- Home »

- Insights »

- Global CIO View »

- U.S. Economic Outlook

- Given the past trajectory of rate increases, and incorporating the expected lag of monetary policy, the Fed should keep rates at this level at least until early 2024.

- Recent data does not yet indicate that the U.S. financial system is suffering from a credit crunch.

- For the debt ceiling risk, a face-saving compromise involving the House Republican leadership remains quite likely.

Once you hit the brakes to avoid an accident, you should keep on doing so until the critical situation is clearly behind you. This everyday trivial wisdom also can be applied to monetary policy – at least to some extent. Obviously, the calibration of monetary policy to the current (and expected) situation of the economy is far more complicated, but the principle remains the same. The critical situation central bankers face right now is still too high inflation and a labor market that is most likely the tightest in recent, recorded U.S. economic history.

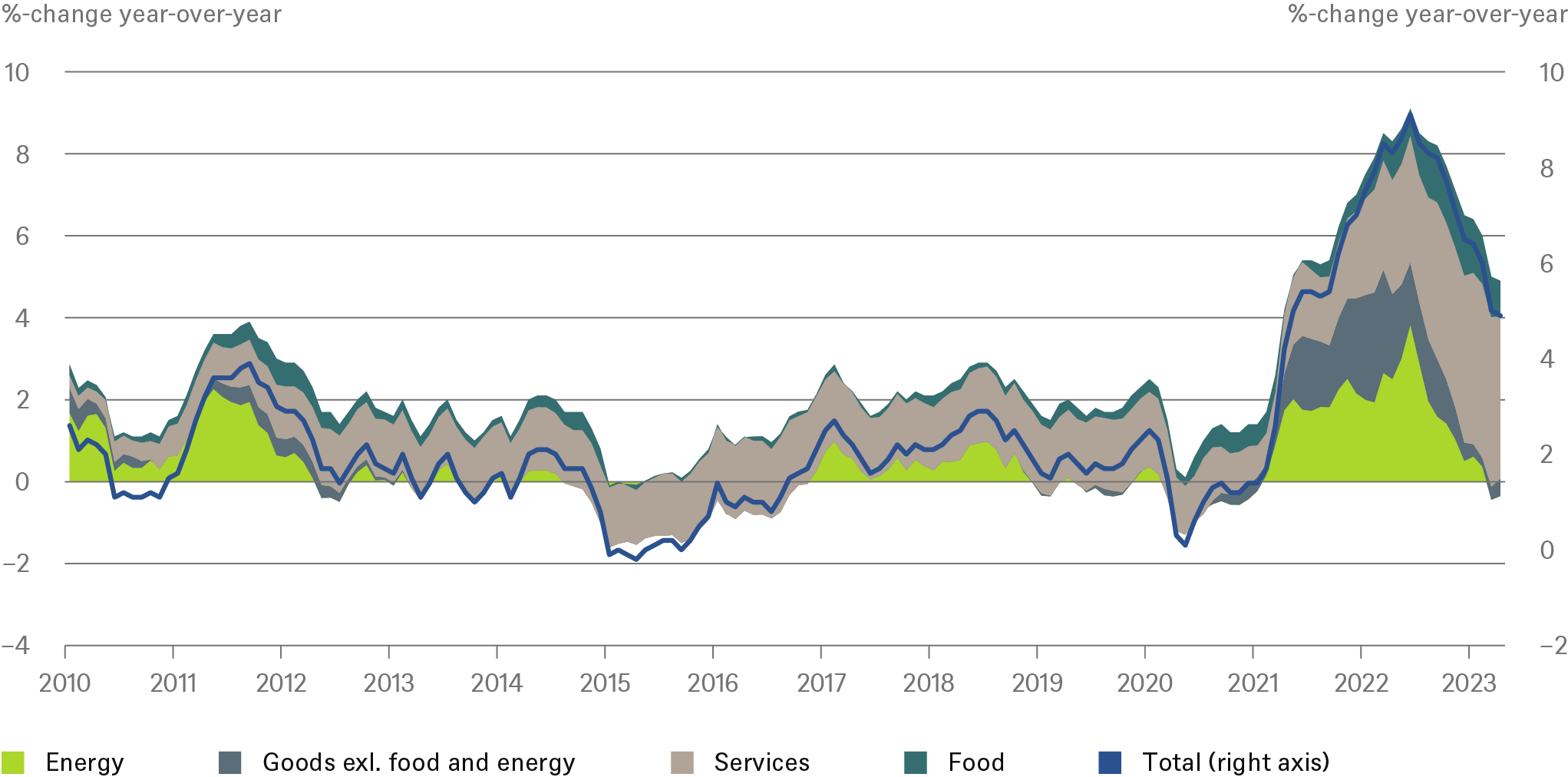

While overall inflation, as measured by the headline consumer price index (CPI), declined significantly since 2022, remaining drivers of price pressures might be around for some time to come. Chart 1 shows the decomposition of the headline CPI since 2010.

Chart 1: Contributions to change of headline Consumer Price Index

Source: Haver Analytics, DWS Investment GmbH as of 5/15/23

The chart reveals that core goods (goods excluding food and energy) and energy prices have been the main drivers of lower inflation rates since peaking in June 2022, up until now. Both, to some extent, relate to the external shocks the pandemic put on the economy as they were most likely driven by disrupted supply chains and reopening effects. Since last summer, the biggest source of observed headline inflation has been services, mainly due to shelter prices driven by residential rents, as well as labor intensive, comparatively low paid tasks, for example in leisure and hospitality. According to private sector measures of rental growth, which tend to lead the CPI’s shelter component, these pressures have started to cool somewhat since last fall, but we expect this process to take quite some time. Moreover, what remains quite sticky is service inflation excluding shelter which is said to be closely linked to the development in the labor markets.

