- Home »

- Insights »

- Global CIO View »

- Chart of the Week »

- That perennial de-dollarization debate

Depending on how and where you get your news, you have probably read about the “stunning” pace of “de-dollarization” since the start of Vladimir Putin’s latest war in 2022[1]. Adjusted for price changes (i.e. after reflecting currency and interest rate changes), the dollar’s share of official global reserve currencies has probably fallen quite dramatically, according to estimates by Stephen Jen, now at Eurizon SLJ Capital[2]. We won’t reproduce the chart here, not least because since the Financial Times ran it in mid-April, it has been eagerly picked up by all the usual channels[3]. Chances are that you already have it, with a few selective quotes, in your inbox.

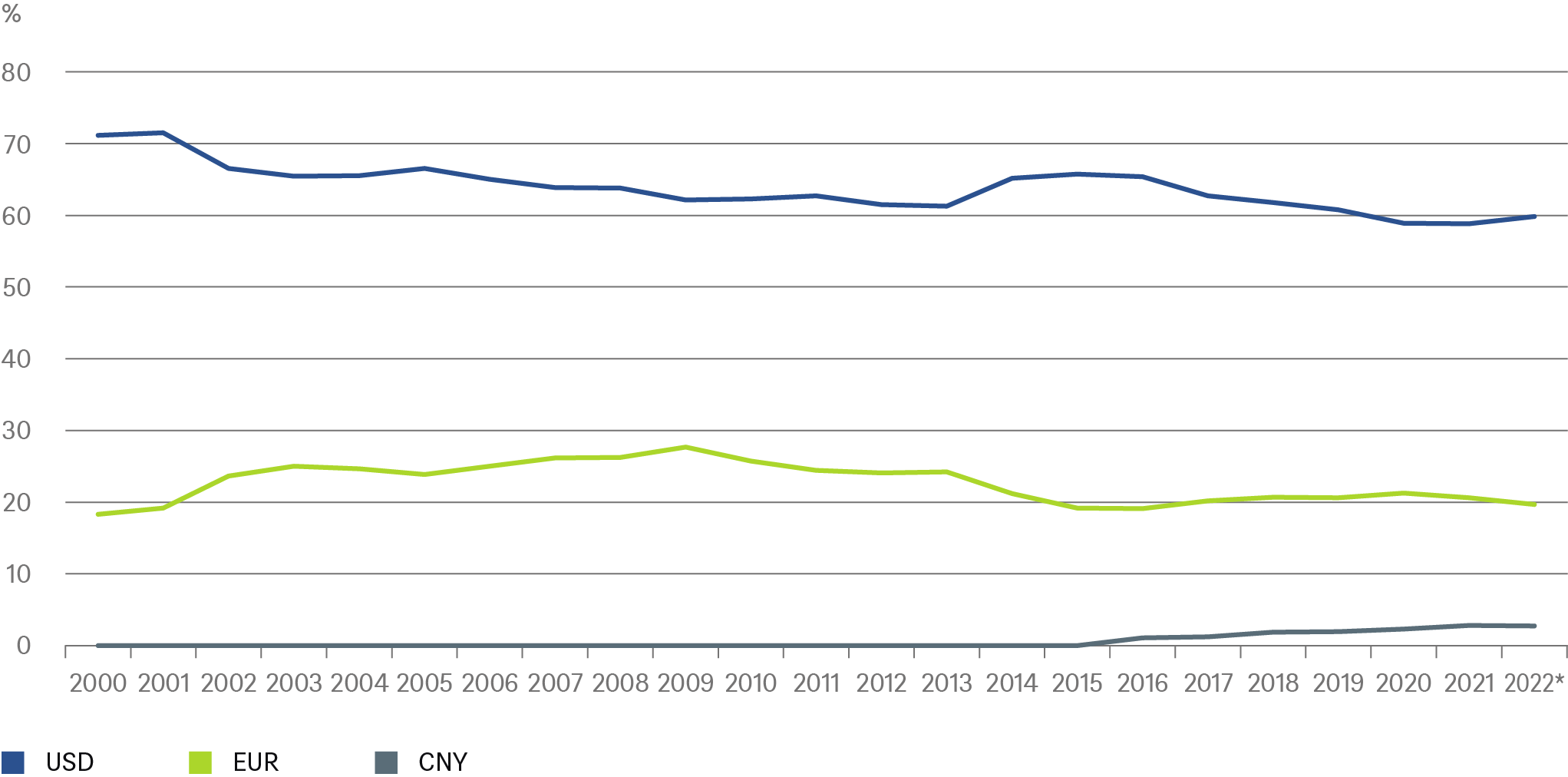

What you might not have so readily available is the reassuringly boring picture of world’s central banks’ dollar holdings in nominal values, i.e. before price changes. Our Chart of the Week shows the world’s reported and allocated currency reserves, which nowadays account for the vast bulk of them[4]. A picture of stability, though depending on where you start, you can certainly tell a story of dollar decline. Indeed, questions such as “Will there be a dollar crisis?” and “What would be the macro-economic scenario of a sudden collapse of the greenback’s value?” have long been the stuff of not just market chatter but profound economic debates in recent decades[5]. “Our take is that steady de-dollarization is likely to continue in the coming years, partly reflecting growth and growing financial sophistication in the rest of the world”, argues Dr. Xueming Song, currency strategist at DWS.

A reassuringly boring picture of world’s central banks’ dollar holdings

* Data until Q3 2022

Sources: Bloomberg Finance L.P., IMF, DWS Investment GmbH as of February 2023, as of 5/2/23

Given how entrenched the greenback’s position is in international trade and finance, though, we would strongly caution against any trying to identify particular events as sudden triggers. Take Western sanctions against Russia after the Russian invasion in Ukraine and resulting changes in inflation, interest rates and currencies since February 2022. This seems to have caused many central banks to dramatically rebalance their portfolios – but probably in quite a mechanical fashion, rather than deliberate policy changes. Otherwise, why would the counterbalancing “real” increases (after adjusting for price changes) to offset the “real” decline in the dollar’s share mainly show up in the shares of Euro and Yen?

In any case, most would-be global reserve currencies, notably China’s Yuan, would have to see dramatic changes in domestic policies to enable them to fulfill the world’s needs for safe assets currently (mainly) served by U.S. treasuries. There is an interesting twist, however. It does appear that more and more emerging market central banks have continued to increase the share of gold in their reserves, mainly at the expense of dollar-denominated bonds. It would be interesting to know how much of this recently acquired central bank gold is actually held within the countries in question. The experience of the Baltic states in the last century are instructive in this regard[6]. For one thing, it underlines the wisdom of keeping some central reserves – in whatever form - safe from foreign invaders by storing them in stable and wealthy democracies, especially for small democracies in fear of powerful, autocratic neighbors.