- Home »

- Insights »

- Global CIO View »

- Investment Traffic Lights »

- Investment Traffic Lights

- It’s been another rewarding month for equity markets, but there are still some risks on the horizon.

- In the AI era, investor’s need to learn to apply Nassim Taleb's reverse Turing test.

- We conclude with 3 specific AI-related recommendations that we can offer you this summer with a particular high degree of conviction.

1 / Market overview

1.1 Another rewarding month for equity markets, but still some risks on the horizon

For most investors, July proved another good month. That was driven in part by several lower-than-expected inflation readings; the most remarkable being the real down-side surprise in U.S. consumer prices, with good news pretty much across the board.[1] All else equal, that would make a soft-landing scenario for the U.S. economy more likely. Keep in mind, however, that monthly inflation numbers are notoriously volatile, that the overall level of inflation in the U.S. and elsewhere remains too high for comfort, and that wages, notably in Europe, still have plenty of catching up to do. For now, we stick to our view that central banks will mostly prefer to err on the hawkish side.

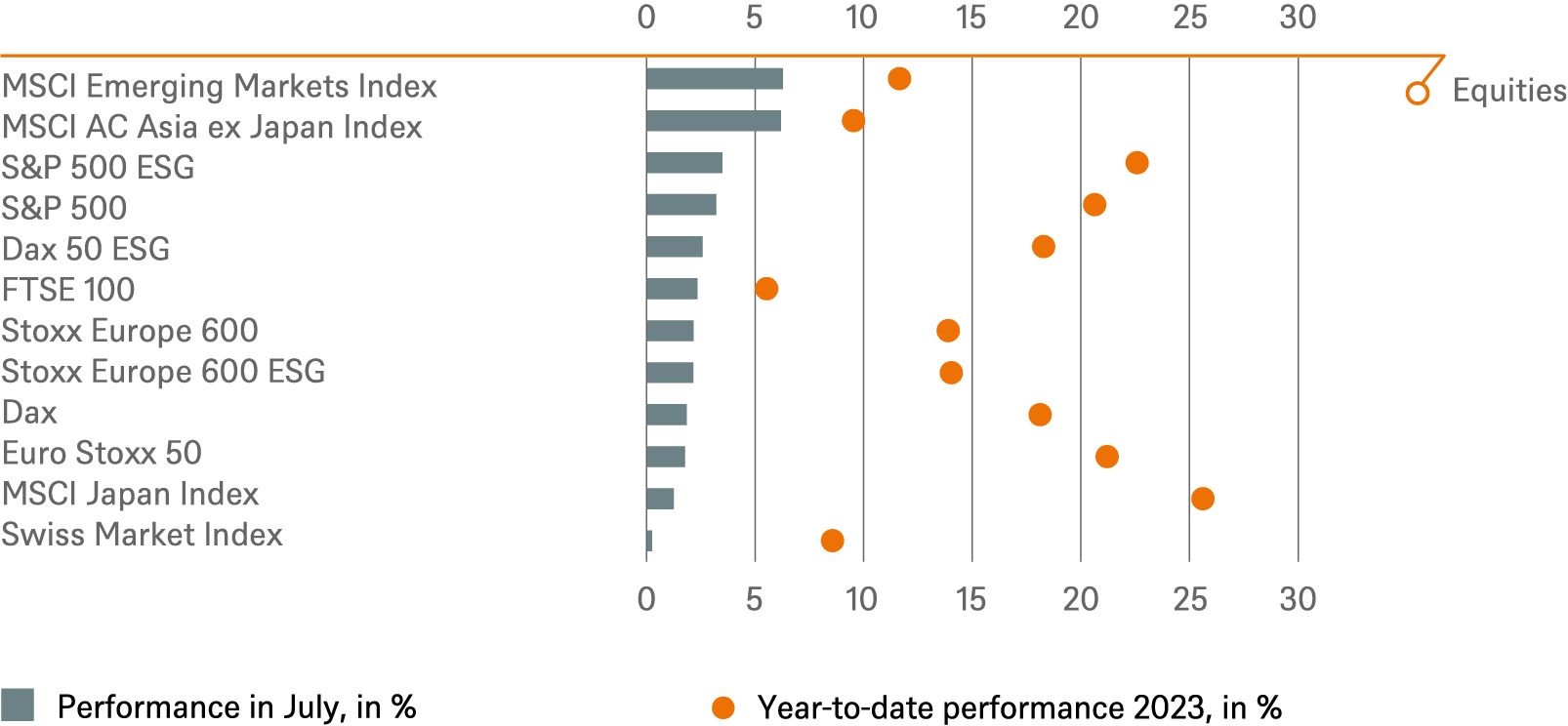

U.S. equities, both the S&P 500 and the Nasdaq extended their rally for fifth consecutive month of positive returns. Enthusiasm about artificial intelligence (AI) has undoubtedly helped, with the NASDAQ 100 ending July at a record-high and up 