Market overview

It has been a period utterly dominated by coronavirus. In March the fear was that the virus would spread rapidly in Europe, North America and elsewhere. This forced governments and companies into radical countermeasures and provoked marked distortions in the capital markets. April fluctuated between disillusionment as record-low economic data rolled in, a certain degree of getting used to dealing with the virus, and ultimately hope that easing of lockdowns will begin soon, depending on the country. Stock markets meanwhile have staged an impressive recovery. It remains to be seen whether this was due to the record-high packages from governments and central banks, an easing in the global growth rates of new infections, or simply the urge of investors to look, with a great deal of optimism, through the coronavirus's valley of tears toward post-virus recovery.

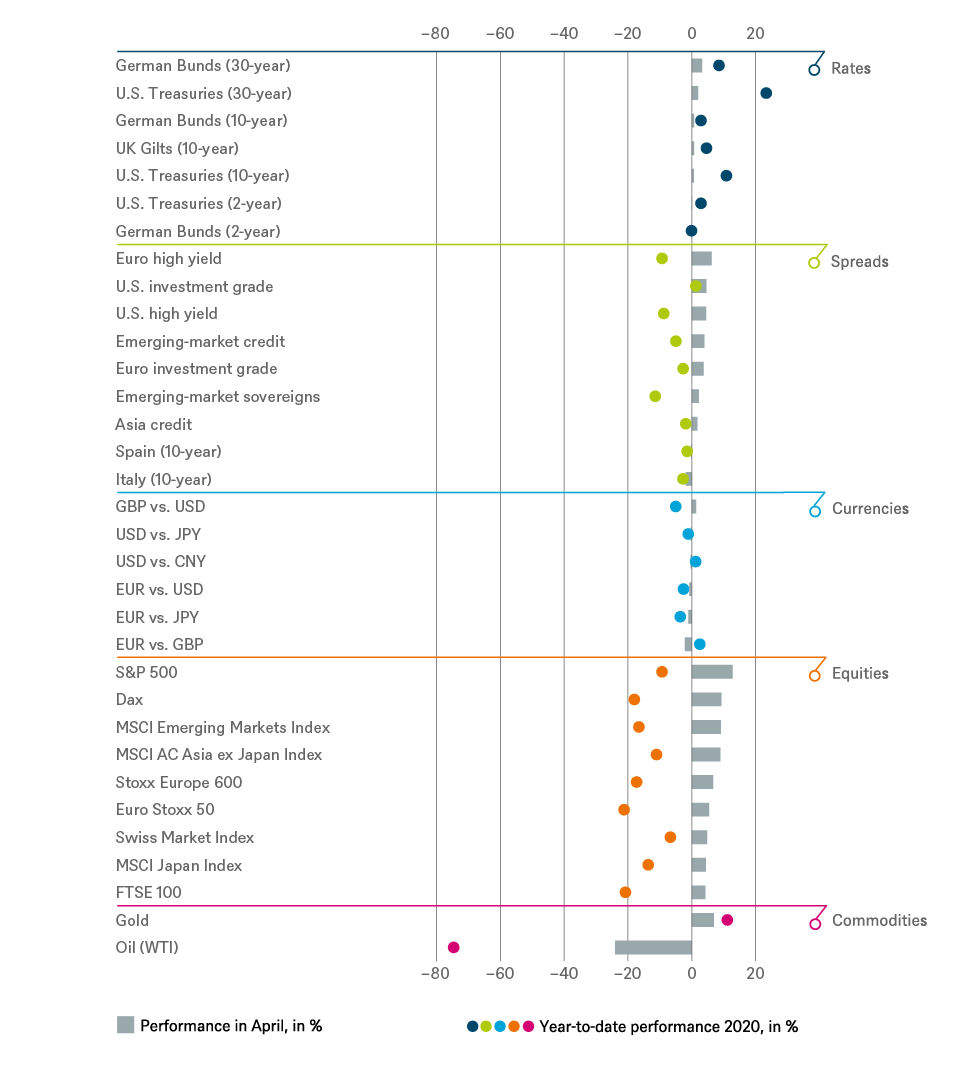

At the beginning of April, the S&P 500 was at 2,500 points and its volatility (measured by the Vix) jumped from around 15 in February to an extremely high 74. Almost one million Covid-19 cases and 50,000 Covid-19 deaths had been reported worldwide. At the end of March, 7.7 million Americans registered for continuing jobless claims, while short-time work in Germany was just being introduced. A month later, on April 30, 18 million Americans had registered for continuing jobless claims and over 10 million workers for short-time work in Germany. The S&P 500 is over 2,900 points, yielding a 12.3% return, its highest since January 1987. The Vix has slipped to 34. In addition, there are now 3.3 million global Covid-19 cases and 230,000 deaths.[1]

