- Home »

- Insights »

- Asset Class Perspectives »

- 2024 Real Estate Outlook

Real estate has historically been synchronized with the economy. Total returns were negative in the savings-and loan (early-1990s) and global financial (2008-09) crises and weak in the dotcom (2001) and COVID (2020) recessions.[1]Interest rates were mildly correlated with the economy (rising in expansions and falling in contractions), arguably muting the real-estate cycle, but never stopping it.[2]

This pattern dissolved in 2023, as real estate values fell despite strong economic growth (GDP was up 3% year-over-year in September).[3] The distinguishing factor, in our view, was the magnitude of the interest-rate shock: 10-year Treasury yields increased from less than 1% in 2020 to 5% in October 2023, the largest jump since 1980.[4] Unlike in past cycles, the detrimental effects of higher interest rates trumped the salutary effects of a buoyant economy.

To be sure, real estate dynamics were also at play. In the residential and industrial sectors, demand cooled from a COVID-fueled spike, while supply sparked by the initial surge materialized.[5] The office sector reeled from the effects of hybrid work, exacerbated by layoffs in the technology industry.[6] Still, vacancy rates across sectors remained near an all-time low in the third quarter of 2023 (5.7%) and net operating income (NOI) increased an inflation-beating 5.6% year-over-year.[1]