42% year-to-date. From a macroeconomic perspective, however, another factor is arguably more important: profitability, reflecting continued strong price setting power by many companies. Despite some mixed tech earnings in the past couple of weeks, U.S. corporate profits have held up remarkably well overall this year. This resilience, in turn, has helped sustain corporate investment, usually one of the cyclical swing factors.

We expect that the buoyant profitability also continues to encourage labor hording, following shortages in recent years. Tight labor markets, especially among skilled workers, contribute to wage pressures, especially in Europe, were the Stoxx 600 eked out a meagre monthly return of 2%, though it is still up 14% for the year. But while high margins and remarkable price setting power are nice at the micro level throughout the developed world, it is worth keeping in mind that they also have macro-economic implications, not least when it comes to fighting inflation.

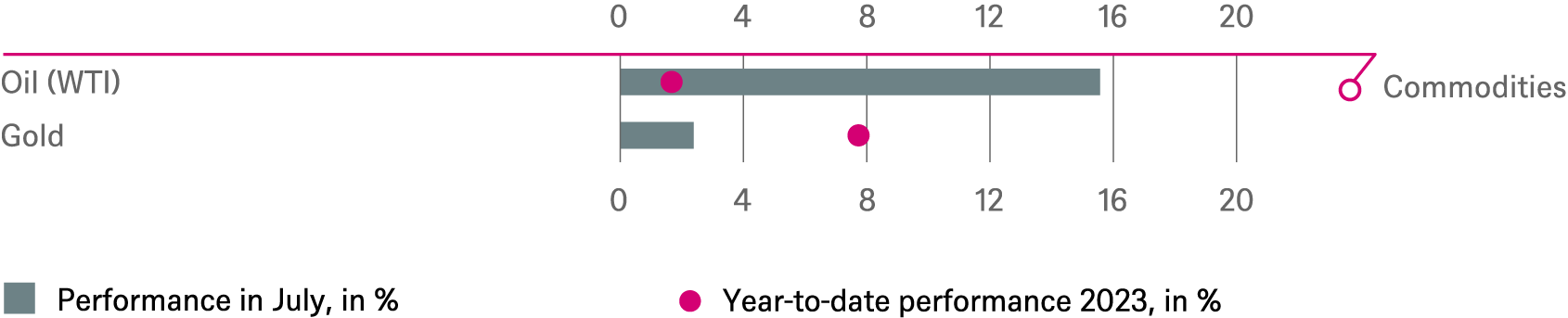

Elsewhere in markets, most commodities had a pretty strong month. Crude oil, in particular, had an impressive run, with gains of 16% for West Texas Intermediate (WTI). That won’t make the fight to get inflation under control any easier in coming months. It reflects production cuts by OPEC+, primarily voluntary supply cuts by Saudi Arabia, the world’s largest exporter of crude oil. However, we would expect the current high prices to eventually prompt additional supplies.