And while labor markets started to show some signs off cooling as well, the overall conditions remain very tight. The root cause of this tightness remains two-fold: sticky labor supply meets still elevated labor demand. The open jobs to unemployed ratio declined to 1.64 in March – compared with being close to 2 in 2022 when price pressures from employment cost built up quickly (Chart2).

Chart 2: Less excess demand might imply lower growth rates for employment costs

Sources: Haver Analytics, DWS Investment GmbH as of 5/15/23

Turning a blind eye on these facts would most likely have resulted in a major accident – out of control inflation, which eventually might send the economy into a depression. Further spiraling wages and prices would risk de-anchoring inflation expectations. Put simply, people would start consuming more today as they expect their purchasing power to be eroded down the road and ask for higher wages, too. The typical consequences are even further rising prices eroding – and collateral damage to the economy, such as businesses collapsing.

To circumvent such a situation, the Fed had to hit the brakes quite aggressively since spring 2022 as they intentionally delayed their reaction leading up to the first hike. Had pandemic induced price pressures indeed proved transitory, braking too early might have been dangerous as well, after all. All of which highlights the challenges any modern bank faces in understanding where an economy “really” is heading at any given point in time. To put it in terms of the driving metaphor we started with, the critical task, once the deceleration is initiated, is to find the right level of interest rates that impose the right level of drag on economic activity. The tricky part in doing so is to incorporate the inertial behavior of our vehicle. An economy as big as the U.S. should be seen as a very large vessel rather than a dynamic sportscar: difficult to steer at the best of times, and very hard to do so when visibility is limited. Our calculations, that match with established estimates based on historical business and rate hiking cycles, suggests a 3-4 quarter lag of the main impact from monetary policy on the economy (Chart 3). It is worth keeping in mind, though, that both real economies and economic statistics will probably remain harder to read than usual for a while yet, not least given that recent shocks include a (hopefully!) once-in-century-pandemic.