Amid the virus turmoil, oil underwent some turmoil of its own. Remarkably, a barrel of Brent crude started the month at around 25 dollars and ended it still at around 25 dollars a barrel. Surprising indeed because, as we all know, April saw unprecedented drama in the oil industry. West-Texas-Intermediate (WTI) crude (which is traded in the Midwest of the United States) slipped to minus 40 dollars per barrel at its low point. OPEC+ nations agreed on historically high cuts of some 10 million barrels per day early in the month but demand for oil in April probably fell by around 30 million barrels per day – to its 1995 level, according to the Paris-based International Energy Agency. With storage capacity becoming scarce and futures contracts forcing buyers without remaining storage space to take delivery of oil on a particular day, negative prices occurred. The oil market is likely to remain profoundly stressed for several months. Though lockdowns may be easing, traffic, especially air traffic, is likely to take a long time to return to pre-crisis levels. According to data from Flightradar24, commercial aircraft traffic is down by 72% since the beginning of the year.[2] In the United States this has caused a halving of the number of oil rigs in operation. Despite a lot of help from the White House, overriding normal market mechanisms, oil-production capacity is likely to shrink significantly in a year. Other, politically and economically more fragile countries may now lose production capacity that will not come back quickly, which is why we expect oil prices to be substantially higher in a year's time. But the risk of political unrest and severe economic imbalances in oil-export-dependent countries seems high.

At the same time, the low oil price has done little to brighten the mood of consumers, whether households or corporates. The first quarter has seen record economic declines, with gross domestic product (GDP) dropping by 4.8% annualized in the United States from the previous quarter, and 3.8%, not annualized, in the Eurozone. In France, some 40% of the workforce is working reduced hours, while the authorities in the United States are struggling to cope with the level of initial applications for unemployment benefits. The latest macro figures also offer little hope. In China, for example, which has been largely freed from restrictions, the Purchasing Managers' Indices fell again in April compared to March. In particular the sub-index measuring export orders slipped from 46.4 to 33.5 points. Most countries will likely hit the low point in their economic growth in the second quarter in which lockdowns have been at their height. For the United States, for example, we expect GDP to decline by 9% from the first quarter, or 36% on an annualized quarter-on-quarter basis. And yet the Americans are reacting more forcefully than any other country in terms of fiscal stimulus and central-bank balance-sheet expansion. The U.S. Federal Reserve's (Fed’s) balance sheet has already risen from 4.5 trillion dollars in mid-February to its current level of 6.7 trillion dollars. By the end of the year, it could surpass 10 trillion dollars. Meanwhile our estimates predict the U.S. budget deficit could rise to as much as 18% of GDP this year. We expect 7.5% for the Eurozone.

The markets gratefully received the fiscal and monetary gifts in April, with U.S. stocks up by around 30%. The question of who has to pay for the stimulus, when and in what form will be answered later. Major technology stocks at first only performed in line with the markets in the initial U.S. rally but have recently been able to gain some ground again, continuing their years of outperformance. The Nasdaq 100 ended April ahead of its level at the beginning of the year. The five largest U.S. stocks now account for a larger share of the S&P 500 than ever before, at over 20%. Internationally, too, the technology and communications sectors have outperformed since the beginning of the year, complemented by the healthcare sector, unsurprisingly given the pandemic. The frontrunner in April with 18.3%, however, was, remarkably, the energy sector, but only because it had lost so much in the first three months.[3] It remains at the bottom of the table in the year-to-date comparison. In the bond sector corporate bonds in particular performed well, not least because of the renewed central-bank intervention. In April the Fed even announced that it would also buy certain segments in the high-yield (HY) area while the European Central Bank (ECB) now also accepts certain HY bonds as collateral. In terms of commodities, gold was again able to gain ground in April, making it one of the very few asset classes to have risen since the beginning of the year.