Oh, and have we already mentioned that equity markets remain enthralled with AI? You may well think that you have already had more than enough on that subject, including, potentially, from us.[2] Nevertheless, we will have to return to AI a few more times below, hopefully in ways that make for suitable reading on the beach. Already, AI is changing everything, including, as it happens, how to read market commentaries, such as this one.

1.2 Market commentary in the age of artificial “intelligence” and natural “ignorance”

Choosing “good” commentary to read has always been hard, regardless of the subject.[3] As my predecessor liked to point out, this involves sorting out sense from nonsense – and avoiding wasting time on the latter.[4] Add AI and AI-generated content to the mix, and things look even worse, right? After all, you never know whether a bot, as the wonderful AI term has it, might be hallucinating.[5] However, the situation is not quite as dismal as it might appear.

Fortunately for readers of this and other market commentaries, a solution is beginning to appear, as an indirect result of encountering more potentially AI-generated content. Indeed, chances are you may already have started to implement it, without consciously realizing what you were doing.

To the best of my knowledge, it was first suggested almost 20 years ago by Nassim Taleb, in his splendid and delightful book “Fooled by Randomness.” Taleb proposed a reverse Turing test, to, as he put it, “make the distinction between the babbler and the thinker.”[6] The idea is very simple: “A human can be said to be unintelligent, if we can replicate his speech by a computer (…) and fool a human into believing that it was written by a human.”[7]

Now, Taleb’s point was to poke mild fun at certain not particularly rigorous academic disciplines, when viewed from the perspective of natural science.[8] The computer he had in mind was literally generating pieces of grammatically sound text by randomly combining bits of published texts as building blocks. In the age of AI-driven language models, such as generative pre-trained transformers, computers have clearly gotten a lot smarter. At least in terms of predicting what humans will find convincing.[9]

That makes Taleb’s reverse Turing test an indispensable part of the mental toolkit of any 2020s reader, writer or investor these days. At the very least, it can help you sort out interesting from uninteresting content. Like expert intuition, much of modern artificial “intelligence” is based on pattern recognition.

Asking whether a comment is based on AI-generated text is already making all of us read more critically. And the skills we are learning are just as useful, if the entity doing the hallucinating is, ahem, very much human.

2/ Outlook and changes

When it comes to AI, we at DWS think that it is likely to prove to be one of the most consequential developments to emerge during our professional lives as asset managers.[2]

However, it is hard to argue that all that has been published during the recent hype would pass Nassim Taleb's reverse Turing test. Incidentally, markets have also historically had quite a dismal track record in correctly understanding and pricing seemingly ground-breaking innovations – precisely because intuitions and the seeming wisdom of the crowd can be misleading in the face of something truly novel.[10] In the meantime, there is no shortage of other topics to consider for various asset classes.

2.1 Fixed Income

Government Bonds

We uphold our neutral view for Bunds and Treasuries across the curve but expect the spreads of 10-year Italian and Spanish government bonds to tighten versus their German counterparts. We do so as these are driven by the rise in Bund yields and a recent switch of the 10-year generic Spanish benchmark bond. Overall, data-dependency following this month’s 25bps rate hikes by both the U.S. Federal Reserve (Fed) and the European Central Bank (ECB) continue to make the assessment of the Fed’s future decisions difficult, while the market’s data sensitivity makes for a volatile trading environment.

Investment Grade Credit

We remain overweight on EUR IG as spreads have continued to inch tighter at a decent pace these past few weeks. We also maintain an overweight position on U.S. IG credit supported by strong earnings and other technical factors, but also anticipate the market to experience slow and steady movements over the next several weeks following the removal of the debt-ceiling overhang, recent hawkish Fed commentary and positive July inflation data.

High Yield Credit

The EUR HY spread has remained relatively stable, as market sentiment and risk appetite for high-yield bonds has stayed consistent, despite lower-than-expected CPI data out of the U.S. We maintain a neutral stance on Eurozone and U.S. HY bonds amid fading supporting factors in the European Union (EU), mounting recessionary fears from recent profit warnings in the basic resources and chemicals space and tightened U.S. HY bond spreads following favorable inflation reports.