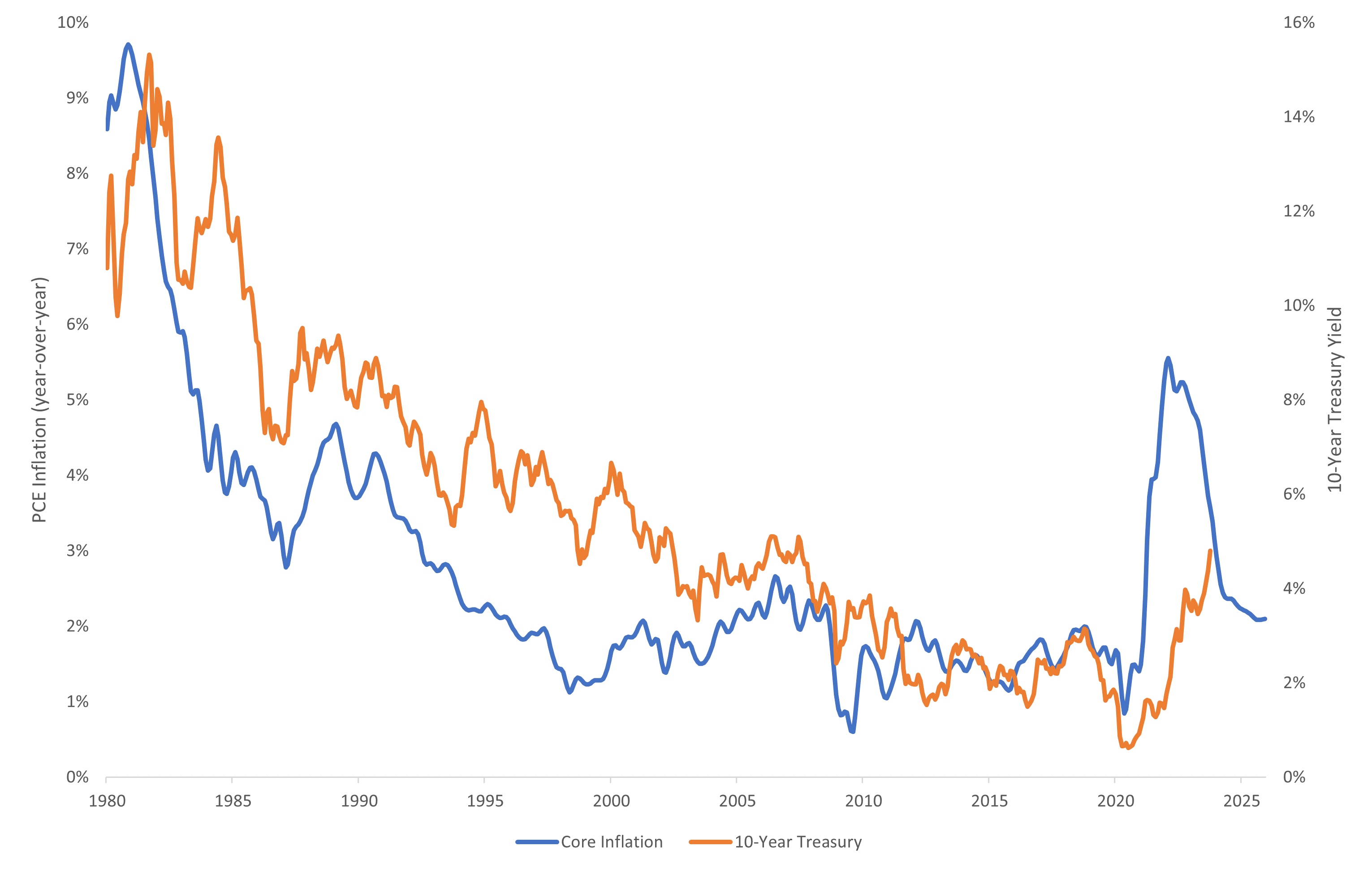

In our view, interest rates are pivotal to the near-term outlook. Since 1980, 10-year Treasuries have been strongly correlated (0.74) with inflation, which is on a downward trajectory thanks a shrinking money supply and a resolution of COVID-related imbalances (see Exhibit).[7] It is not the only consideration: Burgeoning fiscal deficits and the Federal Reserve’s efforts to shrink its balance sheet arguably exert upward pressure on interest rates, while an abundance of global savings, courtesy of an ageing population, could push them lower.[8] The reality may lie somewhere in the middle. With inflation under control, Treasury yields could settle above levels prevailing in the 2010s (around 2.5%) but below those of the 2000s (4.5%).[9]

Exhibit: Inflation and Treasury Yields

Sources: Moody’s Analytics (inflation); Federal Reserve (Treasury). As of October 2023.

If this interest-rate perspective is roughly correct, market cap rates have likely peaked, while appraisal-based cap rates, which respond with a lag, may be nearly there. This would represent a sea change for real estate: at worst, it would remove a major headwind to valuations; at best, it would create tailwinds for future performance, should cap rates follow interest rates lower.

Though a secondary consideration in this cycle, fundamentals should not be neglected. The yield curve, which has inverted 1-2 years before each of the past eight recessions, points to an economic downturn in 2024.[10] Buffers built up during the pandemic — $2 trillion in surplus savings and pent-up demand for vehicles and other goods — have run down, exposing the economy to higher interest rates.[11] The weaker confidence and spending power associated with recessions typically stifle real estate demand.[12]

However, any pullback may be limited. In our view, the recession will be short and mild, thanks to robust consumer finances (wealth is elevated and financial obligations are low relative to incomes).[13] Structural drivers, including population growth and prohibitive for-sale affordability (residential) as well as e-commerce and supply-chain resilience (industrial), may act as a counterweight. Moreover, lower prices and restrictive financing have curtailed construction: Starts plunged 65% from their 2022 peak in the third quarter of 2023.[14] Existing projects will come to fruition in 2024, but thereafter, supply is poised to evaporate. Overall, we believe that rents will hold roughly steady in 2024 (they fell 5%-10% in the global financial crisis and dotcom bust), before accelerating sharply in 2025 and 2026.[15]

We believe that 2024 will mark a turning point for U.S. real estate, as easing financial conditions offset a soft patch for fundamentals. Beyond 2024, prospects are increasingly bright, in our view. Lower prices are pushing income returns to their highest level in more than a decade.[16] Fundamentals are essentially sound, and supply shortages may propel strong rent growth over the next several years. If interest rates ease, cap rates could follow suit, adding further support to capital appreciation. In short, we believe that 2024 may provide an attractive entry point to capitalize on the coming cycle.