- Home »

- Insights »

- CIO View »

- Chart of the Week »

- Making sense of commodity price forecasts

With geopolitical risk spreading from Europe, to the Middle East and now the Taiwan Strait, commodities are a hot topic again in markets. From a disruption in critical energy, rare earth metals or food supplies, to possible flight to safe havens such as gold, these are the sorts of events that make forecasting hard. But is heightened geopolitical risk really a key driver in making commodity prices less predictable?

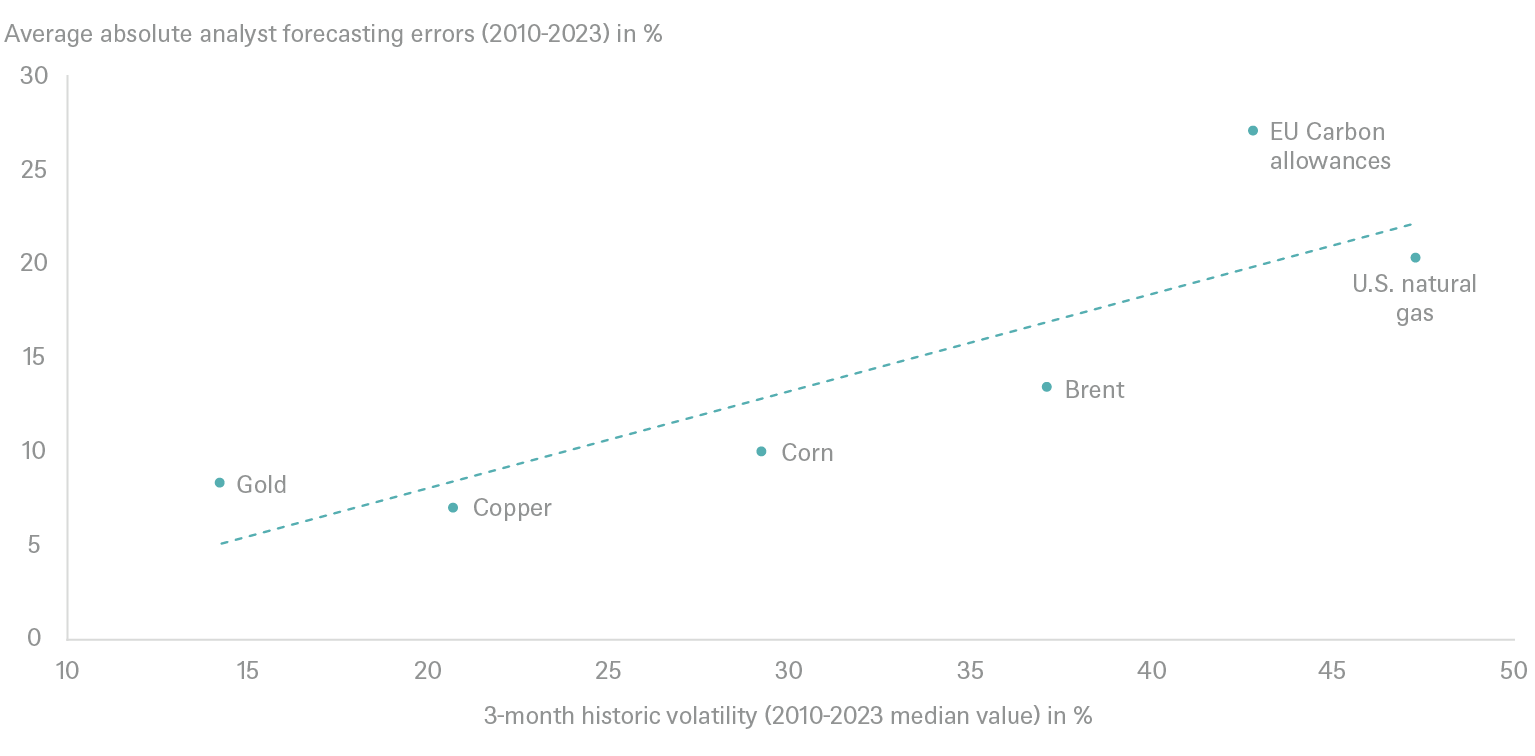

Closer analysis shows that not all commodities are equal when it comes to forecasting prices. This week’s Chart of the Week compares the average absolute analyst forecasting error for various commodities with that commodity’s underlying volatility since 2010. The results reveal a clear positive correlation: the higher the volatility, the larger the analyst forecasting error for that commodity’s future price.

This implies that you can have a relatively high degree of confidence when it comes to the year ahead price forecast for gold and copper; for these price forecasts are typically off by no more than 10%. By contrast, you need to take price forecasts with a heavy pinch of salt when it comes to energy commodities.

Commodity price forecasting errors and volatility

A large part of this volatility divergence between energy and metals can be explained by each commodity’s market and physical characteristics. For example, there is a wide range of consumption-to-inventory ratios across the commodity spectrum. These ratios are typically lower for metals and higher for energy commodities. In layman terms, when an oil supply outage occurs, it will bring about physical shortages significantly faster than if a gold mine collapses.

Within the energy complex, one commodity stands out, namely EU carbon allowances. Between 2010 and 2023, the average absolute forecasting errors has been in excess of 30%, which is more than three times that of gold and almost twice the forecasting error of Brent crude.

Part of the reason that historically, carbon prices have been so challenging to predict is that the market is still maturing. The EU’s emissions trading scheme itself has evolved a fair bit since 2010. Initially, only very few analysts dared to even try to forecast carbon prices. Their numbers have been growing, as more and more investors discovered the asset class. A larger and more diverse crowd might be expected to result in more accurate forecasts and perhaps in lower volatility too.[1]

Last year was a good year for carbon price forecasters, with the annual average EUA price less than 2% away from the consensus forecast made at the start of 2023. However, history would suggest not to read too much into such a low forecasting error just yet. Similarly accurate years in the past were followed by outsized forecasting errors the subsequent year. In 2018 and 2021, the forecasting error was in excess of 70%. According to Bloomberg, the current 2024 price forecast for EU carbon allowances stands at €85 per ton implying prices could either collapse below €40per ton or surge resolutely above €110 per ton. Our money is on higher carbon prices so long as world growth and global equity markets can keep calm amidst geopolitical storms. The smaller the error in 2024 is, the more confident we can be that the carbon market is indeed maturing.