- Home »

- Insights »

- Global CIO View »

- Chart of the Week »

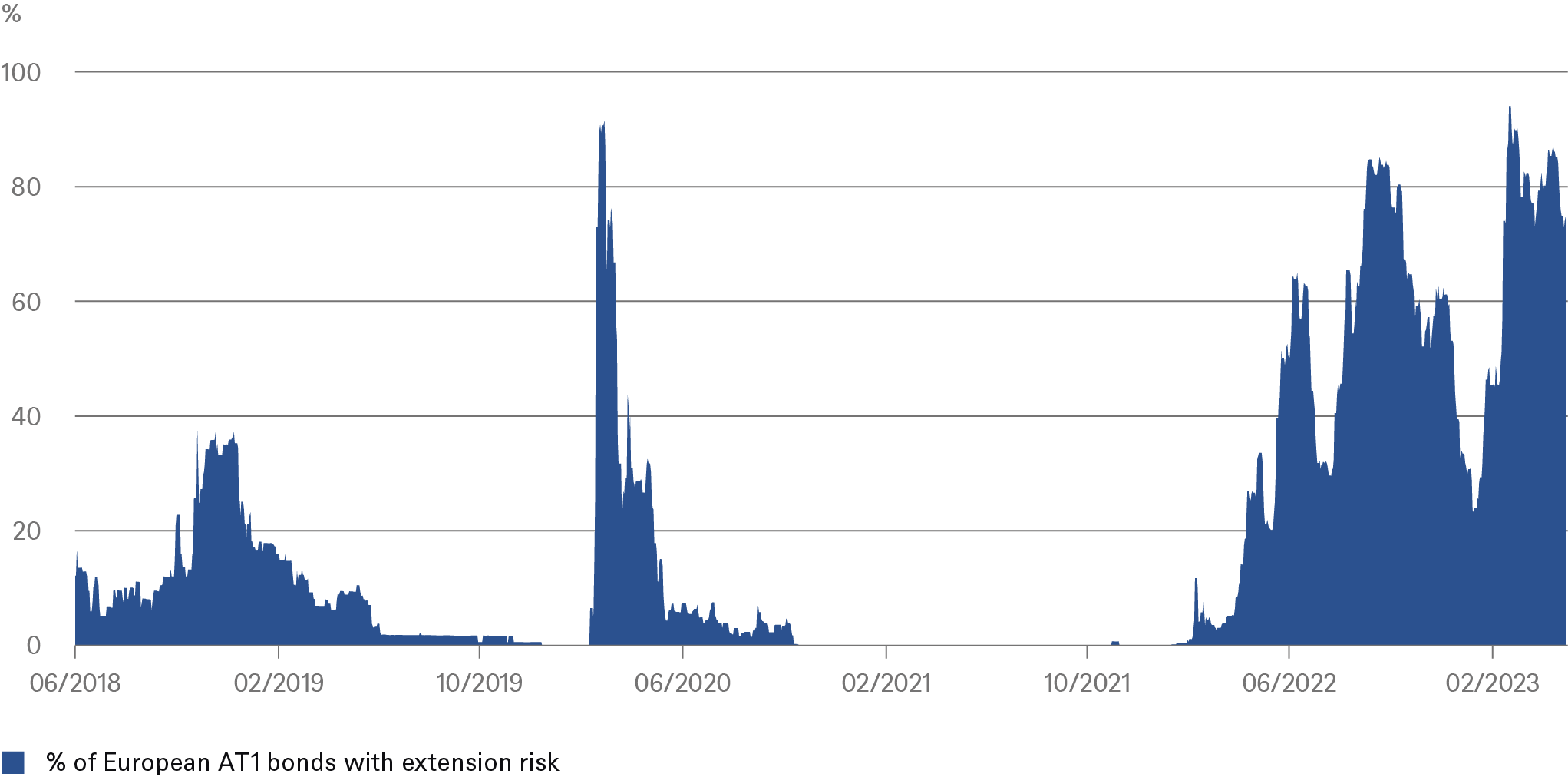

- European bank bonds show surprising anxiety

Percentage of AT1 bonds that are priced as if they were held to perpetuity

Sources: Bloomberg Finance L.P., DWS Investment GmbH as of 5/31/23

Our chart, nevertheless, reveals a remarkable anomaly, as it is trading at about the same highly stressed level as during the March crisis. This is not in line with our view of the state of the European banking sector, which we would consider to be well capitalized and with sufficient liquidity. Nor does it correspond to what share prices or bond default insurance prices of financial institutions indicate. And above all, it does not correspond to what is currently seen in the market. With the exception of six bond issues - which corresponds to only about 1% of the AT1 market - all AT1 bonds have been called at the first possible moment. Even when it was not optimal for economic reasons. And so the banks still seem to fear reputational risk. "From our perspective, AT1 bonds are pricing in too much risk, which can really only be due to the fact that entire investor groups have abandoned this segment since the CS incident. In our view, this makes this segment even more attractive at the moment," says Michael Liller, Senior Credit Portfolio Manager at DWS.