Emerging Markets

EM Sovereigns: Some sovereign bonds within the index trade at tight spreads, and lowly rated HY issuers could potentially contribute to further spread tightening. We maintain an overweight position for Asia Credit and EM Credit due to investors anticipating more stimulus following weaker-than-expected economic data in China, as well as ongoing disinflationary trends, expectations of peak rates from major central banks, and optimism about policy adjustments in certain key EM countries.

Euro vs. dollar

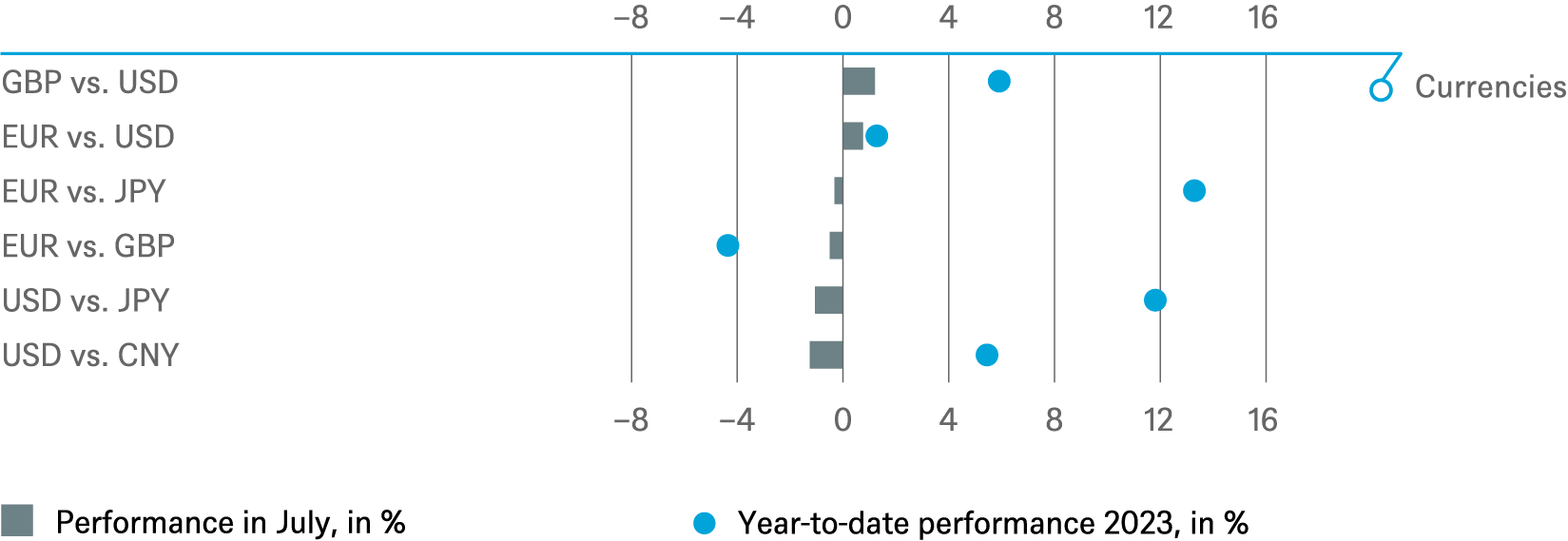

We have taken a long position in the euro against the dollar as the market is heavily influenced by the outlook on interest-rate policy, and currently, the interest-rate differential is in favor of the euro. After 25bps rate hikes from the ECB and the Fed, further action remains data-dependent, but with the ECB grappling with a higher inflation rate of 5.5%, prolonged hawkishness can be expected.

2.2 Equities

Looking only at the aggregate equity market is hiding a lot of variation, notably in performance terms of “growth” versus “value.” Such comparisons need to be handled with care, but it is still worth noting that on some measures, “growth” is currently trading at a 92% premium to “value” which is close to the historic high in 2020 when interest rates were close to zero. The embedded AI excitement remains high and will probably require constant reinforcement, not least during the current reporting season. Whether this could translate into a sustained “value” recovery is a different question altogether, due to cyclical risks.