Outlook and changes

After an extraordinary DWS strategy meeting, we provide both a tactical and a strategic outlook this month. We expect global GDP to decline by 2.6% in 2020 (United States minus 5.7%, Eurozone minus 7.5%), a year in which economic normalization is likely to be slow and incomplete by the end of it. We still believe China can achieve positive growth of 1%. This core scenario assumes there will not be a second, strong wave of coronavirus contagion in major industrialized countries. We expect continued low interest rates on government bonds in Europe and the United States, and a slight decline in risk premiums on corporate and emerging-market bonds. By March 2021, we expect the S&P 500 to return to 3,100 again, the Dax to climb to 12,000 and the Eurostoxx 50 to 3,150 points. We do not expect corporate earnings to regain their 2019 levels until 2022, which is also the basis for our price targets this time. For 2020, we expect the S&P 500 to post earnings per share (EPS) of only 110 dollars (after 164 dollars last year). The consensus is still expecting 129 dollars.

From a tactical perspective, we are somewhat more cautious. Relief over the gradual easing of the pandemic restrictions may be followed by disillusionment over the stuttering restart. Essentially, it is then a question of how high demand really is when supply returns. Business and consumer behavior is likely to remain cautious until the virus is largely contained. In countries with a weak social security system, such as the United States, the UK or even China, the savings ratio is likely to remain above the pre-crisis level for some time. In the short term, however, the immediate coronavirus figures are what markets will look at. The different approaches to dealing with the pandemic should also become apparent in the easing phase. To make a comparison of extremes, in the island state of Mauritius the (relatively strict) lockdown was extended until the beginning of June, although the country had only recorded a single-digit number of new infections over the past three weeks. In the United States, on the other hand, the new infections figure is still in the 20,000 to 30,000 per-day range, but many federal states are taking large steps toward complete relaxation. Aside, from the coronavirus and the election year in the United States, another problematic topic for markets has flared up: the dispute between the United States and China after President Trump makes China increasingly responsible for developing the virus.

We expect equities to consolidate after the strong recovery in recent weeks, and we do not rule out further severe setbacks. In general, the market is prepared to grant companies higher valuation multiples, even in the midst of the crisis and in a climate of almost unprecedented uncertainty. However, the current reporting season illustrates the far-sightedness investors need. Around four-fifths of companies have so far refrained from issuing an annual outlook. Quarterly figures are already tending to show quite well which sectors are suffering most from the virus – or benefitting from it, in the case of some companies from the technology, communications and healthcare sectors. These remain our favorites, thanks to their solid balance sheets and relatively stable sales and cash flows, but some cyclical stocks could also be given a boost in the coming weeks if investors gain confidence in the economic recovery. Regionally, we continue to have no clear preferences.

In the bond sector, the medium-term picture remains dominated by a weak economic outlook, the enormous rescue packages and the associated high refinancing needs of governments. We previously expected rising yields and thus weaker prices for European and U.S. government bonds but we have now switched back to neutral, including for the European peripheral countries. With corporate bonds, on the other hand, we see the potential for further narrowing of risk premiums. Certainly, the headlines about companies in financial distress will increase in the near future, as will actual credit defaults: we expect the default rate on European high-yield bonds for example to rise from 1% to 5%. Also, the continued unusually high level of issuance is putting some pressure on the market and may lead to a degree of indigestion. However, in view of the still high spreads relative to government bonds, the broad supportive measures taken by central banks, as well as the government-aid programs designed to avert company bankruptcies, we are leaving our positive assessment. We also continue to take a positive view of emerging-market bonds, whether issued by governments or companies, even though there is generally no central-bank buyer. However, we take quite distinct views on different countries, considering among other things the extent of their dependence on oil revenues and the burden of the lockdown on their public finances.

The multi-asset perspective

From the perspective of multi-asset portfolios, by mid-April capital-market valuations had already recovered to such an extent that a somewhat more defensive stance seemed appropriate. As a consequence, emerging-market equities were downgraded to underweight and developed markets were given a correspondingly higher weighting. The United States remains a slight favorite, not least because the sectors we value most are also particularly strong represented there: technology, communications and healthcare. Within emerging markets, we still see Asia as the strongest region.

Within bonds, we prefer hard-currency emerging-market bonds to high-yield bonds from Europe and the United States, especially as the recovery has been much less pronounced in emerging markets than developed ones. Although central banks are actively supporting the corporate-bond market, from a portfolio perspective we prefer equities in the short term, if only because they are more tradable during periods of market stress. But also in the longer term we believe that the crisis will strengthen the relative attractiveness of equities, especially compared to government bonds. At bonds' currently very low yield level, we believe there is very little room for maneuver (in terms of price) if further market turbulence drives investors into so-called safe havens. The diversification effect of government bonds will thus largely disappear. In addition, the current yield level is not very attractive if the aid packages already adopted by central banks and governments have inflationary impacts for some time.