Chart 3: Model estimated drag to GDP growth from past rate hikes

Source: Federal Reserve Board, DWS Investment GmbH as of 5/15/23

Having this in mind, doing too little or stopping braking too early results in what we and central bankers recall from the 70’s– the most likely consequence is that the critical situation is not solved properly. Fears of imposing more harm on businesses and households by failing to get inflation under control clearly remains at the top of many of today’s central banker’s minds. Following the recent Fed meeting, it seems like Fed-Chair Jerome Powell and his colleagues currently see benchmark federal funds rates in a range of 5.0%-5.25% as the right level of borrowing costs to tame inflation. We tend to agree to this judgement. Our model suggests an appropriate stance of monetary policy in the range of 4.3% - 4.7% in March when only the tightness of the labor market is considered (Chart 4). A federal funds rate slightly above this corridor should ensure that demand, including for labor, begins to moderate, thereby avoiding wages and prices resuming spiraling upwards.

Chart 4: Rates most likely high enough to keep pressure on labor markets

Sources: Michaillat, Pascal, and Emmanuel Saez. 2022, Haver Analytics, DWS Investment GmbH as of 5/15/23

We think, given the past trajectory of rate increases, and incorporating the expected lag of monetary policy, the Fed should keep rates at this level at least until early 2024 to keep inflation on a downward trajectory towards its increasingly flexible target of averaging 2%; in our view, the direction over the coming year, is likely to be as important in shaping policy as any month’s precise number.

The risk, as it is with every deceleration maneuver, is that your vehicle cannot bear the forces of retardation and something breaks, potentially resulting in an n accident as well. This analogy applies to the emerging risk to financial stability out of the U.S. banking sector. As of now, central bankers judge the banking sector as “sound and resilient”. Should this certificate of roadworthiness not reflect the real conditions of the sector, however, the consequences for the economic outlook would be significant. In such a case a mild recession, which we continue to expect to start later this year, quickly could turn into a more serious downturn. This situation might call for a different stance of monetary policy as current high inflation and tight labor markets are most likely no longer the only, or necessarily the main thing that central bankers have to worry about.

Instead, their primary focus right now rests on a possible credit crunch. In such a situation, credit institutions suddenly reduce their willingness to lend money to businesses and households which in turn slows economic activity. In extreme cases, such as the 1960s, when the term was initially coined, a credit crunch can lead to business insolvencies what in turn negatively impacts labor markets.[1] Causes of a credit crunch tend to typically include a sudden weakening of bank balance sheets as deposits are withdrawn quickly and/or if bank’s assets deteriorate in value. The latter might have been the root cause this time as fast increasing interest rates lowered the value of bank’s holdings in treasury securities. Usually, not all such valuation losses must be realized but once bank clients decide to withdraw their money at a larger scale for one or another reason, a bank might find itself in a situation of being forced to sell a certain amount of its holdings to fulfill client’s request, thereby realizing losses. In general, it is increasingly seen as good practice for banks to try to insure their investments against the risks from interest rate movements. However, U.S. rules on this have tended to be less stringent than in other advanced countries, especially for small to medium-sized U.S. banks. Recent research suggests that in the case of the first U.S. bank that collapsed, this practice was neglected to a large extent.[2] This failure most likely raised questions who else in the U.S. banking sector might have failed to take precautionary steps, such as engaging in insurance like protections against adverse market movements eroding their balance sheets. At the end of the day, it is a game of trust. If it is not possible to restore the trust, the lack of confidence might spill-over to other institutions that are under the cloud of potentially having similar issues. This is exactly what we have seen in the recent months. As of now, it seems like the situation remains under control. Joint efforts by official institutions like the Fed, the Treasury, and the FDIC but also the involvement of large private sector banks defused the situation somewhat. But we should remain vigilant as such situations can unfold very powerful dynamics.

Recent data does not yet indicate that the U.S. financial system is suffering from a credit crunch. Despite declining, deposits in the whole banking sector remain at about 30 percent above pre-pandemic levels. Unprecedent fiscal support during the pandemic, as well as (precautionary) savings, flooded bank deposits to an extend never seen in modern U.S. monetary history. It’s just natural to assume that once the economy is recovering out of the pandemic, those deposits are set to shrink again. So far, the fallout on lending has been muted as well. Weekly data suggests that the growth of lending is merely “slowing”, as one would expect when interest rates are higher, instead of “crunching”, as feared by some market participants (Chart 5).