U.S. Market

Inflationary and recessionary fears are slowly fading, and markets are optimistic towards AI and its implications for the tech sector. These developments have lowered the equity risk premium and explain most of the year-to-date rally. U.S. 10-year yields have not changed year-to-date and did not have much of a meaningful impact on the market. In summary, however, we remain unconvinced, and expect any economic recovery to be muted. We thus remain underweight U.S. equities.

European Market

We still overweight the Stoxx 600 since it is still trading at an excessive valuation discount to U.S. equities. Moreover, we strongly overweight European small and mid caps compared to large-cap peers, small and mid caps are still too cheap.

German Market

German equities have been rallying, lately, with the Dax reaching a historic high at 16,528 points on Monday, July 31st. Compared to the S&P 500, the Dax nevertheless continues to trade at a record price-to-earnings (PE) discount. Investors seem optimistic, and analysts believe the rally could even continue towards 17,000 points. This is uncharted territory, leaving plenty of uncertainty in both directions.

Emerging Markets

We remain neutral on emerging-market equities. Macro, micro, and geopolitical trends remain mixed. An ongoing weakness in the property sector and uncertainty among Chinese consumers lead to an increased down-side risk to the asset class.

2.3 Alternatives

Real Estate

Overall, fundamentals of the real-estate market are generally healthy with low vacancy rates and growing net operating income (NOI). We also believe that long-term interest rates are close to their peak, relieving pressure on valuations. Investors looking through the current price dip might find opportunities to buy into strong long-term fundamentals at attractive yields.

Infrastructure

With inflation becoming more benign and the interest-rate environment looking more stable, the focus for infrastructure performance will be shifting towards how assets can deal with the softer demand picture presented by slowing economic growth. Positive momentum should, however, build into 2024, driven by the strong performance of the asset class in recent years, the desire of investors to increase allocations, strong policy tailwinds in the sector and an unchanged value proposition relative to other alternative asset classes.

Gold

Precious-metal prices displayed a mixed performance, with gold finally recording a slight gain following a period of fluctuation as markets digested each U.S. economic data point.

Oil

As oil prices rebounded sharply throughout July, we now see only limited scope for further, gradual improvements in the coming months. Higher profit margins on refined products, an eventual reversal in WTI inventory trends and robust transportation demand across both developed and developing countries provide some support. However, in the medium term, reaching $85/bbl. may be challenging if China’s efforts to stimulate its economy remain limited, and Iran and Russia increase their oil exports.

2.4 DWS High Conviction

In addition to the ideas shared above, we would like to highlight three fixed income segments that usually do not feature as prominently in our investment traffic lights.

U.S. Mortgage-backed securities (MBS) have seen their spreads tighten considerably from the wides reached in May. With bank troubles seemingly receding and asset liquidations mostly done, MBS looks set to perform more in line with rates and rate volatility going forward. The coming months could see some very attractive entry points. We think that the primary source of spread volatility is likely to come from macro surprises and perceived Fed reactions and that the best value continues to be in higher coupon mortgage pools.

U.S. structured finance is dominated by commercial mortgage-backed securities (CMBS). As such, it should come as no surprise that problems with the office sector have dominated the headlines on the segment. However, keep in mind that the vast majority of commercial real estate is non-office and that multifamily residential, retail, industrial and hotel all continue to perform well. Conduit (diversified) deals with lower office exposure at the AAA/AA level should perform well even in extremely bearish scenarios. We favor low office conduit AAA/AA and high-quality AAA-A single-asset single-borrower (SASB), however, individual asset selection is key.

Finally, EUR covered Bonds over attractive carry over Bunds at 86 basis points. Swap spreads are expected to move lower over the coming months. We also think that covered bond spreads vs. swaps should not widen further in coming weeks due to subsiding primary market activity over the holiday season.