Past performance of major financial assets

Total return of major financial assets year-to-date and past month

Past performance is not indicative of future returns.

Sources: Bloomberg Finance L.P., DWS Investment GmbH as of 4/30/20

Tactical and strategic signals

Fixed Income

| Rates | 1 to 3 months | until March 2021 |

|---|---|---|

| U.S. Treasuries (2-year) | ||

| U.S. Treasuries (10-year) | ||

| U.S. Treasuries (30-year) | ||

| German Bunds (2-year) | ||

| German Bunds (10-year) | ||

| German Bunds (30-year) | ||

| UK Gilts (10-year) | ||

| Japan (2-year) | ||

| Japan (10-year) |

| Spreads | 1 to 3 months | until March 2021 |

|---|---|---|

| Spain (10-year)[4] | ||

| Italy (10-year)[4] | ||

| U.S. investment grade | ||

| U.S. high yield | ||

| Euro investment grade[4] | ||

| Euro high yield[4] | ||

| Asia credit | ||

| Emerging-market credit | ||

| Emerging-market sovereigns |

| Securitized / specialties | 1 to 3 months | until March 2021 |

|---|---|---|

| Covered bonds[4] | ||

| U.S. municipal bonds | ||

| U.S. mortgage-backed securities |

| Currencies | ||

|---|---|---|

| EUR vs. USD | ||

| USD vs. JPY | ||

| EUR vs. JPY | ||

| EUR vs. GBP | ||

| GBP vs. USD | ||

| USD vs. CNY |

Equities

| Regions | 1 to 3 months[5] | until March 2021 |

|---|---|---|

| United States[6] | ||

| Europe[7] | ||

| Eurozone[8] | ||

| Germany[9] | ||

| Switzerland[10] | ||

| United Kingdom (UK)[11] | ||

| Emerging markets[12] | ||

| Asia ex Japan[13] | ||

| Japan[14] |

| Style | |

|---|---|

| U.S. small caps[26] | |

| European small caps[27] |

Legend

Tactical view (1 to 3 months)

- The focus of our tactical view for fixed income is on trends in bond prices.

- Positive view

- Neutral view

- Negative view

Strategic view until March 2021

- The focus of our strategic view for sovereign bonds is on bond prices.

- For corporates, securitized/specialties and emerging-market bonds in U.S. dollars, the signals depict the option-adjusted spread over U.S. Treasuries. For bonds denominated in euros, the illustration depicts the spread in comparison with German Bunds. Both spread and sovereign-bond-yield trends influence the bond value. For investors seeking to profit only from spread trends, a hedge against changing interest rates may be a consideration.

- The colors illustrate the return opportunities for long-only investors.

- Positive return potential for long-only investors

- Limited return opportunity as well as downside risk

- Negative return potential for long-only investors

Appendix: Performance over the past 5 years (12-month periods)

| 04/15 - 04/16 | 04/16 - 04/17 | 04/17 - 04/18 | 04/18 - 04/19 | 04/19 - 04/20 | |

