your retirement on how your successors could have been so short sighted not to see the disastrous year in fixed income returns coming. With nominal Bunds still only yielding around 2.4%[1], you still find it hard to fathom how German inflation of 9.6% (as calculated on the harmonized, EU measure) should count as a positive surprise to today’s market participants.[2]

Well, we remain comfortable with our strategic target for 10-year Bunds trading at 2.4% by year-end 2023, at least for now. To be sure, there are risks, with higher Bund issuance volume to come, and the European Central Bank (ECB) set to reduce reinvestments under its Asset Purchase Programme (APP) from March onwards. Beyond specific news events, though, it seems appropriate to start the year by acknowledging the high likelihood that we are still in the middle of what seems to be a set of major paradigm shifts since the start of the 2020s.[3] It is still very early to say what the result will be as a new common view. And while we do, we would not necessarily agree with all the thoughts of the above 2010 market veteran, occasionally looking at an issue in 2023 through pre-2010 paradigms might be quite a helpful way to avoid overinterpreting the lessons of the past 12 years. In that spirit, happy New Year!