Talking about holidays, we are also delighted to offer a few ideas for beach side reading, all related, one way or the other to AI. For anyone interested in learning more, we would offer these three recommendations with the utmost conviction that they can definitely pass Nassim Taleb's reverse Turing test:

- Stuart Russell (2020) “Human Compatible: AI and the Problem of Control,” Penguin, 328 pages. This book offers an excellent overview on modern AI and machine learning, and what still needs to be done to make general-purpose AI feasible and provably beneficial. As the co-author of the main textbook on modern AI, Russell is able to simplify the subject for a general audience while still offering brilliant insights for AI specialists.

- Janelle Shane (2021) “You Look Like a Thing and I Love You,” Little Brown and Company, 259 pages. A very entertaining look at the differences between human and AI cognition, machine learning and the underappreciated dangers of AI often not being smart enough, rather than too smart.

- Ajay Agrawal, Joshua Gans and Avi Goldfarb (2022, rev. ed.) “Prediction Machines, Updated and Expanded: The Simple Economics of Artificial Intelligence” Harvard Business Review Press, 250 pages. Core reading when trying to think through what AI can do for you.

- And finally, as an indispensable guide for any investor, not just during periods of rapid innovation: Philip A. Fisher (2003 ed.) “Common Stocks and Uncommon Profits and Other Writings,” John Wiley & Sons, 292 pages. Do not even try to identify and assess companies offering spectacular growth potential, without reading this timeless classic first![11]