|---|---|---|---|---|---|

|

Asia credit |

4.3% |

4.5% |

0.5% |

6.6% |

3.8% |

|

Covered bonds |

0.8% |

0.7% |

0.2% |

2.2% |

1.5% |

|

Dax |

-12.4% |

23.9% |

1.4% |

-2.1% |

-12.0% |

|

EM Credit |

2.8% |

8.7% |

1.3% |

7.0% |

1.7% |

|

EM Sovereigns |

4.3% |

8.6% |

1.3% |

6.0% |

-5.0% |

|

Euro high yield |

0.8% |

8.5% |

3.5% |

2.8% |

-5.9% |

| Euro investment grade |

1.2% |

2.7% |

1.2% |

3.0% |

-0.5% |

| Euro Stoxx 50 |

-13.2% |

22.1% |

2.8% |

2.9% |

-14.0% |

| FTSE 100 |

-6.8% |

20.0% |

8.5% |

3.1% |

-17.1% |

| German Bunds (10-year) |

2.7% |

0.8% |

-1.0% |

5.3% |

4.0% |

|

German Bunds (2-year) |

0.2% |

-0.2% |

-0.8% |

-0.4% |

-0.5% |

|

German Bunds (30-year) |

0.3% |

0.2% |

-1.1% |

10.6% |

14.0% |

|

Italy (10-year) |

2.9% |

-2.3% |

6.5% |

-1.7% |

6.4% |

|

Japanese government bonds (10-year) |

4.0% |

-0.5% |

-0.1% |

1.3% |

0.2% |

|

Japanese government bonds (2-year) |

0.4% |

-0.3% |

-0.2% |

-0.1% |

-0.2% |

|

MSCI AC Asia ex Japan Index |

-18.5% |

21.1% |

24.0% |

-4.1% |

-7.4% |

|

MSCI AC World Communication Services Index |

-6.0% |

-3.6% |

-1.1% |

4.9% |

-1.8% |

|

MSCI AC World Consumer Discretionary Index |

-4.7% |

13.1% |

14.8% |

4.3% |

-3.8% |

|

MSCI AC World Consumer Staples Index |

3.7% |

3.7% |

-1.1% |

6.3% |

-4.1% |

|

MSCI AC World Energy Index |

-18.2% |

1.7% |

14.6% |

-7.6% |

-38.4% |

|

MSCI AC World Financials Index |

-13.7% |

18.9% |

13.2% |

-5.2% |

-23.8% |

|

MSCI AC World Health Care Index |

-6.7% |

5.2% |

7.1% |

5.8% |

13.5% |

|

MSCI AC World Industrials Index |

-3.9% |

14.8% |

9.4% |

2.1% |

-16.3% |

|

MSCI AC World Information Technology Index |

-5.3% |

32.3% |

24.2% |

14.2% |

12.5% |

|

MSCI AC World Materials Index |

-11.9% |

15.2% |

14.7% |

-6.1% |

-14.1% |

|

MSCI AC World Real Estate Index |

-3.5% |

1.0% |

5.0% |

5.5% |

-13.7% |

|

MSCI AC World Utilities Index |

-1.0% |

1.8% |

4.3% |

6.4% |

-4.8% |

|

MSCI Emerging Market Index |

-17.9% |

19.1% |

21.7% |

-5.0% |

-12.0% |

|

MSCI Japan Index |

-6.1% |

10.5% |

19.2% |

-7.2% |

-3.0% |

|

Russel 2000 Index |

-7.3% |

23.8% |

10.1% |

3.2% |

-17.6% |

|

S&P 500 |

1.2% |

17.9% |

13.3% |

13.5% |

0.9% |

|

Spain (10-year) |

2.1% |

2.3% |

5.1% |

4.7% |

2.5% |

|

Stoxx Europe 600 |

-10.8% |

17.2% |

2.9% |

5.2% |

-10.2% |

|

Stoxx Europe Small 200 |

-6.3% |

20.6% |

6.0% |

2.8% |

-9.7% |

|

Swiss Market Index |

-9.3% |

14.5% |

4.3% |

13.3% |

2.3% |

|

U.S. high yield |

-1.1% |

13.3% |

3.3% |

6.7% |

-4.1% |

|

U.S. investment grade |

2.8% |

2.7% |

0.6% |

6.4% |

9.4% |

|

U.S. MBS |

25.0% |

35.0% |

3.7% |

46.4% |

-4.9% |

|

U.S. Treasuries (10-year) |

4.0% |

-1.3% |

-2.7% |

6.6% |

17.4% |

|

U.S. Treasuries (2-year) |

0.9% |

0.4% |

-0.3% |

3.1% |

5.3% |

|

U.S. Treasuries (30-year) |

5.3% |

-2.7% |

-0.2% |

6.4% |

37.8% |

|

UK Gilts (10-year) |

4.5% |

6.2% |

-1.6% |

4.1% |

8.4% |

Source: Bloomberg Finance L.P., DWS Investment GmbH as of 5/1/20

Past performance is not indicative of future returns.

2. Source: https://www.flightradar24.com/data/statistics, data as of May 3.

5. Relative to the MSCI AC World Index

6. S&P 500

8. EuroStoxx 50

9. Dax

11. FTSE 100

12. MSCI Emerging Markets Index

13.

MSCI AC Asia ex

Japan Index

14. MSCI Japan Index

15. MSCI AC World Consumer Stables

16. MSCI AC World Health Care Index

17. MSCI AC World Communication Services Index

18. MSCI AC World Utilities Index

19. MSCI AC World Consumer Discretionary Index

20. MSCI AC World Energy Index

21. MSCI AC World Financials Index

22.

MSCI AC World

Industrials Index

23. MSCI ACWI Information Technology Index

24. MSCI AC World Materials Index

25. MSCI AC World Real Estate Index

26. Russel 2000 Index relative to the S&P 500

27.

Stoxx Europe Small 200 relative to the Stoxx

Europe 600

28.

Relative

to the Bloomberg Commodity Index