Chart 5: Weekly available data of bank lending indicates slowing but no crunching

Sources: Haver Analytics, DWS Investment GmbH as of 5/15/23

In the May meeting, Fed-Chair Jerome Powell indicated that – despite the U.S. financial system being solid – tightening lending standards need to be watched closely as they could impact the economic outlook. While inflation remains too high and labor markets too tight, the Fed signaled a pause on rate hikes. This adds a flavor of increased caution by central bankers. Their intention, however, is to keep rates on high levels as long as necessary to tame inflation.

The subsequent release of the Senior Loan Officer Opinion Survey indeed points to an ongoing tightening of lending standards. While this tightening is exactly what central bankers want to see – a measure on how well the brakes are working – it also provides a measure of how well the financial system can cope with the pressure applied. We like to highlight that most of the tightening already has happened in the past quarters before we had stress in the banking system. The most recent reading, however, indicated that – while not signaling sudden credit crunch – that more pain on the economy is about to come (Chart 6).

Chart 6: Not yet a crunch but a mixed picture indeed: tightening lending standards

Source: Federal Reserve, Haver Analytics, DWS Investment GmbH as of May 2023

For the time being, it seems like the Fed’s brakes are working properly and the U.S. economy can deal with the forces of deceleration. But risks to financial stability remain and should not be neglected.

The same is true for another risk: “Investors brace for a painful crash into America’s debt-ceiling. A solution will probably be found. But default is no longer unthinkable.”[3], as The Economist recently put it. Really? Congress failing to lift the limit gross government borrowing (currently $31.4trn, or 117% of GDP), has, alas been quite imminently thinkable – and feared, to judge from market jitters reactions back in 2011 and 2013.

As we get closer to June 1st, the tentative date currently given by the Treasury for when it expects to run out of wriggle-room several other, distinct differences this time around are likely to shape the economic consequences. First, Republican House majority is extremely narrow and divided. This is in marked contrast to previous rounds of Congressional fiscal brinkmanship, which often centered on Republican demands for “entitlement reform” – cutting mandatory expenditures on social security, health care and the like. That these are now off-limit before negotiations even start shows how much the politics of deficits have shifted in both parties during the past decade. Second, the Biden administration seems increasingly inclined to avoid default at all costs, if necessary by continuing to borrow even after the limit is breached.[4] Third, opinion among U.S. constitutional scholars appears to have shifted quite a bit as to some of the relatively narrow, technical issues involved of what to make of, say, an administration deciding to breach the debt ceiling in order to meet other spending commitments also approved, and indeed mandated, by Congress.[5] The composition of the U.S. Supreme Court (SCOTUS), which now includes 6 Republican nominees out of 9 Justices, might well play a role in this, but not quite in the ways you might expect. How to interpret the 1917 Liberty Bond Act, 100 years onward, is one thing during a doctoral seminar, but probably quite different a time when the United States is once again putting itself on a war footing as the arsenal of democracy.[6] It is hard to imagine that a majority of SCOTUS Justices would willingly participate in a largely political drama that would actually risk bringing about a technical default, with all of the fallout, including for the Courts reputation, that might entail.[7]

As with legislative processes, judicial ones tend to be above the paygrade of a humble economist. That said, the various endgame scenarios currently doing the rounds among Constitutional scholars are already starting to reshape the incentives of various factions in Congress. A face-saving compromise involving the House Republican leadership remains quite likely. Other plausible outcomes include defections by a handful of Republican moderates in the Senate and House - probably without changing the overall, medium-term fiscal stance all that much, ahead of next year’s elections. That seems a shame, as the country’s longer-term fiscal challenges indeed do look quite worrying.[8] Staying within our analogy of slowing down a car, the real issues go beyond nervous passengers squabbling amongst themselves or with the driver at a particularly tricky stretch of road. It is where the car is heading the longer-term. In an ideal world, you would hope for bipartisan compromises. But given the bitterly partisan political realities in today’s Washington, we will happily settle for disasters being avoided until voters have another chance to weigh in next year.