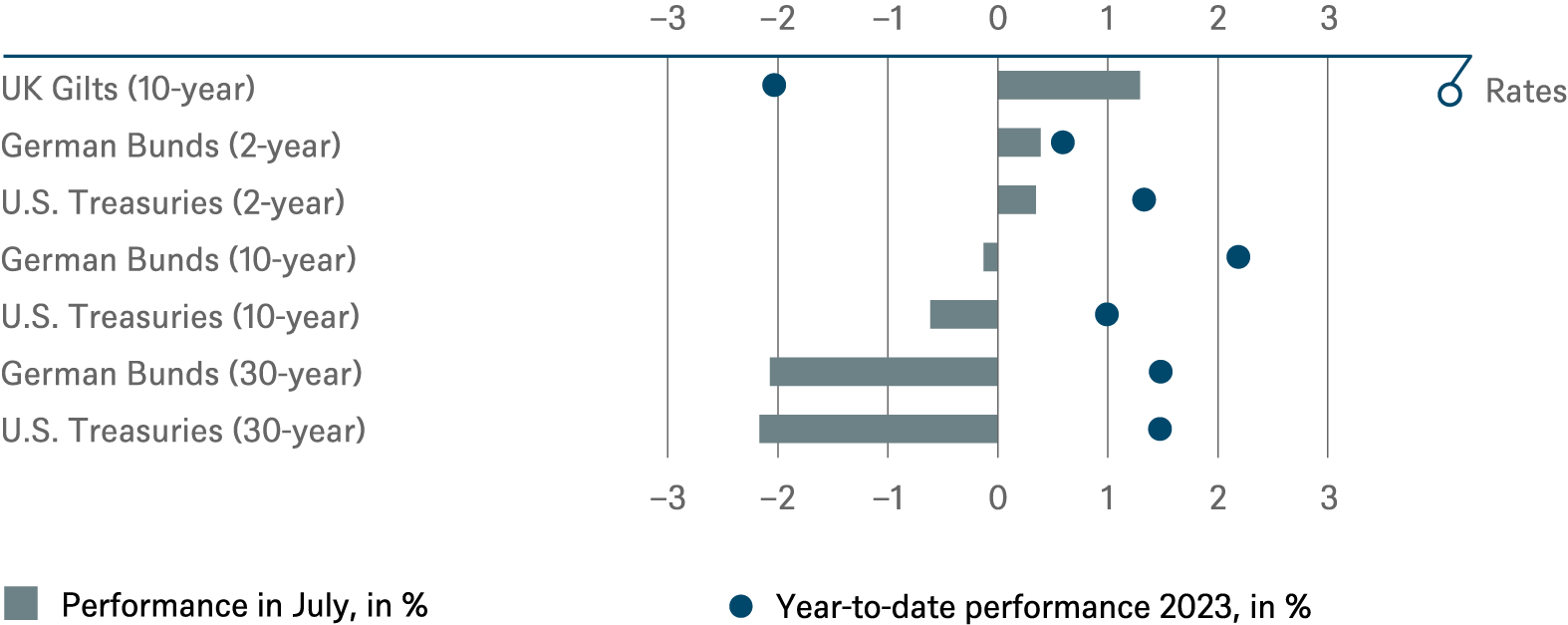

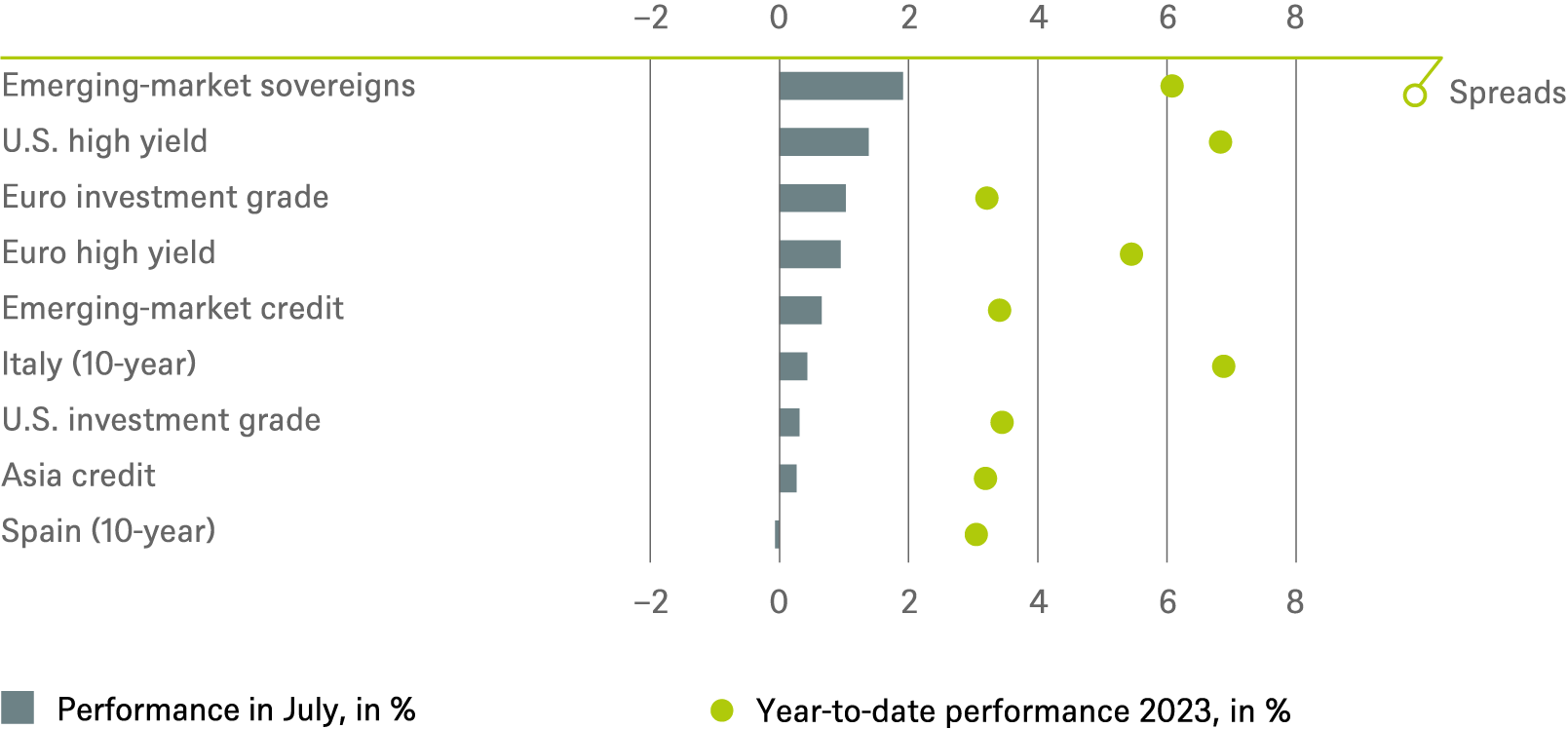

3 / Past performance of major financial assets

Total return of major financial assets year-to-date and past month

Past performance is not indicative of future returns.

Sources: Bloomberg Finance L.P., DWS Investment GmbH as of 7/31/23

4 / Tactical and strategic signals

The following exhibit depicts our short-term and long-term positioning.

4.1 Fixed Income

Rates |

1 to 3 months |

until June 2024 |

|---|---|---|

| U.S. Treasuries (2-year) | ||

| U.S. Treasuries (10-year) | ||

| U.S. Treasuries (30-year) | ||

| German Bunds (2-year) | ||

| German Bunds (10-year) | ||

| German Bunds (30-year) | ||

| UK Gilts (10-year) | ||

| Japanese government bonds (2-year) | ||

| Japanese government bonds (10-year) |

Spreads |

1 to 3 months |

until June 2024 |

|---|---|---|

| Spain (10-year)[12] | ||

| Italy (10-year)[12] | ||

| U.S. investment grade | ||

| U.S. high yield | ||

| Euro investment grade[12] | ||

| Euro high yield[12] | ||

| Asia credit | ||

| Emerging-market credit | ||

| Emerging-market sovereigns |

Securitized / specialties |

1 to 3 months |

until June 2024 |

|---|---|---|

| Covered bonds[12] | ||

| U.S. municipal bonds | ||

| U.S. mortgage-backed securities |

Currencies |

1 to 3 months |

until June 2024 |

|---|---|---|

| EUR vs. USD | ||

| USD vs. JPY | ||

| EUR vs. JPY | ||

| EUR vs. GBP | ||

| GBP vs. USD | ||

| USD vs. CNY |

4.2 Equity

Regions |

1 to 3 months[13] |

until June 2024 |

|---|---|---|

| United States[14] | ||

| Europe[15] | ||

| Eurozone[16] | ||

| Germany[17] | ||

| Switzerland[18] | ||

| United Kingdom (UK)[19] | ||

| Emerging markets[20] | ||

| Asia ex Japan[21] | ||

| Japan[22] |

Style |

1 to 3 months |

|

|---|---|---|

| U.S. small caps[33] | ||

| European small caps[34] |

4.3 Alternatives

1 to 3 months[35] |

until June 2024 |

|

| Commodities[36] | ||

| Oil (WTI) | ||

| Gold | ||

| Infrastructure | | |

| Infrastructure (non-listed) | ||

| Real estate (listed) | ||

| Real estate (non-listed) APAC[37] | ||

| Real estate (non-listed) Europe[37] | ||

| Real estate (non-listed) United States[37] |

4.4 Legend

Tactical view (1 to 3 months)

The focus of our tactical view for fixed income is on trends in bond prices.Positive view

Neutral view

Negative view

Strategic view until June 2024

- The focus of our strategic view for sovereign bonds is on bond prices.

- For corporates, securitized/specialties and emerging-market bonds in U.S. dollars, the signals depict the option-adjusted spread over U.S. Treasuries. For bonds denominated in euros, the illustration depicts the spread in comparison with German Bunds. Both spread and sovereign-bond-yield trends influence the bond value. For investors seeking to profit only from spread trends, a hedge against changing interest rates may be a consideration.

- The colors illustrate the return opportunities for long-only investors.

Limited return opportunity as well as downside risk

Negative return potential for long-only investors